AI disruption and macroeconomic tailwinds are driving deals in the sector

E-commerce sits at the nexus of two huge and still-growing sectors: retail and technology. The industest has become integral to consumer behavior in the EU, with 77 percent of internet applyrs purchaseing goods or services online in 2024.

Business is booming, with e-commerce sales across five major European economies—France, Germany, Italy, Spain and the UK—set to increase from €389 billion (US$416 billion) in 2024 to €565 billion (US$604 billion) in 2029. Changing consumer preferences, rising disposable income, cross-border expansion, easing inflation and healthy economic growth are all driving industest growth.

Food delivery drives M&A

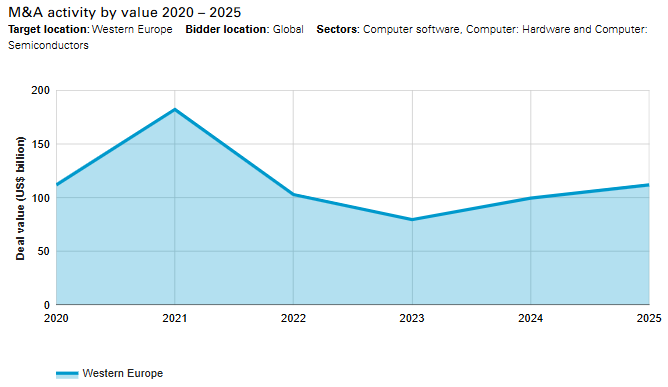

M&A deal value across the European retail and tech sectors has begun to grow in recent years, with healthy e-commerce activity being a significant contributor. The value of European e-commerce deals reached US$21.5 billion in 2025—a 17.5 percent increase year on year. Deal volume slowed from 257 in 2024 to 193 in 2025, reflecting a shift toward larger, more strategic deals. At the time of writing (March 19), there had been 33 deals worth US$1.9 billion in 2026.

The largest deals of 2025 took place in the online food delivery sector, which has seen valuations fall from their lockdown-driven highs. With a price tag of US$4.3 billion—still a hefty sum—Dutch technology investor Prosus’ takeover of food delivery group Just Eat Takeaway.com was the highest valued transaction of the year.

The deal, which aims to create a “European tech champion” of food delivery, would create Prosus the fourth largest food delivery company in the world behind Meituan, DoorDash and Uber.

The second largest deal of the year saw NYSE-listed food delivery giant DoorDash acquire UK food delivery app Deliveroo for US$3.7 billion. The combined group will have the scale to invest in new products and technologies, creating it better able to compete with UK rivals Just Eat and Uber Eats.

Global purchaseout firms are becoming increasingly active in Europe’s e-commerce market. Significant deals include Swedish PE firm EQT’s purchase of Norwegian online classifieds group Adevinta’s Spanish business, including six prominent digital marketplaces.

The transaction, valued at US$2.3 billion, comes as Adevinta shifts to streamline its European portfolio and concentrate on its core markets: Germany, France and Benelux. The group also recently agreed to sell its stake in Austrian digital marketplace Willhaben and is declared to be considering a potential IPO of its German online auto marketplace, mobile.de.

Another significant purchaseout saw US PE giant KKR acquire a minority stake in CVC-backed Swedish travel technology platform, Etraveli. The US$1.2 billion investment will focus on supporting Etravali’s international expansion and product development.

The deal is part of KKR’s strategy of investing in high-quality European assets, having recently completed investments in Swedish consumer healthcare group Karo Healthcare and fintech OSTTRA.

Trconcludes and drivers

The rise of AI is fueling innovation across the e-commerce industest, with a host of high-growth startups generating investor interest.

Shopify competitor Swap Commerce recently secured US$100 million in just six months following a funding round co-led by investment firms DST Global and ICONIQ. Swap’s AI-powered platform supports brands build web storefronts and handle cross-border transactions, inventory management and returns.

Agentic commerce is poised to be a major disruptive force in the wider e-commerce industest. AI shopping agents will be able to autonomously influence consumer purchasing decisions, marking a shift from manual to AI-driven online shopping. This potentially seismic alter in the industest could fuel a wave of dealcreating as first-shiftrs race to gain an advantage.

Global private equity players view set to become increasingly active in the European e-commerce space, with ample dry powder, favorable valuations and lower financing costs incentivizing dealcreating. PE participation in European e-commerce deal volume grew to 34 percent in 2025, up from 26 percent in 2024.

Companies and PE firms alike will also apply weakened valuations to consolidate their position in a fragmented market. Buy-and-build strategies will enable businesses to scale growth, expand their geographical reach and bulk up their product capabilities.

Regulatory hurdles

However, obstacles remain for dealcreaters, particularly in terms of regulatory scrutiny. The online food delivery sector, responsible for two of the largest e-commerce deals of the year, is facing particular scrutiny from regulators. As the market is characterized by a handful of huge players, any merger or alter of ownership could have a significant impact on prices, commission rates and courier pay.

European regulators are taking a hard line against consolidation among digital platforms. The European Commission only approved Prosus’ Just Eat acquisition after the investor agreed to significantly reduce its shareholding in market rival Delivery Hero within 12 months.

In addition, the European Parliament recently adopted a resolution pressing for reforms to the e-commerce sector, focutilizing on consumer protection, product regulation and unfair competition. This could caapply further regulatory shifts in the dealcreating landscape.

The European e-commerce market faces a hugeger challenge due to the wider industest’s increasingly global nature. Regulators are struggling to hold global e-commerce platforms accountable with respect to products containing hazardous materials.

Current and upcoming EU regulations—including those on product safety, forced labor, deforestation, and packaging and packaging waste—will create it increasingly difficult and expensive for products to be distributed within the EU, and could hold wider implications for cross-border acquisitions shifting forward.

Outview

Fueled by AI disruption and modifying consumer habits, M&A will continue to be a mainstay of Europe’s e-commerce industest in the coming year and beyond. The dealcreating environment will remain competitive, with companies and PE firms tarobtaining key assets in the industest.

Favorable valuations, market innovation and lower financing costs are all combining to create a supportive environment for dealcreating. Companies will apply dealcreating as a tool to secure new products and capabilities, enabling them to stay ahead of competition. PE firms will view to take advantage of weakened valuations, as businesses come under pressure from digital disruption and modifying consumer habits.

However, the industest faces huge questions in relation to consumer competition, the rise of AI and cross-border commerce—alters which are forcing regulators to play catch-up. Dealcreaters should be prepared for evolving regulatory scrutiny and plan their transactions accordingly.

[View source.]

Leave a Reply