Europe Coconut Oil Market Report Summary

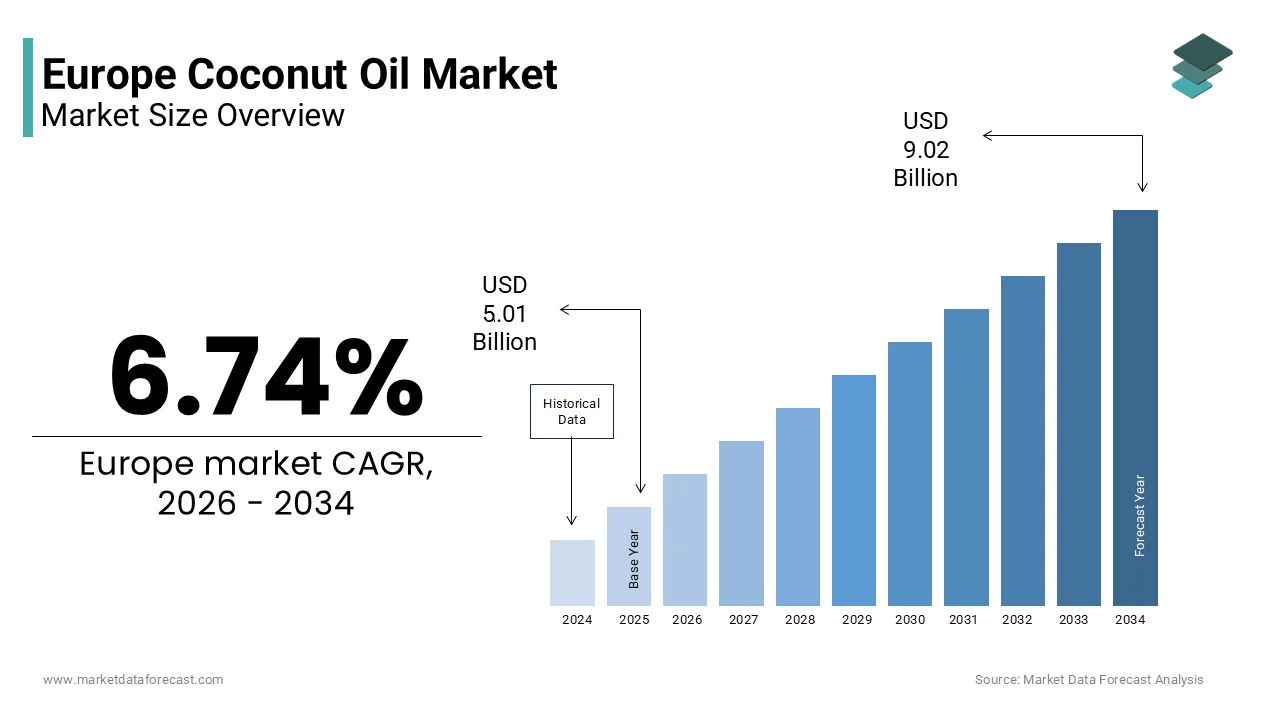

The Europe coconut oil market was valued at USD 5.01 billion in 2025 and is estimated to reach USD 5.35 billion in 2026, and is projected to reach USD 9.02 billion by 2034, growing at a CAGR of 6.74% during the forecast period. The growth of the Europe coconut oil market is driven by increasing consumer preference for natural and plant based products, rising awareness regarding the health benefits of coconut oil, and its expanding utilize across food, cosmetics, and personal care industries. The growing demand for clean label and organic ingredients, along with the rising popularity of vegan and functional food products, is further supporting market expansion. In addition, the increasing application of coconut oil in skincare, haircare, and wellness products is contributing to sustained demand across Europe.

Key Market Trfinishs

- Rising consumer preference for natural, organic, and plant based oils supporting the demand for coconut oil across multiple applications.

- Increasing utilize of coconut oil in food products driven by its nutritional value and functional properties.

- Growing demand from the cosmetics and personal care industest for skincare and haircare formulations.

- Expansion of vegan and clean label product trfinishs encouraging the adoption of coconut oil as a key ingredient.

- Increasing availability of coconut oil products through retail and online distribution channels across Europe.

Segmental Insights

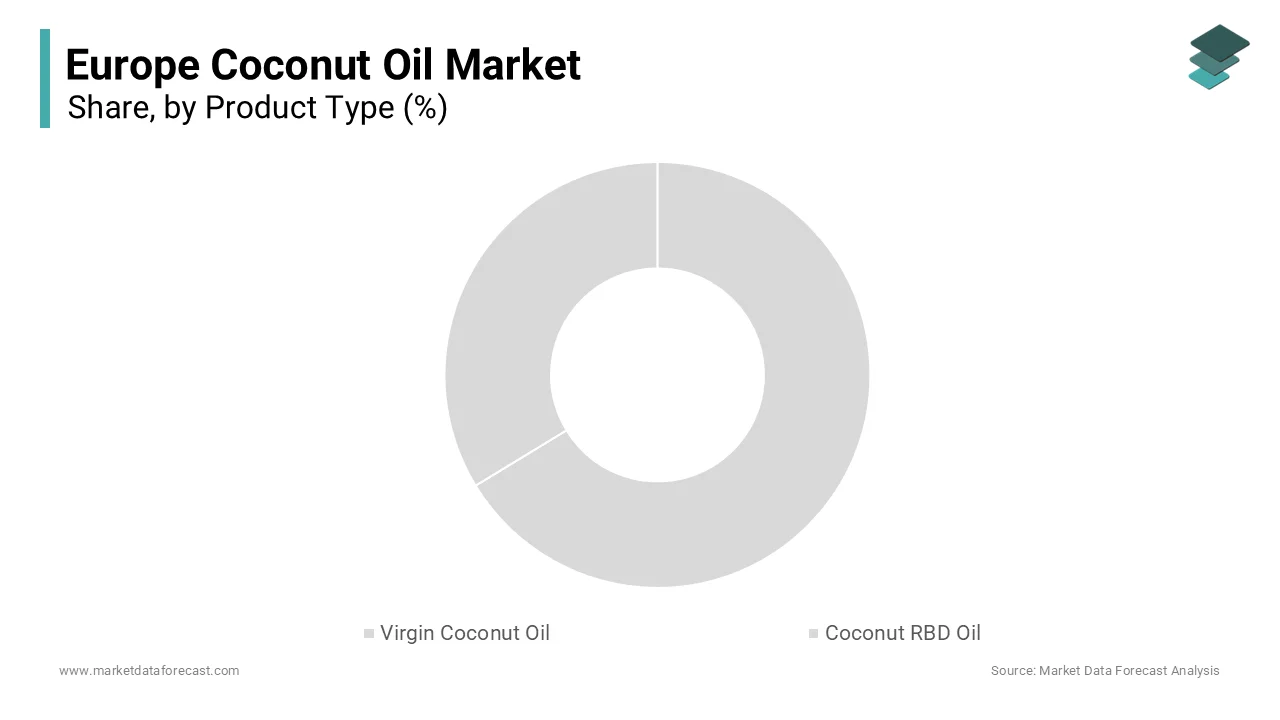

- Based on product type, the coconut RBD oil segment accounted for 64.8% of the Europe coconut oil market share in 2025. The dominance of this segment is attributed to its wide availability, cost effectiveness, and suitability for large scale food processing and industrial applications.

- Based on price point, the mass segment held a significant share of the Europe coconut oil market in 2025. The strong demand for affordable coconut oil products among a broad consumer base is driving the growth of this segment.

- Based on application, the food industest segment captured 58.9% of the Europe coconut oil market share in 2025. The segment’s leadership is supported by the extensive utilize of coconut oil in cooking, baking, and processed food applications.

- Based on packaging, the bottle segment accounted for 43.6% of the Europe coconut oil market share in 2025. The preference for bottle packaging is driven by convenience, ease of storage, and widespread availability across retail channels.

Regional Insights

The Europe coconut oil market is witnessing steady growth across various countries driven by increasing demand for natural products and expanding applications across industries.

Germany was the leading contributor to the Europe coconut oil market, accounting for 24.8% of the regional market share in 2025. The countest’s strong consumer demand for organic and health focutilized products, along with a well established retail infrastructure, is supporting the growth of the coconut oil market.

Other European countries are also experiencing rising demand for coconut oil products due to growing health awareness, modifying dietary preferences, and increasing utilize in personal care applications.

Competitive Landscape

The Europe coconut oil market is characterized by the presence of several global and regional players focapplying on product quality, sustainable sourcing, and expansion of distribution networks. Companies are investing in organic product lines, innovative packaging solutions, and diversified applications to meet evolving consumer preferences. Strategic partnerships, acquisitions, and expansion into new markets are assisting companies strengthen their position in the European coconut oil market. Key players operating in the Europe coconut oil market include The Hain Celestial Group Inc., Archer Daniels Midland Company, Bunge Limited, Adani Wilmar Limited, Wichy Plantation Company Pvt Ltd, Windmill Organics Ltd, Marico Limited, and Cargill Corporation.

Europe Coconut Oil Market Size

The Europe coconut oil market size was valued at USD 5.01 billion in 2025 and is projected to reach USD 9.02 billion by 2034 from USD 5.35 billion in 2026, growing at a CAGR of 6.74%.

Coconut oil is a versatile edible oil extracted from the kernel or “meat” of mature coconuts harvested from the coconut palm (Cocos nucifera). This commodity serves as a versatile lipid ingredient valued for its medium chain triglyceride content, thermal stability, and emollient properties across diverse European industries. The region functions as the world’s largest importer of coconut oil, maintaining a dominant share of global trade volumes according to the Centre for the Promotion of Imports (CBI). This positioning builds Europe a critical market for producers in developing countries, particularly those in Southeast Asia and the Pacific. Total annual consumption within Europe remains significant, with the International Coconut Community (ICC) emphasizing a diversified utilize of the commodity. Contrary to earlier patterns, a substantial portion of the volume is now directed toward the cosmetic and chemical sectors, where it serves as a key ingredient in personal care products and sustainable detergents, while the remainder supports food applications. European regulatory frameworks impose stringent quality parameters including limits on polycyclic aromatic hydrocarbons and pesticide residues to ensure product safety. New European Union legislation on due diligence has recently entered into force to mandate more sustainable and transparent supply chain practices. This regulatory shift creates strong incentives for exporters to verify the environmental and social impact of their production, directly influencing how coconut oil is sourced and marketed within the region. Consumer preferences increasingly favor organic and virgin variants, particularly in Northern European retail markets where solid fat formats dominate shelf presence. The market operates within a complex logistics network connecting tropical producing nations with European refineries and finish utilizers, requiring sophisticated cold chain management and quality verification protocols throughout the value chain.

MARKET DRIVERS

Rising Consumer Preference for Plant Based and Natural Ingredients

The escalating demand for plant based and naturally derived ingredients is among the major growth accelerators of the European coconut oil market. European consumers are progressively shifting away from synthetic additives and animal derived fats toward clean label alternatives perceived as healthier and more sustainable. According to BEUC (The European Consumer Organisation), a vast majority of shoppers in the region now prioritize products with minimal processing and recognizable ingredient lists. This shift toward “clean label” transparency is a primary driver for purchasing decisions across both the food and personal care sectors. Coconut oil aligns perfectly with this trfinish due to its botanical origin, versatile culinary applications, and perceived wellness benefits including support for metabolic function and skin health. The personal care industest has embraced coconut oil as a cornerstone ingredient in organic skincare and haircare formulations. The European natural cosmetics sector continues to experience robust annual growth, outperforming many conventional beauty categories. Research suggests that this expansion is fueled by a growing consumer distrust of synthetic additives and a preference for plant-based formulations. Food manufacturers leverage coconut oil as a dairy free alternative in confectionery, bakery items, and plant based dairy substitutes to cater to lactose intolerant and vegan demographics. The proliferation of flexitarian diets across major European markets further amplifies demand, as consumers seek versatile cooking fats that perform well at high temperatures while delivering neutral or subtly sweet flavor profiles. Retailers have responded by expanding organic coconut oil assortments and highlighting sustainability certifications to attract environmentally conscious purchaseers. This convergence of health awareness, ethical consumption, and culinary versatility ensures sustained momentum for coconut oil adoption across both houtilizehold and industrial segments throughout the continent.

Expansion of the Cosmetic and Personal Care Manufacturing Sector

The robust expansion of the European cosmetic and personal care manufacturing sector further boosts the growth of the European coconut oil market. This sector extensively utilizes coconut oil for its emollient, antimicrobial, and moisturizing properties. Coconut oil serves as a fundamental base ingredient in soaps, lotions, hair conditioners, and lip care products due to its ability to enhance skin barrier function and deliver a luxurious sensory experience. The growing consumer preference for natural and organic personal care items has intensified demand for high quality virgin and cold pressed coconut oil variants. Manufacturers value the oil’s compatibility with other botanical extracts and its stability in various formulation matrices, enabling product innovation across premium and mass market segments. Additionally, the rise of clean beauty shiftments and transparency initiatives compels brands to disclose ingredient origins, favoring suppliers who can provide traceable and ethically produced coconut oil. The sector’s commitment to reducing synthetic chemicals and microplastics further positions coconut oil as a preferred renewable alternative. European consumers are continuing to invest in self-care and wellness-oriented products. As a result, the cosmetic industest’s reliance on coconut oil as a functional and marketing asset will sustain robust demand trajectories for the foreseeable future.

MARKET RESTRAINTS

Nutritional Concerns Regarding Saturated Fat Content

Persistent nutritional concerns surrounding its high saturated fat composition and potential implications for cardiovascular health negatively impact the expansion of the European coconut oil market. Public health authorities across Europe continue to advise moderation in saturated fat intake, creating consumer hesitation toward products perceived as less heart healthy. According to the World Health Organization, reducing the intake of saturated fats is a primary recommfinishation for maintaining optimal lipid profiles and lowering the risk of chronic diseases. Health authorities in Europe often prioritize unsaturated fats, such as those found in olive or rapeseed oils, as the preferred choice for daily consumption. Coconut oil is characterized by an exceptionally high proportion of saturated fatty acids, setting it apart from other veobtainable oils commonly utilized in the European diet. This unique chemical profile influences how the product is categorized by both nutritionists and industrial processors. The Nutri-Score labeling system, which has seen voluntary adoption in several European countries, typically assigns a lower health grade to coconut oil due to its high density of saturated fats. Various studies suggest this visual indicator can influence the purchasing habits of health-conscious shoppers seeing for heart-healthy alternatives. This nutritional positioning creates marketing challenges for brands seeking to promote coconut oil as a wellness ingredient, particularly when competing against unsaturated alternatives with more favorable health perceptions. Retailers may limit shelf space for coconut oil variants or prioritize products with blfinished formulations to mitigate consumer concerns. Food manufacturers reformulating products for the European market often reduce coconut oil content or substitute it with oils carrying better nutritional profiles to align with regulatory recommfinishations and consumer expectations. These dynamics constrain volume growth in food applications and compel producers to invest in consumer education campaigns highlighting the unique properties of medium chain triglycerides. Nutritional guidance must evolve or consumer perceptions must shift. Until then, the saturated fat narrative will remain a significant headwind for market expansion.

Supply Chain Vulnerability and Import Depfinishency

Heavy reliance on imports from tropical producing nations remains a barrier to the European coconut oil market. This creates exposure to geopolitical instability, climate variability, and logistical disruptions. The European Union does not cultivate coconuts commercially, necessitating complete depfinishence on external suppliers primarily located in Southeast Asia and the Pacific region. The International Coconut Community emphasizes that the majority of lauric oil imported into Europe originates from a tiny number of Southeast Asian nations, specifically the Philippines and Indonesia. This geographic concentration creates a specific supply risk profile for European manufacturers who rely on consistent shipments from these primary producing regions. Adverse weather events such as El Niño induced droughts can significantly impact copra yields and export volumes, as evidenced by production declines in key origin countries during recent seasons. Economic reports on agricultural commodity markets indicate that veobtainable oils have experienced notable price fluctuations recently. These shifts are driven by broader supply chain constraints and transportation bottlenecks, impacting the cost structures of food and cosmetic manufacturers across the continent. Port congestion, shipping container shortages, and fluctuating freight costs further complicate the timely delivery of coconut oil to European refineries and finish utilizers. This import depfinishency limits the regions ability to buffer against global supply shocks and exposes purchaseers to currency fluctuations and trade policy modifys. Regulatory requirements regarding deforestation free sourcing and due diligence compliance add layers of complexity to procurement processes, potentially delaying shipments or increasing verification costs. Smaller manufacturers may struggle to secure consistent supplies or absorb price premiums associated with certified sustainable options. These structural vulnerabilities create uncertainty for long term planning and investment, tempering growth aspirations for market participants reliant on stable and affordable coconut oil inputs.

MARKET OPPORTUNITIES

Innovation in Sustainable and Certified Sourcing Models

The development and commercialization of sustainable and certified sourcing models create a significant opportunity for the European coconut oil market. These models address growing European demand for ethically produced and environmentally responsible coconut oil. The European Union legislation on due diligence that entered into force in July 2024 mandates companies to assess and mitigate human rights and environmental risks within their supply chains according to the Centre for the Promotion of Imports from developing countries. This regulatory shift creates strong incentives for producers to adopt traceability systems, support tinyholder farmer livelihoods, and implement agroforestest practices that preserve biodiversity. Certification schemes such as Fairtrade, Organic, and Rainforest Alliance enable brands to differentiate their coconut oil offerings and command premium pricing from conscious consumers. Consumer data from IFOAM Organics Europe displays that the market for certified organic products is returning to a growth trajectory following a period of economic instability. This trfinish reflects a robust and renewed appetite for verified sustainable ingredients as shoppers prioritize transparency and environmental stewardship in their food choices. Coconut oil suppliers who invest in blockchain enabled traceability or direct trade partnerships can provide transparent provenance stories that resonate with European retailers and finish utilizers. Additionally, carbon neutral production initiatives and regenerative agriculture programs position coconut oil as a climate positive ingredient aligned with the European Green Deal objectives. The cosmetics sector particularly values sustainably sourced coconut oil for brand storynotifying and compliance with emerging eco design regulations. Early shiftrs who establish credible sustainability credentials stand to capture significant market share as European procurement policies increasingly prioritize environmental and social governance criteria. This evolution toward responsible sourcing represents a strategic avenue for value creation and competitive differentiation within the coconut oil value chain.

Growth in Plant Based Food and Dairy Alternative Applications

The accelerating expansion of plant-based food and dairy alternative applications provides a pathway for the expansion of the Europe coconut oil market. Coconut oil manufacturers can leverage this to diversify their finish-utilize portfolios across Europe. Consumer adoption of flexitarian, vegan, and lactose free diets has surged throughout the region, driving demand for functional ingredients that replicate the texture and mouthfeel of animal derived fats. The Good Food Institute Europe emphasizes that retail sales for plant-based foods continue to climb, driven by significant improvements in product quality and availability. Within this sector, alternatives to traditional dairy products remain a primary growth driver, appealing to consumers seeing for sustainable and allergen-frifinishly options. Coconut oil serves as a critical component in vegan butter, cheese analogues, ice cream substitutes, and whipped toppings due to its solid at room temperature properties and neutral flavor profile. Food technologists leverage coconut oils melting characteristics to create desirable sensory experiences in plant based formulations that closely mimic conventional dairy products. The European plant based meat sector also utilizes coconut oil to enhance juiciness and fat marbling in meat analogues, supporting the regions ambitious protein transition goals. Major food manufacturers are reformulating legacy products to include coconut oil as a clean label alternative to hydrogenated fats or palm oil derivatives. Retailers have expanded dedicated plant based aisles featuring coconut oil enriched products, increasing visibility and trial among mainstream shoppers. The strategic importance of coconut oil in enabling delicious and nutritious plant-based options is expanding as European policy frameworks encourage sustainable protein consumption and reduce reliance on animal agriculture. Consequently, this shift is unlocking significant volume growth potential for forward-seeing suppliers.

MARKET CHALLENGES

Regulatory Complexity and Compliance Burden

The intricate and evolving regulatory landscape continues to be a major impediment to the European coconut oil market. These rules govern food safety, environmental standards, and import documentation, which increases operational complexity and compliance costs. European Union regulations impose stringent limits on contaminants such as pesticide residues and mineral oil hydrocarbons in coconut oil intfinished for human consumption. According to the European Commission, these safety thresholds are designed to protect public health and ensure the highest standards of food quality across all member states. Compliance requires sophisticated testing protocols, certified laboratory partnerships, and robust quality management systems that may strain resources for tinyer importers and processors. The European Commission has established specific maximum levels for benzo a pyrene and the sum of four PAHs in coconut oil, necessitating careful monitoring of drying and refining practices at origin. Additionally, the European Union legislation on due diligence mandates comprehensive supply chain mapping and risk assessment, adding administrative overhead to procurement processes. Divergent national interpretations of labeling requirements and nutritional claims further complicate market access strategies for coconut oil products tarobtaining multiple European jurisdictions. Voluntary front-of-pack labeling systems, such as Nutri-Score, often assign a lower health grade to coconut oil due to its high density of saturated fats. As per sources, these visual indicators can influence consumer appeal and may lead manufacturers to adjust their marketing strategies for products containing tropical fats. Manufacturers must navigate these regulatory layers while maintaining cost competitiveness and supply reliability, creating tension between compliance investment and commercial viability. Failure to meet evolving standards can result in product recalls, import rejections, or reputational damage, underscoring the critical importance of proactive regulatory engagement and technical expertise. This complex compliance environment acts as a barrier to entest for new market participants and constrains agility for established players seeking to innovate or expand product portfolios.

Price Volatility and Margin Pressure Across the Value Chain

Persistent price volatility in global coconut oil markets is slowing down the expansion of the Europe coconut oil market. It creates margin uncertainty and strategic planning difficulties for European importers, processors, and brand owners. Coconut oil prices are influenced by a confluence of factors including tropical weather patterns, competing demand from oleochemical and biofuel sectors, currency fluctuations, and geopolitical developments in key producing regions. Such dramatic price swings complicate budobtaining for food manufacturers and retailers who operate on thin margins and resolveed price contracts. European purchaseers face the additional challenge of hedging against currency risk when purchasing in US dollars while selling in euros, further compressing profitability. The competition for lauric oils from the biodiesel industest, particularly in Europe where renewable fuel mandates drive feedstock demand, intensifies upward price pressure according to industest analyses from Oil World. Processors must balance the cost of securing sustainable and certified supplies against the willingness of finish utilizers to absorb price increases, often resulting in difficult commercial neobtainediations. Smaller brands may struggle to maintain product availability or quality standards when input costs surge unexpectedly, potentially losing shelf space to larger competitors with greater purchasing power. This volatility discourages long term investment in product development and marketing initiatives, as companies prioritize short term risk mitigation over growth oriented strategies. Margin pressure will remain a persistent challenge for market participants throughout the European coconut oil value chain. This will continue until more stable pricing mechanisms or supply diversification strategies emerge.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

6.74% |

|

Segments Covered |

By Product Type, Price Point, Application, Packaging, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

The Hain Celestial Group Inc., Archer Daniels Midland Company, Bunge Limited, Adani Wilmar Limited, Wichy Plantation Company Pvt Ltd (Bitumix Pvt Ltd), Windmill Organics Ltd, Marico Limited, and Cargill Corporation |

SEGMENTAL ANALYSIS

By Product Type Insights

The Coconut RBD oil segment dominated the Europe coconut oil market and accounted for a 64.8% share in 2025. Moreover, the dominance of RBD coconut oil is credited to the European processing sector where manufacturers prioritize cost efficiency, shelf stability, and versatility across diverse applications. This refined bleached and deodorized variant serves as the preferred choice for industrial food manufacturing, oleochemical production, and cosmetic formulation due to its neutral flavor, high smoke point, and consistent functional properties. Apart from these, a key contributor to the the dominance of Coconut RBD oil is its widespread adoption by industrial food manufacturers who require a neutral tasting fat that withstands high temperature processing without imparting coconut flavor to final products. RBD coconut oil offers a smoke point exceeding 232 degrees Celsius, creating it ideal for frying operations and thermal processing where virgin variants would degrade or alter sensory characteristics. The refining process reshifts impurities and free fatty acids, extfinishing shelf life and reducing the risk of rancidity during extfinished storage and distribution cycles. Food technologists value the predictable melting behavior and crystallization properties of RBD coconut oil, which enable precise control over texture in products like chocolate coatings, biscuit fillings, and plant based dairy alternatives. Additionally, the cost advantage of RBD oil over virgin variants allows manufacturers to manage input expenses while maintaining quality standards, a critical consideration in competitive European food markets where margin pressure remains intense. This functional reliability and economic efficiency ensure that RBD coconut oil remains the backbone of industrial lipid sourcing across the continent. An additional growth factor sustaining the leadership of Coconut RBD oil is its superior compatibility with oleochemical synthesis and cosmetic formulation processes that demand high purity and consistent chemical composition. The European oleochemical industest, which produces surfactants, emulsifiers, and fatty alcohols for detergents and personal care products, relies heavily on refined coconut oil as a feedstock due to its high lauric acid content and low impurity levels. In the cosmetics sector, RBD coconut oil serves as a stable base for soaps, lotions, and hair care products where color, odor, and oxidative stability are paramount. The refining process ensures compliance with stringent European regulatory limits on contaminants, reducing the burden of quality verification for downstream manufacturers. This alignment with industrial technical specifications and regulatory requirements solidifies the entrenched position of RBD coconut oil as the workhorse lipid across multiple European value chains.

The Virgin Coconut Oil segment is likely to experience the rapidest CAGR of 9.4% from 2026 to 2034 due to rising consumer demand for minimally processed, nutrient dense ingredients that align with clean label and wellness oriented purchasing behaviors across European retail and food service channels. Among these, one of the major factors supporting this growth is the intensifying consumer preference for products that retain natural nutrients, antioxidants, and authentic sensory characteristics associated with minimal processing. According to sources, a portion of shoppers in the region actively seek out cold pressed or unrefined oils perceived as healthier and more flavorful than their refined counterparts. Virgin Coconut Oil, extracted through mechanical pressing without chemical solvents or high heat, preserves medium chain triglycerides, polyphenols, and vitamin E compounds that appeal to health conscious demographics. Culinary enthusiasts and professional chefs value the distinctive tropical aroma and subtle sweetness of virgin variants, which enhance gourmet dishes, smoothies, and artisanal confectionery without requiring additional flavorings. Retailers have responded by expanding organic and fair trade virgin coconut oil assortments, often highlighting origin stories and traditional extraction methods to justify premium pricing. This convergence of nutritional awareness, sensory appreciation, and ethical consumption ensures that Virgin Coconut Oil captures disproportionate growth momentum despite its tinyer base volume compared to refined alternatives. A further reason for this growth is the robust expansion of the natural cosmetics and wellness product sector, which increasingly specifies Virgin Coconut Oil for its bioactive properties and marketing appeal among discerning European consumers. Virgin Coconut Oil contains lauric acid with documented antimicrobial properties and antioxidants that protect skin barrier function, creating it a coveted ingredient in premium skincare, haircare, and body care formulations. The rise of clean beauty shiftments and transparency initiatives compels manufacturers to disclose ingredient origins and processing methods, favoring virgin coconut oil suppliers who can provide traceable and ethically produced certifications. Additionally, the wellness tourism and spa industest across Southern and Eastern Europe incorporates virgin coconut oil in therapeutic treatments, further amplifying demand for authentic unrefined variants. European consumers are continuing to invest in self-care and holistic health solutions. Therefore, the strategic importance of Virgin Coconut Oil as a premium functional ingredient will sustain exceptional growth rates throughout the forecast period.

By Price Point Insights

The Mass price point segment led the Europe coconut oil market and captured a significant share in 2025. This position of the segment is attributed to the widespread adoption of coconut oil across mainstream retail channels, industrial food manufacturing, and value oriented personal care formulations where cost efficiency and volume accessibility remain paramount purchasing criteria. The primary engine behind the Mass segment’s leadership is the extensive penetration of coconut oil into mainstream retail formats including discount supermarkets, hypermarkets, and convenience stores across Europe. Private label coconut oil products, typically positioned at the Mass price point, have expanded rapidly as retailers seek to capture margin while offering affordable alternatives to branded items. Mass priced coconut oil benefits from economies of scale in sourcing, refining, and packaging that enable aggressive promotional pricing and multi pack offerings attractive to budobtain conscious houtilizeholds. Additionally, industrial food manufacturers sourcing coconut oil for private label ready meals, bakery items, and confectionery prioritize cost effective Mass grade inputs to maintain retail price competitiveness. The alignment of Mass coconut oil with value driven consumption patterns across diverse European demographics ensures its continued dominance in both houtilizehold and business to business procurement channels. In addition, this area is supported by the strategic emphasis on cost optimization by European industrial utilizers who procure coconut oil in bulk volumes for food processing, oleochemical synthesis, and mass market cosmetic production. According to research, industrial purchaseers consistently prioritize total cost of ownership over premium attributes when sourcing commodity ingredients, favoring Mass price point coconut oil that meets functional specifications without unnecessary expense. Large scale manufacturers leverage long term supply contracts and volume based pricing neobtainediations to secure stable input costs, a practice that inherently favors standardized Mass grade products over niche premium variants. The oleochemical and detergent industries, which consume significant volumes of coconut oil derivatives, operate on thin margins that necessitate careful raw material cost management. Mass priced RBD coconut oil offers the predictable quality and consistent supply reliability required for continuous production processes, minimizing downtime and quality control expenses. Additionally, the rise of value oriented personal care brands tarobtaining price sensitive consumers has increased demand for affordable coconut oil inputs that maintain acceptable performance without premium positioning. This industrial focus on procurement efficiency and margin protection ensures that the Mass price point segment remains the volume leader across the European coconut oil value chain.

The Premium price point segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 10.7% during the forecast period owing to escalating consumer willingness to pay for certified organic, ethically sourced, and specialty processed coconut oil variants that align with evolving lifestyle and values based purchasing decisions. The principal driver for the surge in Premium coconut oil sales is the growing affluence and values oriented consumption patterns among European shoppers who prioritize sustainability, health, and ethical provenance over price alone. Premium coconut oil brands leverage certifications such as EU Organic, Fairtrade International, and Rainforest Alliance to signal adherence to environmental and social standards that resonate with conscious purchaseers. Retailers have responded by dedicating premium shelf space to specialty coconut oil variants in health food stores, gourmet sections, and online marketplaces that cater to discerning demographics. The wellness and functional food shiftment further amplifies demand for cold pressed, unrefined, and virgin coconut oils perceived as nutritionally superior to mass market alternatives. As disposable incomes recover and sustainability concerns intensify across the continent, the Premium segment is positioned to capture disproportionate growth from consumers seeking alignment between purchasing power and personal values. Also, this sector is boosted by the continuous innovation in specialty formats and culinary applications that justify higher price points through enhanced functionality and sensory experiences. According to studies, gourmet food manufacturers and artisanal brands increasingly incorporate premium coconut oil variants into high finish confectionery, plant based dairy alternatives, and functional beverages that command premium retail pricing. Specialty formats such as infutilized virgin coconut oils with herbs, spices, or citrus extracts appeal to food enthusiasts seeking unique flavor profiles for home cooking and entertaining. The rise of food delivery platforms and meal kit services has created new channels for premium ingredient discovery, with curated boxes often featuring artisanal coconut oil products that introduce consumers to elevated culinary experiences. Additionally, the professional food service sector, including high finish restaurants and boutique hotels, specifies premium coconut oil for menu items where quality differentiation justifies menu price premiums. This convergence of product innovation, channel expansion, and experiential consumption ensures that Premium coconut oil captures accelerating growth momentum despite its niche positioning within the broader market.

By Application Insights

The Food Industest segment held the majority share of 58.9% of the Europe coconut oil market in 2025. A major factor that aids this segment is the extensive utilization of coconut oil across bakery, confectionery, dairy alternatives, and ready meal production where its functional properties, thermal stability, and cost efficiency align with industrial manufacturing requirements. One more point that adds strength is the widespread adoption of coconut oil in European bakery and confectionery manufacturing where its solid at room temperature properties and neutral flavor profile enable precise texture control and product consistency. According to sources, a notable share of industrial bakery formulations utilize coconut oil or its fractions to achieve desired crumb structure, shelf life extension, and mouthfeel in products ranging from biscuits and cakes to laminated pastries. Coconut oil’s melting point around 24 to 26 degrees Celsius allows it to remain solid during dough handling yet melt pleasantly during consumption, a critical attribute for chocolate coatings, biscuit fillings, and wafer applications. Food technologists value the predictable crystallization behavior of coconut oil, which enables manufacturers to optimize production parameters and reduce waste from texture defects. Additionally, the rise of plant based and dairy free product development has increased demand for coconut oil as a functional alternative to butter and palm oil in vegan bakery items. This combination of technical functionality, formulation flexibility, and alignment with clean label trfinishs ensures that the Food Industest remains the largest application segment for coconut oil across Europe. An added support for this segment comes from the accelerating expansion of plant based dairy and alternative protein formulations that rely on coconut oil for texture, mouthfeel, and nutritional profile enhancement. Coconut oil serves as a cornerstone ingredient in vegan butter, cheese analogues, ice cream substitutes, and whipped toppings due to its ability to mimic the melting behavior and richness of animal fats. Food manufacturers leverage coconut oils medium chain triglyceride content to enhance the nutritional profile of plant based products while delivering satisfying sensory experiences that drive repeat purchase. Additionally, the plant based meat sector utilizes coconut oil to improve juiciness and fat marbling in meat analogues, supporting the regions ambitious protein transition goals. Major food conglomerates are reformulating legacy products to include coconut oil as a clean label alternative to hydrogenated fats or palm oil derivatives, further expanding application scope. European policy frameworks are encouraging sustainable protein consumption and reducing reliance on animal agriculture. Consequently, the strategic importance of coconut oil in enabling delicious and nutritious plant-based options will continue to expand, securing the Food Industest segment’s dominant market position.

The Cosmetics and Personal Care Industest segment is expected to exhibit a noteworthy CAGR of 8.9% between 2026 and 2034. This accelerated expansion of the segment is fueled by rising consumer demand for natural, organic, and sustainably sourced ingredients in skincare, haircare, and body care formulations across European retail and professional channels. The foremost factor propelling the growth of the Cosmetics and Personal Care segment is the robust expansion of natural and organic cosmetic formulations that prioritize botanical oils like coconut oil for their emollient, antimicrobial, and sensory benefits. Coconut oil serves as a fundamental base ingredient in soaps, lotions, hair conditioners, and lip care products due to its ability to enhance skin barrier function and deliver a luxurious sensory experience. Consumer preference for clean beauty products free from synthetic chemicals and microplastics further amplifies demand for coconut oil as a renewable and biodegradable alternative. Additionally, the rise of transparency initiatives and ingredient traceability requirements compels manufacturers to disclose sourcing origins, favoring suppliers who can provide certified sustainable and ethically produced coconut oil. As European consumers continue to invest in self care and wellness oriented products, the cosmetic industest’s reliance on coconut oil as a functional and marketing asset will sustain exceptional growth trajectories for the foreseeable future. This segment is also shaped by the continuous innovation in multifunctional and tarobtained skincare solutions that leverage coconut oils bioactive properties to address specific consumer concerns such as hydration, anti aging, and sensitive skin care. Coconut oils lauric acid content provides antimicrobial benefits valuable in acne prone and sensitive skin formulations, while its antioxidant compounds assist protect against environmental stressors. The rise of dermocosmetic and pharmacy channel brands has increased demand for high purity coconut oil variants that meet stringent quality and safety standards for therapeutic applications. Additionally, the professional spa and wellness industest across Southern and Eastern Europe incorporates coconut oil in therapeutic treatments, further amplifying demand for authentic and ethically sourced variants. This convergence of scientific validation, product innovation, and channel expansion ensures that the Cosmetics and Personal Care segment captures accelerating growth momentum within the European coconut oil market.

By Packaging Insights

The Bottle packaging segment was the largest segment in the Europe coconut oil market and occupied a 43.6% share in 2025 becautilize of accounting for an estimated 43 percent of total packaging volume. This dominance reveals the widespread consumer preference for convenient, resealable, and portion controlled formats that align with houtilizehold usage patterns and retail shelf optimization strategies across European markets. Along with this, the segment is driven by the strong consumer preference for convenient, simple to pour, and resealable packaging formats that support precise portion control and minimize product waste in houtilizehold settings. Bottle formats, typically manufactured from PET or glass, enable consumers to dispense coconut oil in controlled amounts for cooking, baking, or topical application without mess or spillage. The transparency of clear bottles allows visual verification of product quality and remaining volume, enhancing purchase confidence and repeat purchaseing behavior. Retailers favor bottle packaging for its stackability, shelf stability, and compatibility with automated filling lines, which reduce handling costs and optimize warehoutilize space utilization. Additionally, bottle formats support premium branding opportunities through label design, shape differentiation, and tamper evident features that justify higher price points in competitive retail environments. The alignment of bottle packaging with consumer convenience expectations and retail operational efficiency ensures its continued dominance across both mass and premium coconut oil segments throughout Europe. Beyond that, the segment is supported by the packaging industest’s successful adaptation to European regulatory requirements and sustainability mandates while maintaining the functional advantages of bottle formats. Bottle manufacturers have responded by developing lightweight PET designs with high recycled content, glass options with returnable systems, and bio based plastic alternatives that comply with evolving environmental standards. Additionally, bottle formats facilitate clear communication of mandatory information including nutritional facts, allergen warnings, and sustainability certifications that build consumer trust and regulatory compliance. The versatility of bottle packaging enables brands to offer multiple size options ranging from 250 milliliter trial packs to 1 liter family formats, catering to diverse houtilizehold requireds and purchase occasions. This combination of regulatory alignment, sustainability innovation, and format flexibility ensures that Bottle packaging remains the preferred choice for coconut oil brands seeking market access and consumer acceptance across European retail channels.

The Pouch packaging segment is predicted to witness the highest CAGR of 12.3% during the forecast period. This rapid growth is propelled by escalating demand for lightweight, space efficient, and cost effective packaging solutions that align with e commerce logistics, sustainability goals, and value oriented consumer preferences. Following that, this segment is also driven by the swift expansion of e commerce and direct to consumer sales channels that prioritize lightweight, compact, and damage resistant packaging formats for efficient shipping and handling. Pouch formats, typically manufactured from flexible laminates, reduce package weight compared to rigid bottles, lowering freight costs and carbon emissions associated with transportation. The flat profile of filled pouches enables denser palletization and warehoutilize storage, maximizing space utilization throughout the supply chain. Additionally, pouch packaging supports innovative dispensing features such as spouts, zippers, and stand up designs that enhance utilizer convenience while maintaining product protection. As European consumers continue to embrace online shopping for pantest staples and houtilizehold essentials, the strategic advantages of pouch packaging for e commerce fulfillment will sustain exceptional growth momentum throughout the forecast period. A further reason for this growth of the segment is its superior sustainability profile and alignment with European circular economy objectives that prioritize material reduction, recyclability, and carbon footprint minimization. Pouch manufacturers have invested in mono material designs and recyclable laminate structures that comply with emerging European packaging regulations while maintaining barrier properties essential for coconut oil preservation. Additionally, pouch packaging enables brands to offer refill systems and concentrated formats that further reduce material utilize and transportation emissions. The rise of zero waste retail concepts and bulk dispensing stations in European supermarkets has created new opportunities for pouch based coconut oil products that support package free shopping experiences. This convergence of regulatory alignment, material innovation, and consumer values ensures that Pouch packaging captures accelerating growth momentum within the European coconut oil market despite its niche positioning relative to traditional rigid formats.

REGIONAL ANALYSIS

Germany Coconut Oil Market Analysis

Germany was the top performer in the Europe coconut oil market and captured a 24.8% share in 2025. The dominance of the German market is attributed to its massive domestic consumption, advanced food processing sector, and strong retail infrastructure. The German market is characterized by high consumer awareness of health and wellness trfinishs, robust demand for plant based alternatives, and stringent quality expectations that drive premiumization across coconut oil categories. A key driving factor is the size and sophistication of the German food manufacturing industest, which extensively utilizes coconut oil in bakery, confectionery, and dairy alternative production for both domestic consumption and export markets. Additionally, Germany’s retail landscape is dominated by large discount and hypermarket chains that drive high volumes of both mass and premium coconut oil sales through aggressive promotional strategies and private label expansion. The German consumer’s strong interest in organic and sustainable products. This combination of industrial demand, retail scale, and values oriented consumption secures Germany’s top position in the regional coconut oil market.

United Kingdom Coconut Oil Market Analysis

The United Kingdom was the next prominent countest in the Europe coconut oil market and occupied a 18.9% share in 2025. Factors such as its mature retail sector, strong wellness culture, and dynamic food innovation ecosystem drive the growth of the UK market. The British market is unique due to its high penetration of plant based products, robust e commerce infrastructure, and consumer willingness to experiment with international ingredients. A primary driver is the rapid expansion of the UK’s plant based food sector, which extensively utilizes coconut oil in dairy alternatives, meat analogues, and functional snacks tarobtaining flexitarian and vegan demographics. According to the Plant-based Food Alliance UK, the market for plant-based products has seen steady expansion as consumers increasingly integrate meat and dairy alternatives into their daily diets. Coconut oil continues to be a featured ingredient in new product development, valued by manufacturers for its unique functional properties in creating plant-based fats and textures. Furthermore, the UK’s sophisticated e commerce and direct to consumer channels have accelerated adoption of premium and specialty coconut oil variants, with online sales of edible oils increasing. The British consumer’s strong interest in wellness and self care, reflected in the growth of the natural cosmetics sector, further amplifies demand for coconut oil in personal care applications. Additionally, the UK’s position as a global culinary hub drives demand for versatile cooking fats like coconut oil in both professional and home kitchens. This convergence of food innovation, digital retail, and wellness trfinishs sustains the United Kingdom’s prominent market position.

France Coconut Oil Market Analysis

France continues to be a significant contributor to the Europe coconut oil market due to its strong cosmetic and personal care manufacturing base, gourmet food culture, and growing interest in natural wellness products. The French market is deeply intertwined with its global reputation for beauty and luxury goods, where coconut oil serves as a valued ingredient in premium skincare and haircare formulations. The primary catalyst for the market here is the robust French cosmetics industest, which represents one of the largest globally and extensively utilizes coconut oil for its emollient and sensory properties. Another significant factor is the French consumer’s increasing interest in plant based and functional foods, with organic food sales growing annually. Coconut oil benefits from this trfinish as a versatile ingredient in bakery, confectionery, and dairy alternative applications that align with clean label preferences. Additionally, France’s strong culinary heritage and gourmet retail sector drive demand for premium virgin and specialty coconut oil variants utilized in artisanal cooking and high finish food products. The countest’s commitment to sustainability and ethical sourcing, reflected in growing Fairtrade and organic certification adoption, further supports market growth for responsibly produced coconut oil. This combination of cosmetic leadership, culinary innovation, and values driven consumption secures France’s strong position in the regional market.

Netherlands Coconut Oil Market Analysis

The Netherlands grew steadily in the Europe coconut oil market by leveraging its status as a global logistics hub, advanced food processing sector, and strong commitment to sustainable trade practices. Although tinyer in population compared to Germany or France, the Netherlands punches above its weight due to its strategic port infrastructure and role as a key entest point for coconut oil imports into the European Union. The primary driver is the countest’s function as a major re export hub for edible oils, with the Port of Rotterdam handling a portion of Europe’s coconut oil imports. This logistical advantage enables efficient distribution to neighboring markets while supporting domestic processing and value addition activities. The highly advanced Dutch food manufacturing sector, particularly in bakery, confectionery, and plant based alternatives, utilizes coconut oil for its functional properties and clean label appeal. Additionally, the Netherlands’ strong commitment to sustainability and circular economy principles drives demand for certified organic, fair trade, and recyclable packaging coconut oil variants. The Dutch consumer’s high awareness of health and environmental issues, with a portion regularly purchasing organic products according to the Netherlands Nutrition Centre, further amplifies market growth. This combination of logistical leadership, industrial demand, and sustainability focus ensures the Netherlands’ prominent role in the European coconut oil value chain.

Italy Coconut Oil Market Analysis

Italy is predicted to expand notably in the Europe coconut oil market over the forecast period due to its strong cosmetic manufacturing base, gourmet food culture, and growing interest in natural wellness solutions. The Italian market is deeply influenced by its global reputation for beauty, fashion, and culinary excellence, where coconut oil serves as a valued ingredient across multiple premium applications. A major driving force is the robust Italian cosmetics and personal care industest, which extensively utilizes coconut oil in skincare, haircare, and body care formulations tarobtaining both domestic and export markets. Furthermore, Italy’s strong culinary heritage and artisanal food production drive demand for high quality coconut oil in gourmet confectionery, bakery, and specialty food applications. Additionally, Italy’s position as a leading tourism destination creates opportunities for coconut oil based wellness and spa products that cater to international visitors seeking authentic Mediterranean experiences. The countest’s commitment to sustainability and geographical indication protections also supports market growth for ethically sourced and traditionally produced coconut oil variants. This convergence of cosmetic leadership, culinary innovation, and wellness tourism sustains Italy’s strong position in the regional coconut oil market.

COMPETITIVE LANDSCAPE

The competition in the Europe coconut oil market is characterized by intense rivalry among multinational agribusiness giants and specialized regional processors who vie for dominance through quality and sustainability credentials. Major players leverage their extensive global supply networks to ensure consistent availability and price stability which are critical for retaining large industrial contracts. The market sees frequent innovation in product formulations as companies strive to meet the specific requireds of the rapidly growing plant based food and natural cosmetic sectors. Regulatory compliance acts as a significant differentiator with firms investing heavily in traceability systems to adhere to European deforestation and due diligence laws. Price volatility in raw materials often leads to aggressive hedging strategies and long term supply agreements to protect margins. Private label offerings from major retailers add pressure on branded manufacturers to justify premium pricing through superior quality or ethical sourcing stories. Mergers and acquisitions are common tactics utilized to consolidate market share and gain access to new technologies or distribution channels. This dynamic environment forces continuous adaptation and strategic investment to maintain relevance and profitability in a highly discerning European marketplace.

KEY MARKET PLAYERS

Some of the notable key players in the Europe coconut oil market are

- The Hain Celestial Group, Inc.

- Archer Daniels Midland Company

- Bunge Limited

- Adani Wilmar Limited

- Wichy Plantation Company (Pvt) Ltd (Bitumix (Pvt) Ltd)

- Windmill Organics Ltd

- Marico Limited

- Cargill Corporation

Top Players in the Market

- IOI Loders Croklaan operates as a global leader in specialty fats and oils with a significant footprint in the Europe coconut oil market. The company supplies high quality refined and fractionated coconut oils to major food manufacturers and cosmetic brands across the continent. Their contribution to the global market involves pioneering sustainable sourcing initiatives and advanced enzymatic interesterification technologies. Recently the company strengthened its position by expanding its production capacity in the Netherlands to meet rising European demand for clean label ingredients. They actively collaborate with suppliers in Southeast Asia to ensure traceability and compliance with new European deforestation regulations. Their focus on innovation allows them to create tailored fat solutions that mimic dairy textures in plant based products. This strategic emphasis on sustainability and technical expertise solidifies their role as a preferred partner for European industries seeking reliable and responsible coconut oil supplies.

- AAK AB stands as a prominent Swedish veobtainable oil specialist that plays a crucial role in the Europe coconut oil market through its extensive portfolio of customized lipid solutions. The company serves diverse sectors including confectionery, bakery, and personal care by providing coconut oil variants with specific melting profiles and functional characteristics. Globally AAK is recognized for its value chain optimization and commitment to zero deforestation goals which resonate strongly with European purchaseers. Recent actions to strengthen their market position include investing in new refining technologies at their European facilities to improve efficiency and reduce environmental impact. They have also formed strategic partnerships with coconut farmers to enhance livelihoods and secure long term supply stability. Their ability to offer bespoke formulations assists clients achieve superior product performance while adhering to strict European quality standards. This dedication to customization and sustainability ensures their continued influence and growth within the competitive European landscape.

- Wilmar International functions as a massive agribusiness group with a substantial presence in the Europe coconut oil market via its integrated supply chain and trading networks. The company imports vast volumes of coconut oil from tropical regions and processes them in European refineries to serve food service and industrial clients. Their global contribution includes maintaining one of the most extensive palm and lauric oil logistics networks which ensures consistent availability even during market fluctuations. To strengthen their European position Wilmar recently enhanced its sustainability certification programs to align with evolving European Union due diligence laws. They have also expanded their distribution capabilities to reach tinyer regional manufacturers who require flexible supply terms. Their investment in digital tracking systems provides transparency from farm to fork which builds trust among conscious European consumers. By leveraging their scale and logistical prowess Wilmar effectively mitigates supply risks and offers competitive pricing strategies that attract large scale industrial purchaseers across the region.

Top Strategies Used by Key Market Participants

Key players in the Europe coconut oil market primarily focus on sustainability and supply chain transparency to maintain competitiveness. Companies actively invest in certification schemes such as organic and fair trade to meet stringent European regulatory requirements and consumer expectations. Vertical integration is a common strategy where firms acquire upstream assets or form direct partnerships with farmers to secure raw material supplies and control costs. Product innovation drives growth as manufacturers develop specialized fractions and blfinishs tailored for plant based foods and natural cosmetics. Expansion of production facilities within Europe allows players to reduce logistics costs and improve delivery speed to local clients. Strategic collaborations with research institutions assist in creating novel applications for coconut oil in health and wellness sectors. Digitalization of procurement processes enhances efficiency and provides real time data on inventory and sourcing origins. These combined approaches enable market leaders to navigate complex regulatory landscapes while capturing emerging opportunities in green and healthy product segments.

MARKET SEGMENTATION

This research report on the European coconut oil market has been segmented and sub-segmented based on categories.

By Product Type

- Virgin Coconut Oil

- Coconut RBD Oil

By Price Point

By Application

- Food industest

- Agriculture

- Cosmetics & personal care industest

- Chemical Industest

- Others

By Packaging

- Bottle

- Jar

- Can

- Pouch

- Tanks

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe