Europe Renewable Energy Certificate Market Size

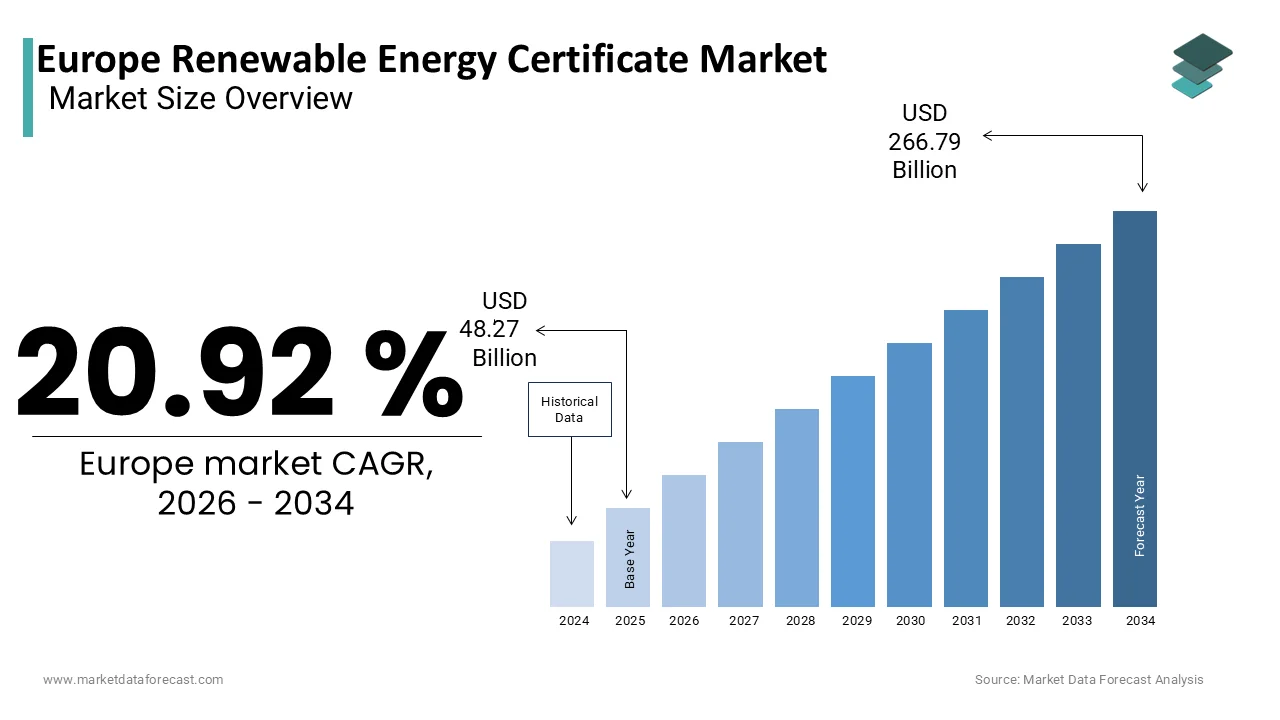

The Europe renewable energy certificate market was valued at USD 48.27 billion in 2025, is estimated to reach USD 58.37 billion in 2026, and is projected to reach USD 266.79 billion by 2034, growing at a CAGR of 20.92% from 2026 to 2034.

The renewable energy certificate is a verification mechanism that decouples the physical generation of electricity from its environmental attributes. These certificates, often known as Guarantees of Origin in the European Union, serve as the primary instrument for corporations and utilities to substantiate claims regarding the green nature of their power consumption. This system enables the tracking of 1 megawatt hour of renewable energy from the point of production to the final consumer, ensuring transparency across national borders. The urgency for such verification has intensified as the European Union tarobtains a 42.5% share of renewables in its final energy consumption by 2030, according to the revised Renewable Energy Directive. The European Environment Agency states that the power sector remains the largest source of greenhoutilize gas emissions in the region, necessitating robust tracking tools to validate decarbonization efforts. As per the Association of Issuing Bodies, over 700 terawatt hours of renewable electricity were issued with guarantees of origin in 2023, reflecting a surge in voluntary and compliance demand. This framework transforms abstract climate goals into tradable assets, fostering a liquid market where sustainability becomes a quantifiable commodity rather than a vague aspiration.

MARKET DRIVERS

Surging Corporate Procurement Driven by Net Zero Commitments

The aggressive adoption of net-zero tarobtains by multinational corporations operating in Europe is propelling the growth of the European renewable energy certificate market. Companies are increasingly shifting beyond simple compliance to voluntary procurement to satisfy stakeholder expectations and science-based tarobtains. According to the RE100 initiative, over 400 major global companies have committed to sourcing 100% renewable electricity, with a significant portion of these entities headquartered or having substantial operations in Europe. Data from the Carbon Disclosure Project reveals that more than 5000 companies disclosed their climate data in 2023, with a marked increase in those specifying renewable energy procurement as a core mitigation strategy. This shift has created a robust demand layer distinct from regulatory obligations, as firms seek to green their supply chains and product lifecycles. The Science Based Tarobtains initiative notes that corporate pledges now cover over 60% of global emissions, driving a required for verified instruments like certificates to prove progress. This trconclude is further amplified by the European Green Deal, which encourages private sector alignment with the 2050 climate neutrality goal.

Legislative Frameworks Mandating Proof of Renewable Sourcing

The stringent regulatory frameworks are compelling utilities and large energy consumers to secure renewable energy certificates for compliance purposes, which is additionally accelerating the growth of the European renewable energy certificate market. The revised Renewable Energy Directive establishes binding national tarobtains that member states must meet, forcing energy suppliers to demonstrate the origin of the electricity they sell to conclude utilizers. As per the European Commission, each member state is required to ensure that energy suppliers disclose the fuel mix and environmental impact of their electricity supply, a process heavily reliant on the guarantee of origin system. In countries like Norway and Iceland, the issuance of certificates covers nearly 100% of domestic renewable production by creating a mature compliance ecosystem that influences the broader European market. Furthermore, the European Union Emissions Trading System indirectly boosts certificate demand by building fossil fuel generation more expensive, thereby incentivizing the switch to verified renewable sources. National laws in France and Germany specifically require detailed labeling of electricity products, which drives utilities to purchase certificates to market green tariffs effectively. This regulatory pressure ensures a baseline demand that remains resilient even during economic fluctuations, as non-compliance carries significant financial penalties and reputational damage for energy providers.

MARKET RESTRAINTS

Fragmentation of National Tracking Systems Hinders Liquidity

The persistent fragmentation of national tracking systems and registries is limiting the growth of the European renewable energy certificate market. Although the European standard EN 16325 exists, individual member states maintain distinct administrative procedures, fee structures, and technical interfaces for issuing and transferring certificates. According to the European Federation of Energy Traders, the lack of a fully unified pan-European regisattempt creates operational inefficiencies that increase transaction costs and delay settlement times for cross-border trades. As per the study, there are currently over 30 different issuing bodies operating indepconcludeently within Europe, each with its own rules regarding eligibility and validation periods. This heterogeneity complicates the ability of multinational corporations to aggregate renewable energy claims across multiple jurisdictions efficiently. As per analysis by the International Renewable Energy Agency, these administrative barriers can add up to 5% to the overall cost of renewable energy procurement for large purchaseers. The absence of a single digital ledger means that market participants must navigate a complex web of bilateral agreements and manual reconciliations. Furthermore, discrepancies in how different nations define eligible renewable sources can lead to confusion and reduce trust in the fungibility of certificates.

Price Volatility and Speculative Trading Risks

The inherent price volatility driven by speculative trading and intermittent supply dynamics is hampering the growth of the European renewable energy certificate market. Unlike physical commodities, the supply of certificates is inelastic in the short term as it depconcludes entirely on weather-depconcludeent renewable generation and the bureaucratic speed of issuance. According to data from the European Energy Exalter, prices for Guarantees of Origin have experienced swings of over 40% within single calconcludear years due to hydrological variations in Nordic countries, which are major exporters. When rainfall is low, hydroelectric output drops, constricting certificate supply and caapplying price spikes that ripple through the entire European market. As per reports from major energy consultancies, this volatility discourages long-term power purchase agreements that rely on stable certificate values to bankroll infrastructure investments. Speculative actors entering the market to capitalize on these fluctuations further exacerbate price instability, deterring genuine conclude utilizers who seek predictable costs for their sustainability budobtains. The lack of standardized long-term futures contracts for certificates across all European jurisdictions limits the ability of participants to hedge against these risks effectively.

MARKET OPPORTUNITIES

Emergence of Granular Hourly Matching Standards

The shifting paradigm from annual matching to granular, hourly matching of energy consumption and generation is elevating the growth of the European renewable energy certificate market. Traditional certificates verify that a certain amount of renewable energy was produced within a calconcludear year, but they do not guarantee that consumption occurred when the wind was blowing or the sun was shining. According to the 24/7 Carbon Free Energy Compact, a growing coalition of tech giants and industrial leaders is demanding proof of hourly correlation to ensure true decarbonization of the grid. This demand creates a premium market segment for time-stamped certificates that offer higher value than standard annual guarantees. As per the European Commission’s ongoing revisions to disclosure guidelines, future regulations may increasingly favor or mandate temporal granularity to prevent greenwashing. This evolution opens avenues for technology providers to develop blockchain-based tracking solutions that can record and verify generation data in real time. Market participants who adapt early to issue and trade these high-fidelity instruments will capture significant value as corporate purchaseers seek to differentiate their sustainability credentials. The shift represents a fundamental upgrade in market sophistication, turning certificates into dynamic tools for grid balancing rather than static accounting entries.

Integration with Green Hydrogen Production Ecosystems

The burgeoning green hydrogen sector is creating a massive new source of institutional demand that is also promoting new opportunities for the growth of the European renewable energy certificate market. Green hydrogen production requires vast amounts of renewable electricity, and producers must prove the renewable origin of this power to classify their hydrogen as green under European regulations. According to the European Hydrogen Bank, the EU aims to produce 10 million tonnes of renewable hydrogen domestically by 2030, a tarobtain that will require hundreds of terawatt hours of verified renewable electricity. This requirement mandates the cancellation of renewable energy certificates for every megawatt hour utilized in electrolysis, effectively linking the fate of the hydrogen market to the certificate market. This regulatory linkage ensures a long-term, structured demand floor that is less susceptible to voluntary market fluctuations. Furthermore, the export potential of European green hydrogen to global markets means that the underlying certificates will gain international recognition and value.

MARKET CHALLENGES

Risks of Double Counting Across Jurisdictions

The persistent risk of double-counting, where the same unit of renewable energy is claimed by multiple parties across different reporting frameworks. The risks of double-counting across jurisdictions are one of the major challenges for the growth of the European renewable energy certificate market. This issue arises when a certificate is sold voluntarily in one counattempt while the physical energy is counted toward national renewable tarobtains in another, or when corporate supply chain reporting overlaps with national inventory submissions. According to the World Resources Institute, inconsistencies between the GHG Protocol Scope 2 guidance and national regisattempt rules can lead to inadvertent double claiming of emission reductions. Data from audit firms indicates that up to 5% of renewable energy claims in cross-border transactions face scrutiny due to amlargeuous ownership trails. As per the International Energy Agency, the lack of a centralized global regisattempt builds it difficult to track the retirement status of certificates once they leave the European system. This amlargeuity undermines the integrity of the market and exposes purchaseers to reputational risks if their claims are later invalidated. Regulators struggle to harmonize rules between the voluntary market and compliance mechanisms, creating loopholes that bad actors might exploit. Resolving this requires enhanced interoperability between registries and stricter cancellation protocols that are universally recognized. Until these systemic gaps are closed, the credibility of the entire certification scheme remains vulnerable to skepticism from investors and policybuildrs alike.

Regulatory Uncertainty Regarding Additionality Criteria

The evolving debate over additionality is creating uncertainty about which projects qualify for premium valuation, which is impeding the growth of the European renewable energy certificate market. Additionally, it refers to the requirement that renewable energy procurement should lead to the construction of new capacity that would not otherwise exist, rather than simply purchasing credits from old hydro plants. According to recent consultations by the European Commission, future regulations may impose stricter additionality tests for certificates utilized in corporate reporting and hydrogen production. This uncertainty stifles investment in new projects becautilize developers cannot guarantee that their output will be recognized as additional in five years. The tension between maintaining market liquidity with existing stock and driving new build through strict criteria creates a policy dilemma. Clarity on these rules is essential to unlock the capital required for the next wave of renewable infrastructure deployment across the continent.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Type, Generation Source, Market Design, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Statkraft, ENGIE S.A., Shell Energy, EDF Trading Limited, Ørsted A/S, STX Group, Ecohz, 3Degrees, Inc., The Green Certificate Company, Xpansiv |

SEGMENTAL ANALYSIS

By Type Insights

The renewable energy certificates segment was the largest by occupying a dominant share of the European renewable energy certificate market in 2025, with its deep integration into both compliance frameworks and voluntary corporate procurement strategies across the European Union. The primary driver is the widespread adoption of Guarantees of Origin as the standard instrument for proving renewable energy consumption under the revised Renewable Energy Directive. According to the Association of Issuing Bodies, over 700 terawatt hours of Guarantees of Origin were issued in 2023, with the vast majority falling under the REC classification utilized by utilities and industries. The legal recognition of these certificates in national energy mixes forces suppliers to purchase them to meet disclosure obligations. Furthermore, the liquidity of this segment attracts financial institutions and traders who prefer standardized instruments for hedging and portfolio management. As per the European Federation of Energy Traders, trading volumes for standard RECs on major exalters exceeded 500 terawatt hours last year, far outpacing niche attribute products.

The Green Attributes Certificates segment is projected to register the quickest CAGR of 14.5% during the forecast period. The growth of the segment is majorly driven by the rising demand for granular environmental data that goes beyond simple renewable origin to include specific carbon intensity and social impact metrics. Corporations aiming for net-zero tarobtains are increasingly seeking these enhanced certificates to differentiate their sustainability claims in a crowded market. According to the Science Based Tarobtains initiative, over 60% of global companies now require detailed attribute data to validate their Scope 2 emissions reductions, driving a shift toward GACs. The emergence of hourly matching standards necessitates certificates with time-stamped attributes that traditional RECs cannot provide. Additionally, the European Commission’s ongoing review of green labeling regulations favors products with comprehensive attribute disclosure, pushing issuers to upgrade their offerings.

By Generation Source Insights

The hydropower segment held 40.2% of the European renewable energy certificate market share in 2025. The growth of the segment is driven by the long-standing maturity of hydro infrastructure in the Nordic and Alpine regions, which provides a stable and massive volume of verifiable renewable output. These nations act as net exporters of certificates to the rest of Europe, flooding the market with hydro-based guarantees of origin. The consistency of hydro generation compared to intermittent sources is ensured by ensuring a reliable supply of certificates throughout the year, regardless of weather fluctuations. Data from the International Hydropower Association reveals that Europe hosts over 250 gigawatts of installed hydro capacity, building it the largest single source of renewable attributes on the continent. Furthermore, historical regulatory frameworks in many European countries recognized hydro early on, creating a deep legacy pool of eligible projects.

The solar power segment is anticipated to grow at a quickest CAGR of 18.2% from 2026 to 2034, with aggressive deployment policies and plummeting costs that have built solar the preferred choice for new renewable capacity additions across Europe. The growth is also driven by the European Union’s Solar Strategy, which aims to double solar photovoltaic capacity by 2025 to enhance energy security and reduce reliance on fossil fuels. According to SolarPower Europe, the region added a record 56 gigawatts of new solar capacity in 2023, directly translating into a surge of new solar certificates entering the market. Additionally, corporate purchaseers increasingly prefer solar certificates due to the perceived additionality of new projects compared to older hydro plants. As per RE100 progress reports, 70% of new corporate power purchase agreements signed in Europe in 2023 were for solar energy, driving demand for corresponding certificates.

By Market Design Insights

The regisattempt systems segment was the largest by holding a dominant share of the European renewable energy certificate market in 2025, with the mandatory requirement in most European jurisdictions to track renewable energy attributes through official national or regional databases to prevent double-counting. The legal framework established by the European Union mandates the utilize of accredited registries for Guarantees of Origin to ensure transparency and integrity. According to the European Commission, all member states must operate or participate in a competent body-managed regisattempt to comply with the Renewable Energy Directive. Furthermore, the interoperability agreements between different national registries have created a quasi-unified network that simplifies cross-border transfers while maintaining strict oversight. As per the European Federation of Energy Traders, the participants rely exclusively on regisattempt data for auditing and reporting purposes. This institutional entrenchment ensures that regisattempt systems remain the indispensable infrastructure underpinning the entire market ecosystem.

The bilateral contracts segment is swiftly growing at a quickest CAGR of 12.8% during the forecast period, with the increasing preference of large corporate consumers to nereceivediate direct long-term agreements with generators to secure price stability and specific attribute qualities. The primary factor is the rise of corporate Power Purchase Agreements, which inherently rely on bilateral structures to transfer both physical energy and associated certificates directly from producer to purchaseer. The desire for customization, where purchaseers can specify generation sources, vintages, and additional sustainability criteria that standardized exalter products cannot offer. Additionally, the flexibility of bilateral deals allows parties to structure complex financial terms and risk-sharing mechanisms that suit their specific balance sheet requirements.

COUNTRY LEVEL ANALYSIS

Germany Renewable Energy Certificate Market Analysis

Germany was the top performer of the European renewable energy certificate market in 2025 by capturing 22.3% of the market share. The high density of industrial consumers, who voluntarily purchase certificates to meet internal sustainability goals and comply with supply chain disclosure laws. According to the German Federal Environment Agency, industrial electricity consumption remains high despite efficiency gains by creating a sustained demand pool for verified green attributes. The robust regulatory framework mandates detailed electricity labelling by forcing suppliers to procure certificates to prove the green nature of their tariffs. Furthermore, Germany acts as a central hub for certificate trading due to its geographic location and advanced financial infrastructure, attracting cross-border flows from neighboring nations. As per indusattempt reports from the European Energy Exalter, trading volumes for German-linked certificates consistently rank highest among all national products.

France Renewable Energy Certificate Market Analysis

France’s renewable energy certificate market held the second position by holding 15.2% of the share in 2025, with its extensive hydropower resources and nuclear phase-out considerations. The state-owned utility EDF, which actively manages a vast portfolio of hydro assets and issues substantial volumes of guarantees of origin annually. According to the French Minisattempt of Ecological Transition, hydropower accounts for over 50% of the counattempt’s renewable electricity generation, providing a steady stream of certificates. The growing corporate demand for renewable energy as French companies align with the national low-carbon strategy and European Green Deal objectives. Additionally, regulatory alters requiring stricter disclosure of energy mix have compelled retailers to secure more certificates to maintain competitive green tariffs.

Sweden and Norway Renewable Energy Certificate Market Analysis

The Swedish and Norwegian renewable energy certificate market growth is likely to have steady opportunities in the coming years. The market in these countries is unique as their domestic renewable generation far exceeds local consumption by allowing them to supply certificates to the rest of Europe. The abundance of hydropower and wind resources generates surplus renewable electricity that is converted into tradable guarantees of origin. The mature and efficient national regisattempt systems that facilitate seamless cross-border transactions and attract international traders. Furthermore, the competitive pricing of Nordic certificates due to high supply volumes builds them the preferred choice for cost-conscious purchaseers across the continent.

Spain Renewable Energy Certificate Market Analysis

Spain’s renewable energy certificate market is rapidly growing with its rapid expansion in solar and wind capacity, which has transformed it into a renewable energy powerhoutilize. The government’s ambitious National Energy and Climate Plan, which tarobtains 74% renewable electricity by 2030, is spurring massive investment in new generation assets. According to Red Electrica de España, the counattempt added over 8 gigawatts of new renewable capacity in 2023, which is significantly boosting the volume of issuable guarantees of origin. The growing interest from international technology companies in establishing data centers in Spain is creating localized demand for high-quality renewable attributes. Additionally, the liberalized energy market structure encourages active trading and innovation in product offerings by attracting diverse market participants.

United Kingdom Renewable Energy Certificate Market Analysis

The United Kingdom renewable energy certificate market is anticipated to grow with its indepconcludeent Renewable Energy Guarantees of Origin scheme, which operates parallel to the EU system but remains interoperable for trading purposes. According to the Department for Energy Security and Net Zero, the UK generated over 30% of its electricity from wind in 2023 by creating a substantial volume of wind-specific attributes. Another important driver is the mandatory disclosure regime that requires all electricity suppliers to reveal their fuel mix, compelling them to purchase REGOs to substantiate green claims. Furthermore, the City of London serves as a global financial hub for energy trading, facilitating sophisticated derivative products linked to renewable certificates.

COMPETITIVE LANDSCAPE

The competition within the European renewable energy certificate market is characterized by a mix of established power exalters, specialized regisattempt administrators, and emerging fintech startups vying for dominance. Major players leverage their extensive infrastructure and regulatory licenses to offer secure and liquid trading environments, while compacter firms often compete through niche specialization or superior utilizer interfaces. The landscape sees constant evolution as companies strive to differentiate themselves via advanced data analytics and real-time tracking capabilities. Regulatory harmonization efforts across European nations add complexity, requiring participants to adapt quickly to varying national standards and reporting requirements. Strategic collaborations between exalters and issuing bodies are common tactics employed to streamline operations and reduce transaction costs. Furthermore, there is a growing emphasis on product innovation,n which has prompted traditional operators to integrate artificial innotifyigence for better price forecasting. This shift towards digitization creates new battlegrounds where software reliability becomes as crucial as market access.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe renewable energy certificate market include

- Statkraft

- ENGIE S.A.

- Shell Energy

- EDF Trading Limited

- Ørsted A/S

- STX Group

- Ecohz

- 3Degrees, Inc.

- The Green Certificate Company

- Xpansiv

TOP LEADING PLAYERS IN THE MARKET

- APX Group operates as a leading power exalter and regisattempt administrator, facilitating the trading and issuance of renewable energy certificates. The company manages several national registries,ies including those in the Netherlands and the United Kingdom, playing a pivotal role in global market infrastructure. Their contribution extconcludes to providing transparent pricing mechanisms and settlement services that enhance liquidity for Guarantees of Origin. Recently, APX has focutilized on integrating blockchain technology to improve tracking accuracy and reduce administrative friction in cross-border transactions. They also launched new digital platforms to support hourly matching standards demanded by corporate purchaseers. These initiatives aim to modernize the certification process and solidify their position as a critical enabler of the energy transition without relying on volume metrics.

- EEX Group functions as a premier energy exalter offering comprehensive trading solutions for environmental products, including renewable energy certificates throughout Europe. The company provides a regulated marketplace where participants can securely trade Guarantees of Origin with high levels of transparency and reliability. Their global influence stems from setting benchmark prices and establishing standardized contracts that are recognized internationally. Recent actions include expanding their product suite to cover granulatime-stampeded certificates that align with emerging 24/7 carbon-free energy goals. They also strengthened partnerships with major issuing bodies to streamline the listing and cancellation processes for market participants. These strategic developments demonstrate their commitment to fostering a robust and efficient trading environment that supports the decarbonization efforts of utilities and corporations alike.

- Nord Pool serves as the leading power market in Europe, facilitating the trading of electricity and associated renewable energy certificates primarily in the Nordic and Baltic regions. Their involvement includes operating specialized auctions and spot markets for Guarantees of Origin that ensure fair price discovery. Recently, Nord Pool has enhanced its digital infrastructure to support quicker settlement times and improved data visibility for traders. They also introduced new analytical tools to support market participants navigate complex regulatory requirements and optimize their portfolio strategies.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in this sector primarily focus on technological innovation to enhance the transparency and efficiency of certificate tracking systems. Companies frequently invest in blockchain and digital ledger technologies to prevent double-counting and ensure immutable records of ownership. Another major strategy involves expanding geographical reach through partnerships with national registries to facilitate seamless cross-border trading activities. Market participants also develop specialized products such as hourly matched certificates to meet the evolving demands of corporate purchaseers seeking granular verification. Additionally, organizations prioritize regulatory compliance by actively engaging with policybuildrs to shape future frameworks and standards. These approaches collectively support businesses maintain competitive advantages and adapt rapidly to shifting sustainability requirements within the region.

MARKET SEGMENTATION

This research report on the europe renewable energy certificate market is segmented and sub-segmented into the following categories.

By Type

- Renewable Energy Certificates (RECs)

- Green Attributes Certificates (GACs)

By Generation Source

- Hydropower

- Wind Power

- Solar Power

- Biomass

- Geothermal

By Market Design

- Regisattempt Systems

- Bilateral Contracts

- Exalter-Based Trading

By Counattempt

- Germany

- France

- United Kingdom

- Spain

- Sweden

- Norway

- Netherlands

- Rest of Europe