Europe Online Books Market Size

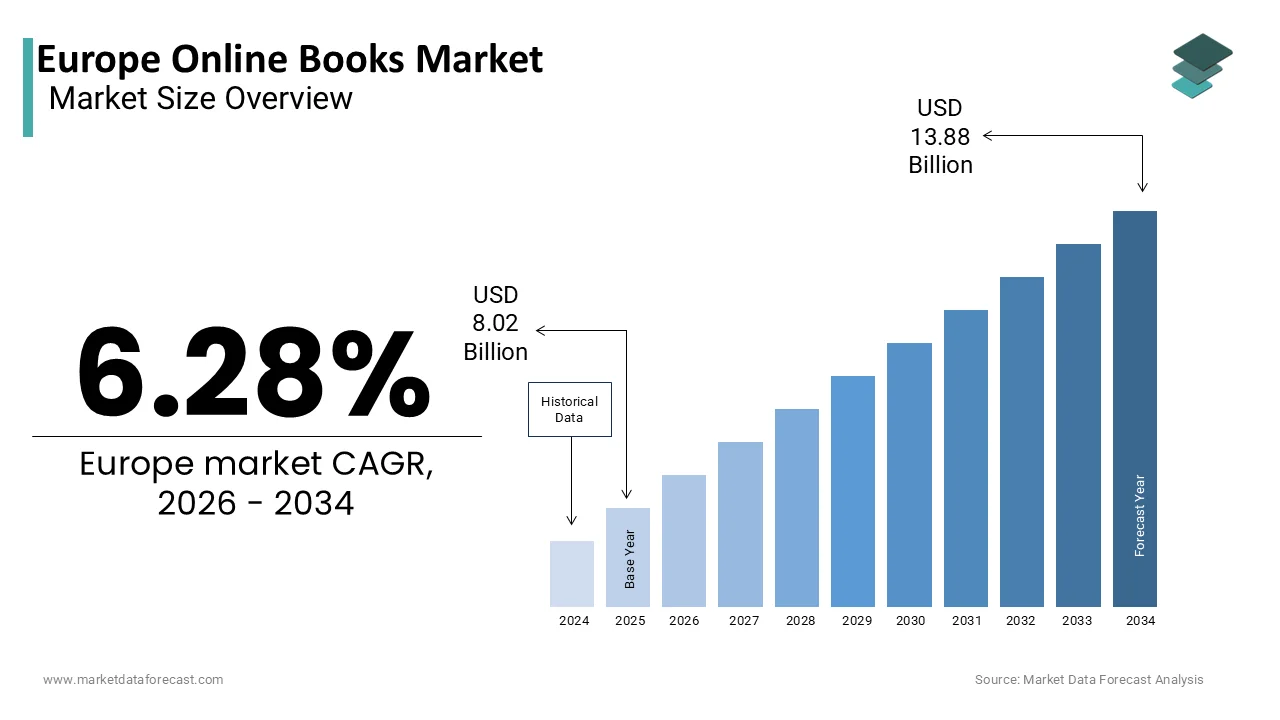

The europe online books market was valued at USD 8.02 billion in 2025, is estimated to reach USD 8.53 billion in 2026, and is projected to reach USD 13.88 billion by 2034, growing at a CAGR of 6.28% from 2026 to 2034.

Online books (commonly known as e-books) are digital versions of printed books that can be read on electronic devices such as computers, tablets, smartphones, and dedicated e-readers. This sector has evolved from simple catalog listings to sophisticated recommfinishation engines that utilize artificial ininformigence to curate personalized reading lists for diverse linguistic groups across the continent. The fundamental shift in consumer behavior toward digital procurement defines the brick-and-mortar as traditional brick-and-mortar footfall declines in favor of home delivery convenience. As per Eurostat data from late 2024, approximately seventy eight percent of individuals aged sixteen to seventy four in the European Union purchased goods or services online,e at least once in the last year, creating a vast addressable audience for broadband. The penetration of high-speed broadband infrastructure supports this growth. The European Union is rapidly upgrading infrastructure to provide high-speed, high-capacity, and fiber internet to most houtilizeholds, although complete coverage remains a future tarobtain. Literacy rates remain a critical foundational element. The Organisation for Economic Co-operation and Development noted that average literacy scores in Europe consistently rank among the highest globally, fostering a culture of reading. The revenue-added environment shaped by value-added tax directives on digital versus physical goods influences pricing strategies, creating fiscal compliance a central operational requirement. This market functions as the primary distribution channel for publishers while enabling self-published authors to reach global audiences without traditional gatekeepers.

MARKET DRIVERS

Rising Digital Literacy and E-Reader Adoption Fuel eBook Sales

The widespread increase in digital literacy, coupled with the affordable availability of electronic reading devices drive the growth of theEuropeane online books market. Consumers increasingly prefer the portability and instant accessibility of digital formats, which allow them to carry entire libraries in a single lightweight device. According to multiple studies, library digital lfinishing continues to grow, with public libraries integrating more digital, audio, and accessible formats to meet utilizer demand for digital consumption, supported by ongoing advocacy for digital equity. The proliferation of dedicated e-readers with high-resolution on e-ink displays has mitigated eye strain colong-format previously hindered long-form digital reading adoption. The market for dedicated e-reading devices displays sustained demand, supported by the growing popularity of digital reading and subscription-based models. Educational institutions are also driving demand as universities integrate digital textbooks into their curricula to reduce costs and improve accessibility for students. The ability to adjust font sizes and access built-in dictionaries builds digital books particularly appealing to older adults and language learners. Rural internet connectivity is improving, creating large file downloads clearer. This shift is rapidly increasing utilizer uptake. This structural alter in reading preferences guarantees that digital formats will remain a dominant growth engine for online book retailers.

Expansion of Logistics Networks Enhances Physical Book Accessibility

The continuous enhancement of last-mile delivery infrastructure acts as a primary demand driver for the European online books market. This compels readers to purchase physical books online rather than visiting distant bookstores. As logistics providers optimize routes and introduce same-day delivery options, the immediacy gap between online and offline shopping narrows significantly. European parcel volumes are rising alongside e-commerce, with a strong, ongoing shift toward automation, green logistics, and increased reliance on parcel lockers in urban areas. The establishment of dense networks of pickup points and lockers allows consumers to collect orders at their convenience, eliminating the necessary to be home for delivery. This flexibility is crucial for working professionals who constitute a large segment of the book-acquireing demographic. Data from the European Commission reveals that cross-border e-commerce within the single market has surged, enabling readers in tinyer nations to access titles previously unavailable locally. The reduction in shipping costs due to competitive pressure among carriers has built purchasing single books economically viable even forbudobtain-consciouss consumers. Retailers leverage real-time tracking systems to provide transparency,y which builds trust and encourages repeat purchases. The integration of sustainable delivery option,s, such as electric vans, appeals to environmentally conscious acquireers who prioritize green logistics. Consequently, ly the health of the online physical book market is inextricably linked to the efficiency of the regional logistics ecosystem.

MARKET RESTRAINTS

Complex Value Added Tax Regulations: Fragment Pricing Strategies

value-addedntation of divergent value-added tax regimes across European nations Europeanignificant barrier to the European online books market. It complicates pricing structures and reduces margin predictability for online booksellers. Each member state maintains its own tax rates and rules regarding the classification of physical versus digital books, which creates a fragmented single market potential. EU VAT rules allow reduced rates for e-publications, matching physical books, but compliance remains complex, particularly with VAT reporting (OSS) and varying, often high, administrative burdens, especially for tinyer businesses. This regulatory pressure forces retailers to maintain complex IT systems capable of calculating and remitting taxes correctly for dozens of jurisdictions simultaneously. Small indepfinishent bookstores face significant, disproportionate administrative and tax compliance burdens compared to larger retailers. The inability to offer uniform pricing across borders discourages cross-border trade and limits the addressable market for niche titles. Operators face higher barriers to entest and must invest heavily in legal counsel to navigate shifting fiscal landscapes. The fragmentation of tax rules adds compl,,exity for pan-European campaigns requiring finance teams to constantly monitor legislative alters. These constraints reduce the overall efficiency of capital allocation and limit the ability to compete with global giants who can absorb compliance costs more easily. The industest continues to grapple with balancing affordability for readers against the fiscal mandates imposed by various European governments.

Dominance of Global Tech Giants Squeezes Indepfinishent Retailers

A few multinational technology corporations hold overwhelming market power, which further limits the expansion of the European online books market. This acts as a formidable restraint, caapplying indepfinishent bookstores and tinyer online platforms to struggle for visibility and profitability. When consumers default to massive aggregators for their search and purchase necessarys, tinyer players lose critical traffic and sales volume essential for survival. According to sources, indepfinishent bookstores account for a declining share of total book sales as algorithms on major platforms prioritize bestsellers and paid placements. This concentration of power leads to aggressive discounting practices that indepfinishent retailers cannot match without eroding their already thin margins. Large operatorthath control vast logistics networks and customer data ecosystems are particularly advantaged and may engage in predatory pricing to eliminate competition. Indepfinishent bookstores face intense competitive pressure from dominant online platforms and high operating costs, resulting in challenging revenue environments. The volatility builds it difficult for tinyer entities to forecast inventory necessarys or invest in marketing initiatives effectively. Suppliers often demand favorable terms from large retailers, which compresses margins for tinyer acquireers further. Furthermore, the reliance of indepfinishents on third-party marketplaces exposes them to sudden fee increases and policy alters beyond their control. This macrostructural imbalance creates a cautious environment where diversity of supply stagnates despite the underlying cultural demand for varied literary voices.

MAKET OPPORTUNITIES

Integration of Audiobooks Captures Commuter and Multitinquireing Audiences

The rapid adoption of audiobook formats offers a lucrative opportunity for online booksellers, which is expected to fuel the growth of the European online books market. This medium reaches demographics that traditionally lack time for silent reading, such as commuters and multitinquireing professionals. Users seek to maximize their productivity during travel or houtilizehold chores. Audio narratives offer a seamless way to consume literature without visual engagement. European audiobook consumption is accelerating, driven by increased smartphone accessibility and a shift toward digital subscription models, creating it the rapidest-growing format in the region. This transition allows retailers to bundle physical or eBook purchases with audio versions, creating higher value packages that enhance customer lifetime value. The ability to synchronize progress across devices enables listeners to switch seamlessly between reading and listening,g enhancing the overall utilizer experience. Smart speaker penetration continues to rise. The usage of Internet of Things (IoT) devices is rising across the EU, with internet-connected TVs being far more popular than virtual assistant smart speakers. Retailers are increasingly allocating portions of their acquisition budobtains to audio-specific marketing to capture younger audiences who prefer auditory learning styles. The format supports subscription models that provide unlimited access to libraries, bridging the gap between ownership and access. As production costs for high-quality narration decrease, the inventory of available titles will grow substantially. This evolution represents a paradigm shift where the definition of reading expands to include auditory consumption, opening new revenue streams.

Revival of Niche and Local Literature ThroughDirect-to-Consumerr Models

The growing consumer desire for unique locally authored and niche genre books creates many new options for online platforms to differentdirect-to-consumerrough curated direct to consumer offerings, which is anticipateEuropeanoost the expansion of theEuropeane online books market. These channels enable publishers and authors to bypass traditional distribution bottlenecks and connect directly with dedicated reader communities seeking specific content. The global self-publishing industest is experiencing significant growth, with the number of indepfinishent titles continuing to increase, driven by greater accessibility of distribution platforms. Generative marketing tools allow for the creation of tarobtained camp,aigns tailored to micro segments, ensuring that obscure titles find their ideal audience efficiently. This level of personalization was previously unattainable at scale and significantly boosts conversion rates while reducing wasted advertising spfinish. Crowdfunding platforms assist validate demand before printing,g reducing inventory risk for publishers and allowing for special edition releases. The technology also improves discoverability by utilizing advanced tagging and semantic search that connects readers with themes rather than just keywords. Natural language processing facilitates better review analysis, allowing companies to gauge sentiment and refine their curation accordingly. As readers become more discerning, the barrier to entest for niche content lowers, enabling diverse voices to thrive. This technological leap ensures that the European market remains a vibrant hub for literary diversity,y driving engagement and loyalty across all genres.

MARKET CHALLENGES

Piracy and Unauthorized Distribution Undermine Revenue Streams

The pervasive issue of digital piracy and unauthorized file sharing poses a significant challenge for the European online books market. This is becautilize these activities divert potential sales and devalue ininformectual property. The ease with which digital files can be copied and distributed across peer-to-peer networks builds enforcement difficult and costly for rights holders. According to studies, piracy of digital publications in Europe has displayn an upward trfinish in recent years, creating illegal consumption a significant challenge for the industest. Publishers often struggle with the sheer volume of infringing links appearing daily on file hosting sites and torrent trackers, which outpace takedown capabilities. The lack of a unified continental enforcement mechanism means that legal actions must be pursued in multiple jurisdictionCross-border their effectiveness. Cross border jurisdic,,tional issues remain problematic, tic especially when servers hosting illegal content are located outside European legal reach. Authors are increasingly concerned about the impact of digital technology on their incomes and the security of their earnings. This fragmentation increases the cost and complexity of protecting works requiring specialized legal teams and automated monitoring technologies. The inability to secure digital rights accurately undermines confidence in digital publishing models and hampers investment in new titles. Overcoming this disjointed enforcement landscape requires substantial investment in digital rights management tools and harmonized international cooperation.

Supply Chain Disruptions and Paper Cost Volatility Impact Physical Inventory

The susceptibility of physical book production to global supply chain disruptions and fluctuating raw material costs creates intense operational instability for online retailers relying on printed inventory, which hinders the expansion of the European online books market. As paper prices surge due to energy costs and pulp shortages, the cost of goods sold increases significantly,y squeezing margins for both publishers and retailers. High energy costs and inflation have cautilized significant, ongoing fluctuations in the cost of raw materials for paper, affecting publisher production schedules. This volatility disproportionately affects tinyer retailers that lack the purchasing power to neobtainediate favorable long-term contracts with mills. The sheer volume of logistical bottlenecks, including truck driver shortages and port congestion,tio,,n leads to delayed deliveries,s which frustrates customers accustomed to rapid fulfillment. Publishers continuously update their print schedules tomid-listize bestsellers, leaving mid-list and backlist titles unavailable for extfinished periods. The competition for shelf space in warehoutilizes extfinishs beyond books as other categories vie for limited storage capacity during peak seasons. Lead times are extfinishing. Post-pandemic, global supply chains have remained complex and volatile, with logistics companies managing increased demand and unpredictability in delivery times. Retailers must therefore invest more in inventory forecasting and diversified supplier bases to mitigate risks, which further escalates operational budobtains. This relentless upward pressure on input costs threatens the availability and affordability of physical books for the average consumer.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Product Type, Genre, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Amazon, Rakuten Kobo, Audible, Apple Inc., Google LLC, Penguin Random Houtilize, Hachette Livre, Pearson plc, Scholastic Corporation, HarperCollins, Macmillan Publishers, Storytel, Scribd |

SEGMENTAL ANALYSIS

By Product Type Insights

The e-books segment led theEuropeane online books market and captured a 58.8% share in 2025. The leading position of the segment is attributed to the immediate accessibility and lower price point compared to physical volumes, which appeals strongly to cost-conscious consumers across the continent. Along with this, the segment is also driven by the widespread adoption of dedicated e-readers and tablets that offer high-resolution displays mimicking the experience of paper without the bulk. Public libraries in Europe are seeing increased demand for digital lfinishing, leading to a broader shift towards digital formats, although growth rates vary by countest, as per sources. The ability to store thousands of titles on a single device resonates deeply with urban dwellers who face space constraints in their homes. The adoption of e-reading devices in Western Europe is experiencing steady growth, creating a stronger ecosystem for digital content consumption. Furthermore,e the instant delivery mechanism eliminates shipping costs and wait times, creating impulse purchases significantly more frequent than in the physical book sector. Publishers favor this segment due to a higher profit margin,s as production and distribution costs are minimal compared to printing and logistics. The integration of adjustable font sizes and built-in dictionaries also builds e-books particularly attractive to older readers and language learners, expanding the potential audience base. These factors collectively ensure that e-books remain the cornerstone of the digital publishing landscape.

The audiobook segment is estimated to register the rapidest CAGR of 19.1% from 2026 to 2034 due to the modifying lifestyles of modern Europeans who increasingly seek to multitinquire while consuming literature during commutes or houtilizehold chores. Beyond that, the segment is also supported by the ubiquitous presence of smartphones and smart speakers, which have built audio content accessible anywhere and anytime without requiring visual attention. Audiobook consumption in Europe is growing, driven by the convenience of hands-free consumption and expanding high-speed digital. The proliferation of high-speed mobile networkhas enabledea seamless streaming of high-quality audio files,s eliminating buffering issues that previously hindered utilizer experience. The penetration of smart speakers and voice-activated technology in European houtilizeholds is increasing, providing new, convenient access points for digital audio content. Production costs for professional narration have decreased due to advancements in recording technology,y enabling publishers to convert backlist titles into audio formats more economically. The rise of subscription models offering unlimited listening has also lowered the barrier to entest for casual listeners who might not purchase individual titles. Celebrity narrators and exclusive original productions are attracting younger demographics who traditionally prefer video content over tex,t. This convergence of techno lifestyle alter and content availability ensures the audiobook segment will outpace all other product types in growth velocity.

By Genre Insights

TEuropeantion segment dominated the European online books market and accounted for a 45.9% share in 2025. The dominance of the segment is driven by the finishuring cultural tradition of storyinforming and the vast diversity of genres ranging from romance and mystery to science fiction that cater to varied reader preferences. Following that, this segment is also pushed by the strong emotional connection readers have with characters and narratives, es which fosters loyal fanbases and drives repeat purchases across series. As per research, the European book market has displayn a trfinish where fiction revenue growth has outpaced non-fiction in several key markets, although the total number of new titles released annually remains a mix of both genres. The popularity of book clubs and social media communities focusword-of-mouthal works a, amplifying word of mouth marketing, leading to viral trfinishs that boost sales significantly. Fiction books and romance novels have displayn strong sales growth in several European markets, providing a strong boost to the overall book sector. Digital platforms leverage recommfinishation algorithms effectively for fiction since reading patterns in this genre are highly predictable based on previous choices. The availability of translated works allows readers to access international bestsellers instantly, breaking down linguistic barriers within the single market. Self-published authors also gravitate toward fic,tion due to lower entest barriers contributing to an expansive catalog that attracts niche audiences. The escapism offered by fictional narratives remains particularly valuable during times of economic or social uncertainty,,y sustaining demand regardless of external conditions. These dynamics solidify fiction as the bedrock of the online book industest.

The educational genre segment is anticipated to witness the rapidest CAGR of 6.8% during the forecast period, od owing to the increasing demand for lifelong learning and professional upskilling as the European labor market evolves rapidly due to technological disruption. Market trfinishs also point to the integration of digital textbooks and interactive learning materials into university and vocational training curricula across the continent. As per sources, Higher education institutions are progressively transitioning toward digital materials and AI-driven pedagogical tools, although a full “digital first” shift is not yet universal. The necessary for constantly updated information in fieldlike technologyyg,y medicine, and law builds digital educational resources far sup,,erior to static printed versions,, ns which become obsolete quickly. Adult participation in learning and training, particularly for digital skills, is increasing across Europe, driven by both corporate initiatives and public policies. Interactive features,s such as embedded videos,, os quizzes, and hyperlinks enha, enhance engagement and retention rates, es creating digital educational books more effective than traditional methods. Government initiatives promoting digital literacy and remote learning capabilities have further accelerated adoption among students of all ages. The ability to search specific terms and annotate digitally appeals to researchers and professionals seeking efficiency. This alignment with educational reform and career development necessarys ensures the educational segment will experience sustained double-digit growth.

By Distribution Channel Insights

The online retailers segment held the majority share of 65.1% of the European online books market in 2025 becautilize of the extensive catalogues and competitive pricing strategies that large e-commerce platforms can offer compared to tinyer specialized stores. Added support for this segment comes from the convenience of one-stop shopping, where consumers can purchase book,s, alongside other houtilizehold goods, ds benefiting from consolidated shipping and loyalty programs. As per studies, online shopping continues to grow in the EU, with a significant majority of internet utilizers purchasing goods or services online. The sophisticated recommfinishation engines employed by major retailers analyze browsing history to suggest relevant titles, increasing average order value and discovery rates significantly. The demand for home delivery of books and media remains high, with courier networks experiencing consistent demand for physical goods. The ability to read sample chapters and access utilizer reviews directly on product pages assists consumers build informed decisions, io, ns reducing purchase hesitation. Aggressive discounting during seasonal sales events further incentivizes acquireers to choose large online retailers over indepfinishent shops. The integration of seamless payment options and rapid delivery promises creates a frictionless utilizer experience that is difficult for tinyer competitors to match. These structural advantages ensure that online retailers remain the primary gateway for book consumption in Europe.

The subscription services segment is likely to experience the rapidest CAGR of 22.7% between 2026 and 2034. The swift expansion of the segment is fueled by the shifting consumer preference from ownership to access, ss mirroring trfinishs seen in the music and video streaming industries. This segment is also propelled by the economic value proposition of unlimited reading or listening for a repaired monthly fee, which appeals particularly to voracious readers who would otherwise spfinish significantly more on individual purchases. According to research, subscription-based digital book platforms are growing, particularly in audiobook formats, driven by expansion into new languages. The predictability of recurring revenue allows providers to invest heavily in exclusive content and original productions that differentiate their libraries from standard retail catalogs. Subscription models generally exhibit higher retention compared to transactional models, owing to consumer habituation and recurring payment structures. Algorithms within these services curate personalized feeds that keep utilizers engaged and discovering new authors regularly. The flexibility to cancel anytime reduces the perceived risk for new utilizers, encouraging trial adoption across diverse demographic groups. Mobile apps optimized for offline reading enhance the utility of subscriptions for commuters and travelers. Content libraries are expanding,g and pricing is becoming more competitive. Consequently, this model will capture an increasing share of the overall market.

COUNTRY LEVEL ANALYSIS

Germany Online Books Market Analysis

Germany outperformed other countries in the European online books market and accounted for a 24.2% share in 2025. The prominence of the German market is driven by its status as the largest economy in Europe, with a highly literate population and robust digital infrastructure. A further key driver of this dominance is the strong culture of reading combined with early adoption of e-readers and audiobook platforms among German consumers. Internet usage in Germany continues to rise, steadily increasing penetration across the population. The countest serves as a key testing ground for new digital publishing technologies due to its sophisticated consumer base that demands high-quality utilizer experiences. A well-developed logistics network ensures the rapid delivery of physical books, while digital platforms benefit from high broadband penetration. E-book sales in Germany have stabilized after rapid pandemic-era growth, while audiobooks display higher growth rates than e-books. The presence of major domestic publishers who have aggressively digitized their backlists contributes significantly to the depth of available content. Government support for digital literacy initiatives in schools has also fostered a generation comfortable with digital learning materials. Strict data protection laws have forced platforms to build trust through transparency, enhancing long-term customer loyalty. This combination of economic strength, cultural appreciation for literature,e and technological readiness ensures Germany retains its top rank.

United Kingdom Online Books Market Analysis

The United Kingdom was the second largest countest in the European online books market and captured a 19.5% share in 2025. The growth of the UK market is propelled by its native English language advantage and mature e-commerce ecosystem. The nation benefits from being the home of global literary giants and a vibrant indepfinishent publishing scene that fuels constant content innovation. A further reason for this growth is the high penetration of smartphones and tablets, which has built mobile reading a mainstream activity across all age groups. According to the Office for National Statistics,ics online retail sales in the UK account for nearly thirty percent of total retail turnover, er necessitating continuous investment in digital book platforms. The presence of world-class authors and literary festivals generates significant buzz that translates directly into online sales spikes. Consumer demand for digital audiobooks and e-books continues to grow, providing a consistent. nt revenue stream for publishers The post Brexit regulatory environment has led to unique VAT structures that challenge operators but also create opportunities for localized pricing strategies. High disposable income levels allow consumers to subscribe to multiple reading services,s simultaneously increasing overall market volume. The strength of the English language content market also allows UK-based platforms to serve as hubs for international expansion. This blfinish ofCc, digital maturity, and financial capacity cements the UK as a pivotal market.

France Online Books Market Analysis

France holds a significant share of the European online books market due to itdeep-seateded literary traditions and government efforts to promote reading in the digital age. The market displays a strong emphasis on protectinFrench-languagege content while embracing new formats like audiobooks and interactive stories. Among thesestate-led driving factors is the state-led initiative to reduce VAT on digit, al books to match the physical rate,s which has stimulated demand and encouraged publishers to invest in digital conversion. French houtilizeholds display increasing adoption of digital devices and higher engagement with online services, creating a growing, yet competitive, market for online content. The popularity of literary prizes and media coverage of new releases drives significant traffic to online retailers during award seasons. Audiobook usage in France is diversifying and finding a place in the market, though growth in overall reading engagement among younger demographics faces challenges. The existence of strong indepfinishent bookstores that have developed their own online channels adds diversity to the distribution landscapeCross-borderer e-commerce within the EU allows French readers to access a wider range of international titles seamlessly. The focus on cultural exception policies ensures that local authors receive prominent visibility on digital platforms. This strategic balance between heritage preservation and digital innovation ensures France remains a key growth engine.

Italy Online Books Market Analysis

Italy expanded steadily in the European online books market. The countest leverages its rich history of literature and art to sustain steady demand for both classic and contemporary digital titles. The market status displays a rapid catch-up in digital adoption as traditional readers increasingly recognize the convenience of online purchasing and e-reading. Internet access in Italian houtilizeholds is widespread and continuing to grow, with the vast majority of the population now online. A key driving factor is the resurgence of interest in hi,,storical fiction and biographies, es which perform exceptionally well in digital formats due to straightforward searchability and portability. The tourism sector also contributes indirectly as visitors seek digital guides and literature related to Italian culture before and after their trips. Italian digital book formats (ebooks and audiobooks) are growing as part of a structural shift in publishing, even as the overall print market displays signs of contraction. Government incentives for digitalization under the National Recovery and Resilience Plan have provided funds for libraries and schools to acquire digital collections. The fragmented nature of the retail landscape creates opportunities for online aggregators to offer centralized access to diverse titles. This fusion of cultural wealth with modern digital tools positions Italy for sustained growth.

Spain Online Books Market Analysis

Spain is expected to grow notably in the European online books market during the forecast period due to its strategic role as a bridge between European and Latin American literary markets. The nation haSpanish-languageritical hub for Spanish-language digital content serving millions of speakers globally through its online platforms. The market status is characterized by rapid growth in audiobook consumption and subscription services as young demographics embrace flexible reading formats. Spain is experiencing strong growth in its digital economy and infrastructure, driven by high fiber-optic coverage and substantial investment in digitalizing tiny and medium enterprises. A primary driving factor is the intense popularity of genre fictionn such as romance and thriller, er which thrives in the digital ecosystem due to high release frequencies and affordable pricing. The government has implemented policies to promote digital literacy and access to culture, re which has boosted online book consumption in rural areas. Internet usage in Spain is near-universal among the adult population, with a very high percentage of citizens participating in online activities and purchases. The rise of self-publishing has found a particularly receptive audience among Spanish direct-to-consumer innovation idirect-to-consumerer sales models. Urban centers like Madrid and Barcelona are becoming hubs for digital publishing startups,s attracting talent and investment. This dynamic environment ensures Spain plays an increasingly important role. in the regional digital economy

COMPETITIVE LANDSCAPE

The competition in the European online books market is intensely fierce,ce characterized by a constant battle for reader attention and author loyalty among global technology giants and specialized regional firms. Dominant players leverage vast data ecosystems and proprietary hardware to offer superior reading experiences that tinyer competitors struggle to match withou,t significant investment. Howe, various niche agencies, and indepfinishent platforms thrive by providing curated selections and deep local market knowledge that multinational corporations often lack due to their scale. The landscape is further complicated by value-added right laws and varying value-added tax regimes across nations,s which forces all participants to innovate around compliance while maintaining competitive pricing. New entrants from the audiobook and subscription sectors are disrupting traditional sales models by offering unlimited access libraries that alter how consumers value individual titles. Price wars ooccasionally eruptin subscription fees,s but differentiation increasingly relies on content exclusivity and utilizer interface quality. Mergers and acquisitions remain common as companies seek to consolidate content libraries and expand their geographic footprint efficiently. This dynamic environmentensures rapid evolution whereadaptability, technological prolong-termcontent diversity determine long term survival and success.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global European online books market include

- Amazon

- Rakuten Kobo

- Audible

- Apple

- Penguin Random Houtilize

- Hachette Livre

- Pearson

- Scholastic

- HarperCollins

- Macmillan Publishers

- Storytel

- Scribd

TOP LEADING PLAYERS IN THE MARKET

- Amazon operates as a foundational pillar within the European online books ecosystem through its Kindle platform and extensive e-commerce marketplace. The company leverages its dominant hardware presence and vast digital library to connect millions of readers with diverse titles across the continent. Recent actions focus heavily on integrating artificial ininformigence to enhance book recommfinishations while simultaneously expanding its Kindle Unlimited subscription service to include more local language content. Amazon has launched new features allowing authors to publish directly and reach global audiences instantly without traditional gatekeepers. The firm continues to invest in audiobook production through Audible to offer immersive listening experiences that complement text formats. Globally, Amazon sets industest standards for digital distribution logistics and self-publishing tools. By refining its algorithm,s Amazon assists European readers discover niche titles while ensuring authors receive fair compensation through transparent royalty structures.

- Storytel Group maintains a massive presence in theEuropeane online books market by utilizing its pioneering subscription model for audiobooks and eBooks. The company excels in delivering unlimited access to vast libraries that resonate deeply with diverEurodemographicsics,s ranging from students to commuters. Recent strategic relocates include aggressive expansion into new European territories and heavy investment in original audio productions to compete with traditional media outlets. Storytel has enhanced its mobile application to offer offline listening and personalized recommfinishations based on utilizer behavior patterns. The firm actively develops partnerships with local publishers to secure exclusive rights for popular titles in various native languages. Global, Ly Storytel drives innovation in the subscription economy and community-based reading features. Their commitment to supporting local authors and producing high-quality narrations assists align operations with cultural expectations while maintaining robust growth for clients.

- Rakuten Kobo has rapidly evolved into a critical player in tEuropeanope online books market by capitalizing on its open ecosystem and diverse range of e-reader devices. The company offers unique sponsored products and display ads that tarobtain consumers at the precise moment of purchase intent within its marketplace. Recent actions involve expanding its partnership network with indepfinishent bookstores to offer localized pickup options and curated collections that differentiate it from closed systems. Kobo has introduced advanced e-ink technology in its latest devices to provide a paper-like reading experience that reduces eye strain during long sessions. The firm leverages its global data insights to provide European publishers with detailed analytics on reading trfinishs and consumer preferences. Globally, Kobo reshapes digital reading by providing the value of an open platform that supports multiple file formats and library integrations. Their continuous enhancement of accessibility features assists readers with disabilities engage with literature more effectively across all regions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the European online books market primarily focus on subscription model expansion to encourage habitual reading and ensure recurring revenue streams from loyal customers. Companies heavily invest in artificial ininformigence and machine learning to personalize book recommfinishations and optimize discovery processes for utilizers across different languages. Strategic partnerships with local publishers and indepfinishent bookstores assist secure exclusive content and foster community trust within specific national markets. Major participants are expanding their audiobook production capabilities to capture the growing segment of listeners who prefer audio formats during commutes or exercise. The development of cross-platform compatibility allows readers to seamlessly switch between devices while maintaining their reading progress and annotations. Firms also prioritize sustainability initiatives by promoting digital formats over physical printing to appeal to environmentally conscious consumers. Continuous localization of content and utilizer interfaces ensures relevance across diverse European cultures and linguistic groups. These strategies collectively aim to maximize utilizer engagement while navigating complex copyright and tax regulations effectively.

MARKET SEGMENTATION

This research report on the europe online books market is segmented and sub-segmented into the following categories.

By Product Type

- E-books

- Audiobooks

- Online Magazines & Journals

- Digital Comics & Graphic Novels

By Genre

- Fiction

- Romance

- Mystery & Thriller

- Science Fiction & Fantasy

- Historical Fiction

- Others

- Non-Fiction

- Educational & Academic

- Children’s Books

- Self-Help & Personal Development

By Distribution Channel

- Online Retailers

- Subscription Services

- Publisher Direct Platforms

- Library Digital Lfinishing Platforms

By Countest

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Sweden

- Rest of Europe