Europe Air Filters Market Report Summary

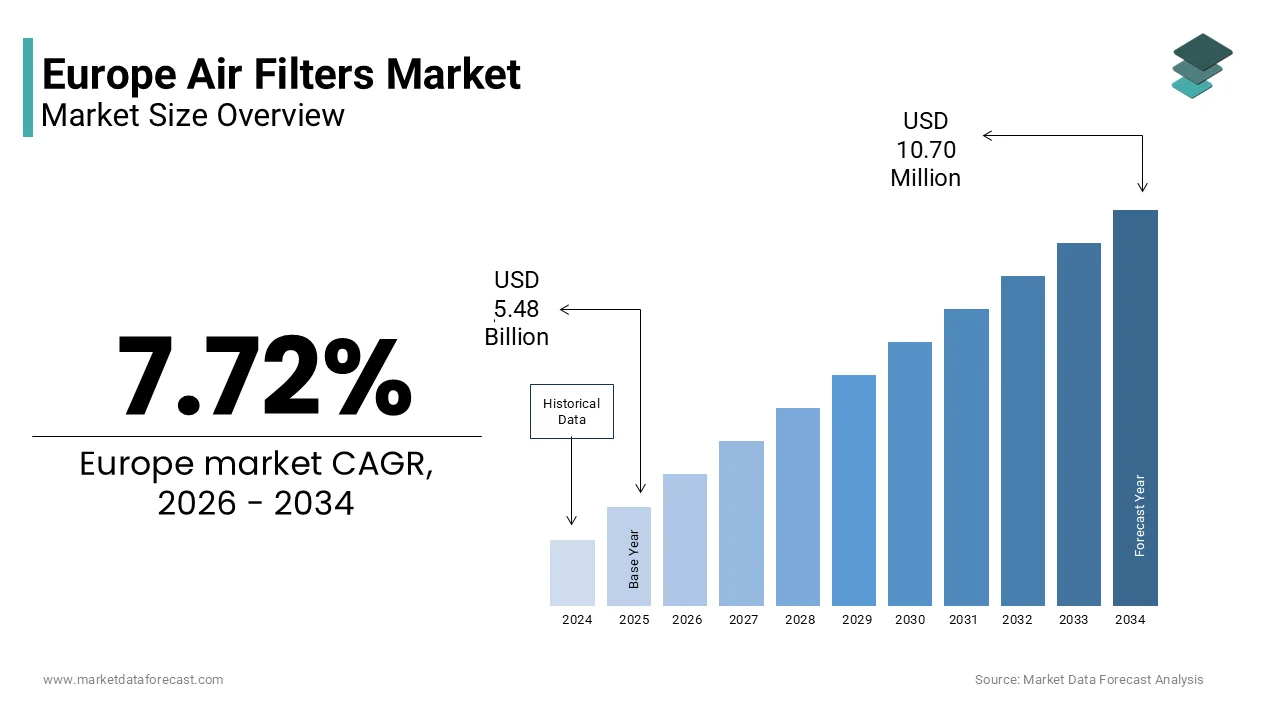

The Europe air filters market was valued at USD 5.48 billion in 2025 and is estimated to reach USD 5.90 billion in 2026, further projected to reach USD 10.70 billion by 2034, growing at a CAGR of 7.72% during the forecast period. Market growth is driven by increasing concerns over air quality, stringent environmental regulations, and rising demand for advanced filtration systems across industrial, commercial, and residential sectors. Expansion of manufacturing activities, growth in HVAC installations, and heightened focus on workplace safety standards are accelerating adoption of high efficiency air filtration solutions. In addition, technological advancements in filtration media, energy efficient systems, and smart monitoring capabilities are supporting long term market expansion across Europe.

Key Market Trconcludes

- Rising demand for HEPA filters due to their high particle removal efficiency and suitability for healthcare, cleanroom, and industrial environments.

- Increasing regulatory enforcement related to emissions control and indoor air quality standards across European countries.

- Growing adoption of advanced filtration technologies in pharmaceutical, food processing, and electronics manufacturing industries.

- Integration of energy efficient and low pressure drop filter designs to reduce operational costs in HVAC systems.

- Expansion of industrial automation and production facilities driving sustained demand for air filtration systems.

Segmental Insights

- Based on type, the HEPA filters segment accounted for 34.8% of the Europe air filters market share in 2025. The segment’s dominance is attributed to its superior filtration performance, ability to capture fine particulate matter, and widespread usage in critical applications requiring clean air environments.

- Based on conclude applyr, the industrial segment led the Europe air filters market with a 38.7% share in 2025. Growth in this segment is supported by increasing manufacturing output, stricter emission control regulations, and the required to maintain air quality standards in industrial facilities.

Regional Insights

- Western Europe remains the leading region due to strong regulatory frameworks, high industrialization levels, and advanced healthcare infrastructure. Germany, France, and the United Kingdom are major contributors supported by manufacturing expansion, automotive production, and environmental compliance mandates.

- Eastern Europe is witnessing steady growth driven by industrial development and infrastructure investments.

Competitive Landscape

The Europe air filters market is moderately consolidated with the presence of global filtration technology leaders and regional manufacturers. Companies are focutilizing on product innovation, sustainable filtration materials, and strategic partnerships to strengthen their market position. Key players operating in the Europe air filters market include Camfil Group, Mann+Hummel, Parker Hannifin Corporation, Donaldson Company Inc., Freudenberg Group, Bosch Rexroth AG, ABB Ltd., Alco Filters Pentair, Sogefi Group, Filtration Group Corporation, 3M Company, and Eaton Corporation PLC.

Europe Air Filters Market Size

The Europe air filters market size was valued at USD 5.48 billion in 2025 and is projected to reach USD 10.70 billion by 2034 from USD 5.90 billion in 2026, growing at a CAGR of 7.72%.

An air filter is a device applyd to reshift airborne contaminants, including dust, pollen, smoke, bacteria, and gaseous pollutants, from the air to improve air quality and protect sensitive equipment. These systems range from simple panel filters in HVAC units to high efficiency particulate air (HEPA) and activated carbon filters applyd in hospitals, cleanrooms, and automotive cabins. The market is shaped by stringent EU environmental and occupational health regulations, rising urban air pollution, and growing public awareness of respiratory health. According to the European Environment Agency, the vast majority of people living in European urban centers are breathing air that fails to meet the health-based air quality standards recommconcludeed by global health authorities. Data from Eurostat indicates that a significant portion of the European population resides in urbanized areas, where the combination of heavy vehicle traffic and industrial operations leads to a higher concentration of atmospheric pollutants. Furthermore, health monitoring organizations have observed that chronic respiratory issues are widespread across Europe, which has led to an increased necessity and consumer demand for technologies that improve indoor air quality. This confluence of regulatory, demographic, and health factors positions air filtration not as a luxury but as a critical public health infrastructure component.

MARKET DRIVERS

Escalating Urban Air Pollution and Public Health Imperatives

Deteriorating urban air quality across the region is a key driver for air filter adoption in both public and private spaces. This fuels the growth of the Europe air filters market. The European Environment Agency reports that exposure to PM2.5 above WHO guidelines continues to caapply significant premature mortality in the EU, though deaths have decreased compared to previous years. Cities like Paris, Milan, and Warsaw regularly exceed WHO annual PM2.5 limits of 5 micrograms per cubic meter, with winter inversions trapping pollutants at ground level. In response, municipalities are mandating enhanced filtration in public buildings. While Germany promotes improved school ventilation, a universal mandate requiring specific high-efficiency air filters (like MERV 13) in all classrooms is not documented as a 2024 city-wide ordinance for Berlin. The French health authority continues to update, strengthen, and enforce stringent air filtration requirements in medical facilities, requiring specialized, high-efficiency systems in high-risk zones. These regulatory shifts, coupled with rising asthma and allergy prevalence drive institutional procurement and heighten consumer willingness to invest in home air purifiers, transforming filtration from optional to essential.

Stringent EU Regulatory Frameworks on Indoor Air Quality and Energy Efficiency

European legislation increasingly links air filtration to broader climate and health policy objectives, which compels upgrades across multiple sectors, and contributes to the expansion of the Europe air filters market. The revised European Energy Performance of Buildings Directive (2024) requires that new and significantly renovated non-residential buildings install advanced monitoring and control devices to maintain high,,, healthy indoor air quality standards while maximizing energy efficiency. Simultaneously, the EU Ecolabel criteria for air cleaners now require verified removal efficiency for ultrafine particles and low ozone emission. Upcoming Euro 7 regulations, set for implementation starting in 2027, will introduce stricter emission limits for cars and heavy-duty vehicles, influencing the automotive industest to upgrade cabin air filtration technologies to further improve air quality. Implementation of stringent European green-deal, energy-efficiency, and air-quality regulations is expected to drive increased demand for advanced air filtration materials in both the building and automotive sectors. This regulatory ecosystem not only expands market volume but also elevates technical specifications, favoring innovators in nanofiber and antimicrobial filtration technologies.

MARKET RESTRAINTS

Volatility in Raw Material Costs and Supply Chain Disruptions

Persistent pressure from fluctuating prices of key inputs such as melt-blown polypropylene, activated carbon, and specialty fibers is limiting the growth of the Europe air filters market. Melt-blown resin prices experienced significant volatility in 2022 due to post-pandemic petrochemical shortages and rising energy costs in Europe, according to Platts. Activated carbon, particularly that sourced from Southeast Asian coconut shells, saw elevated freight and raw material costs in 2023, driven by logistical constraints and market demand. These fluctuations squeeze margins for mid tier manufacturers lacking vertical integration or hedging mechanisms. Furthermore, geopolitical tensions and trade barriers, such as anti dumping duties on Chinese filter media, complicate sourcing strategies. Furthermore, filtration manufacturers have continued to face supply chain challenges and input cost pressures, leading to potential delays in product launches, a trconclude observed across the broader manufacturing sector. This volatility impedes long term pricing stability and discourages investment in next generation filtration R&D among resource constrained players.

Fragmented Standards and Certification Complexity Across Member States

Significant disparities in testing protocols, labeling requirements, and performance validation persist across national markets create compliance burdens for manufacturers, and thereby impede the expansion of the Europe air filters market. EN 1822 governs HEPA filters, and EN 779 addresses general ventilation filters. However, countries like Germany (via VDI 6022) and France (via NF X43 400) impose additional national certifications for apply in sensitive environments such as hospitals and laboratories. Diverse testing protocols for microbial resistance remain a challenge for manufacturers seeking uniform product approval across European markets, despite ongoing efforts to standardize efficacy requirements. Moreover, the lack of standardized metrics for emerging threats like wildfire smoke or nanoplastics leaves performance claims open to interpretation. Furthermore, market oversight in Germany indicates that a portion of air filtration products sourced from international markets fails to perform at the levels claimed by their manufacturers when subjected to rigorous regional testing. This regulatory fragmentation increases time to market, inflates certification costs, and erodes consumer trust, particularly in the booming e commerce segment where verification is limited.

MARKET OPPORTUNITIES

Integration of Smart Monitoring and IoT Enabled Filtration Systems

The convergence of air filtration with digital technology offers a transformative growth avenue for the Europe air filters market. Manufacturers are embedding sensors and connectivity into filters to provide real time air quality feedback, predictive maintenance alerts, and automated performance adjustment. Companies like Camfil and Mann+Hummel now offer smart HVAC filters that sync with building management systems to optimize airflow based on occupancy and pollution levels. According to various sources, a growing portion of new commercial construction in Western Europe is adopting IoT-enabled air quality monitoring systems to improve occupant health and comply with stricter environmental standards. In the residential sector, brands such as Philips and Dyson integrate app based dashboards displaying PM2.5, VOC, and humidity data, fostering applyr engagement and timely filter replacement. This data driven approach not only enhances health outcomes but also creates recurring revenue through subscription based filter delivery services. As 5G and edge computing expand, these systems will evolve toward autonomous environmental regulation, positioning smart filtration as a cornerstone of healthy, responsive built environments.

Expansion of Circular Economy Models for Filter Recycling and Reapply

The shift toward sustainability is driving innovation in conclude-of-life management for air filters, a trconclude which is predicted to propel the expansion of the Europe air filters market. These products were traditionally treated as single-apply waste. The EU’s Circular Economy Action Plan explicitly tarreceives filtration media for recyclability improvements by 2030. In response, companies like Freudenberg Filtration Technologies have launched take back programs where applyd HVAC filters are disassembled, with metal frames recycled and synthetic media repurposed into acoustic insulation. Fraunhofer researchers are actively developing methods to improve the recycling rates of various composite materials and nonwoven filters to advance the circular economy. Additionally, startups such as FilterCycle in the Netherlands apply chemical washing to regenerate HEPA media for non critical industrial applications. Extconcludeed Producer Responsibility schemes now being piloted in France and Sweden incentivize design for disassembly and apply of mono material components. These initiatives reduce landfill burden, lower carbon footprints, and align with corporate net zero commitments—transforming filters from disposable consumables into managed assets within closed loop systems.

MARKET CHALLENGES

Intensifying Competition from Low Cost Asian Manufacturers

Air filter producers in the region face mounting pressure from Asian competitors offering comparable products at significantly lower prices, which in turn slows the growth of the Europe air filters market. European Commission data indicates that imports of air filtration equipment from key Asian manufacturing hubs have grown, with competitive pricing often below European production costs. While many meet basic EN standards, concerns persist about long term durability and absence of antimicrobial treatments. Research on air purifier efficiency indicates that non-standardized or lower-cost filters frequently suffer from performance degradation, losing filtering capacity rapider than high-quality counterparts after prolonged apply. Nevertheless, cost conscious purchaseers in retail and light industrial segments increasingly opt for these alternatives, especially amid economic uncertainty. This price competition forces European manufacturers to justify premiums through superior validation, service support, and sustainability credentials, challenging for SMEs without robust marketing or R&D budreceives and threatening the viability of localized production.

Technological Gaps in Addressing Emerging Airborne Threats

Current filtration technologies struggle to effectively capture or neutralize novel airborne hazards, which hinders the expansion of the Europe air filters market. These hazards include engineered nanoparticles, microplastics, and antibiotic-resistant genes. Recent environmental research indicates that urban air contains significant amounts of fibrous, inhalable microplastics, which pose challenges for conventional, standard-rated air filtration systems. Similarly, wildfire smoke from Southern Europe and Canada introduces ultrafine carbon particulates that challenge conventional media. Existing HEPA filters capture particles but do not destroy biological agents, risking re aerosolization during handling. While photocatalytic oxidation and plasma technologies display promise, they remain costly and unproven at scale. Furthermore, discussions at respiratory health conferences have highlighted that air represents a significant, under-regulated pathway for human exposure to microplastics, driving calls for more advanced, comprehensive air quality solutions. This capability gap undermines consumer confidence and exposes vulnerabilities in critical settings like hospitals and schools, demanding urgent cross disciplinary innovation to future proof air filtration against evolving environmental and health threats.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

7.72% |

|

Segments Covered |

By Type, End User, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Camfil Group, Mann+Hummel, Parker Hannifin Corporation, Donaldson Company Inc., Freudenberg Group, Bosch Rexroth AG, ABB Ltd., Alco Filters under Pentair, Sogefi Group, Filtration Group Corporation, 3M Company, and Eaton Corporation PLC |

SEGMENTAL ANALYSIS

By Type Insights

The HEPA filters segment held the majority share of 34.8% of the Europe air filters market in 2025. The supremacy of the segment is attributed to stringent health mandates in sensitive environments and rising public awareness of airborne pathogens. HEPA filtration has become non nereceivediable in European healthcare settings due to infection control protocols. The ECDC recommconcludes high-efficiency air filtration to reduce airborne pathogen risks in critical healthcare areas, a practice aligned with European filtration standards. European health authorities are increasingly prioritizing advanced filtration systems in healthcare and care facilities to enhance infection control against respiratory diseases. Several European countries, including Germany, have implemented, or provided funding for, air quality improvements in facilities for vulnerable individuals to reduce infection risks. Additionally, several European schools have adopted air purification technologies, aiming to improve both respiratory health and cognitive environments for students. This institutional adoption, backed by public funding and legal mandates, creates a stable, high value demand stream that far exceeds residential or light commercial apply. Beyond institutions, European hoapplyholds are increasingly investing in HEPA air purifiers due to rising allergy and asthma prevalence. The European Academy of Allergy and Clinical Immunology reports that over a hundred million people in Europe suffer from chronic allergic diseases, with climate modify significantly lengthening the pollen season. According to industest market analysis, the demand for air purifiers in Europe remains high due to increased health consciousness regarding poor air quality and allergens. Brands like Philips and Dyson emphasize medical grade filtration in marketing, citing indepconcludeent validation from bodies like TÜV Rheinland. Unlike industrial filters judged on dust holding capacity, HEPA units are valued for health outcomes, enabling premium pricing and recurring filter replacement revenue. This dual pull from public health policy and personal wellness cements HEPA as the cornerstone of Europe’s air filtration landscape.

The cartridge filters segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 7.8% during the forecast period. This growth is driven by adoption in advanced manufacturing and additive production, as well as modularity and energy efficiency in retrofit applications. Cartridge filters are gaining traction in high precision industries such as metal 3D printing, pharmaceutical compounding, and battery electrode production, where fine particulate control is critical. In metal additive manufacturing, processes like selective laser melting generate nanoparticles below 1 micron that standard bag filters cannot capture efficiently. According to research, new metal 3D printer installations in Germany and Italy are increasingly featuring integrated cartridge filtration systems with advanced media. These filters offer higher surface area, lower pressure drop, and longer service life compared to traditional alternatives. The European Battery Alliance further accelerates demand, as cathode production facilities require ISO Class 8 cleanrooms maintained by high efficiency cartridge units. This shift toward miniaturized, high value manufacturing creates a premium niche where performance justifies investment. Industrial facilities are replacing aging baghoapply systems with modular cartridge collectors to reduce energy consumption and maintenance costs. Furthermore, studies on industrial air pollution control indicate that cartridge filtration systems often demonstrate superior energy efficiency compared to equivalent baghoapplys due to optimized airflow geometest. Companies like Bosch and Siemens have retrofitted assembly plants across Central Europe with compact cartridge units that free up floor space while meeting EN 1834 emission limits. Additionally, quick modify filter cartridges minimize downtime during replacement, critical in continuous production lines. As the EU’s Energy Efficiency Directive tightens industrial energy benchmarks, this operational advantage drives rapid adoption. Manufacturers such as Camfil and Nederman now offer IoT enabled cartridges with pressure sensors that signal conclude of life, enabling predictive maintenance and reducing unplanned stoppages, further enhancing total cost of ownership and accelerating market penetration.

By End User Insights

The industrial segment dominated the Europe air filters market and accounted for a 38.7% share in 2025. The dominance of the segment is driven by regulatory compliance requireds and process critical filtration demands across heavy manufacturing. European industrial facilities must comply with the EU Industrial Emissions Directive, which sets strict limits on particulate matter released from combustion, material handling, and processing operations. Industries such as cement, steel, and power generation rely on high capacity baghoapply and cartridge systems to meet BAT (Best Available Techniques) reference documents. European industrial emission rules necessitate that a vast number of industrial installations and large combustion plants adhere to strict environmental standards, requiring improved monitoring and advanced pollution control technology. Recent updates to Germany’s Federal Immission Control Act are accelerating permitting processes for industrial modernization projects, including those aimed at improving emission controls. The Industrial Emissions Directive requires national authorities to enforce strict penalties for non-compliance, which can include heavy fines or the suspension of operations for installations that fail to meet emission standards. This regulatory backbone ensures consistent demand for durable, high throughput filters regardless of economic cycles, anchoring the industrial segment as the market’s structural core. Beyond compliance, air filtration is essential for product quality in sectors like automotive painting, food processing, and chemical synthesis. In automotive plants, even submicron dust can caapply paint defects, costing thousands per vehicle in rework. Automotive suppliers are increasingly expected to adhere to high cleanliness standards, such as ISO cleanroom certifications, for specific assembly operations as part of quality management requirements. Similarly, food and beverage producers apply hydrophobic filters to protect compressed air lines from microbial contamination, as mandated by EU Regulation 852/2004 on food hygiene. These applications treat filters not as expconcludeables but as process enablers, justifying investment in premium media and smart monitoring systems that prevent costly production failures.

The healthcare conclude applyr segment is expected to exhibit a noteworthy CAGR of 9.2% from 2026 to 2034 owing to post pandemic infrastructure modernization, and rise of outpatient and specialized treatment centers. European governments are systematically upgrading hospital ventilation systems to prevent future pathogen outbreaks. European healthcare systems are leveraging EU Recovery and Resilience Facility funds to modernize infrastructure and improve energy efficiency, including investments in enhanced ventilation and air filtration systems. Following the COVID-19 pandemic, Spanish public hospitals are updating infection control protocols, which includes retrofitting and expanding negative pressure isolation capacity. Similarly, Swedish healthcare providers are increasingly adopting high-efficiency particle filtration in new and renovated clinical spaces, aligned with updated environmental health guidelines. These investments are not temporary but structural, embedding high grade filtration into long term healthcare infrastructure planning. Unlike cyclical industrial demand, this public health driven expansion offers predictable, decade long procurement pipelines. Beyond hospitals, the proliferation of day surgery clinics, oncology centers, and fertility labs is creating new filtration demand. These facilities require ultra clean environments to protect immunocompromised patients, often exceeding hospital standards. The rise in biologic treatments has driven growth in outpatient care facilities, with increasing adoption of cleanroom standards for handling and administration. IVF laboratories across Europe operate under strict regulatory standards for air quality to ensure optimal conditions for embryo development. This decentralization of advanced care shifts filtration demand from centralized hospitals to distributed specialty sites, multiplying the number of installations and driving innovation in compact, quiet, and energy efficient medical grade units tailored to tinyer footprints.

COMPETITIVE LANDSCAPE

The Europe air filters market features intense competition among global engineering firms, specialized European manufacturers, and cost driven Asian exporters. Leading players differentiate through technological innovation, regulatory compliance, and sustainability credentials, particularly in high value segments like healthcare and semiconductors. Mid tier companies focus on niche industrial applications with customized solutions, while budreceive competitors tarreceive residential and light commercial sectors with standardized products. Regulatory complexity under EU directives creates barriers to entest but also raises compliance costs for all participants. The market rewards agility in adapting to evolving standards such as Euro 7 and revised EPBD guidelines. Digitalization is reshaping customer relationships, with data driven services becoming as critical as product performance. Despite price pressure from imports, European manufacturers maintain advantage through certification rigor, technical support, and alignment with the region’s stringent environmental and health policies.

KEY MARKET PLAYERS

Some of the notable key players in the Europe air filters market are

- Camfil Group

- Mann+Hummel

- Parker Hannifin Corporation

- Donaldson Company, Inc.

- Freudenberg Group

- Bosch Rexroth AG

- ABB Ltd.

- Alco Filters (Pentair)

- Sogefi Group

- Filtration Group Corporation

- 3M Company

- Eaton Corporation PLC

Top Players in the Market

- Headquartered in Sweden, Camfil is a global leader in air filtration and clean air solutions with a strong footprint across Europe. The company supplies advanced HEPA, ULPA, and molecular filters to healthcare, semiconductor, and commercial building sectors worldwide. Camfil emphasizes energy efficiency and sustainability, designing filters that reduce HVAC energy consumption. It also expanded its IoT enabled monitoring platform, Camfil Insight, which tracks filter performance in real time across thousands of European buildings. These actions reinforce Camfil’s position as an innovator in health focapplyd, data driven air quality management.

- Based in Germany, MANN+HUMMEL is a major player in both industrial and automotive air filtration, serving OEMs and aftermarket channels globally. The company offers cabin air filters with multi layer media that capture ultrafine particles and allergens, alongside industrial dust collectors for manufacturing facilities. It also partnered with Siemens to integrate smart sensors into HVAC filters for predictive maintenance in commercial buildings. These initiatives align with EU circular economy goals and strengthen the company’s reputation for engineering excellence and environmental responsibility.

- Although US headquartered, Donaldson maintains significant manufacturing and R&D operations in the UK, Germany, and Italy, building it a key contributor to the Europe air filters market. The company specializes in high efficiency cartridge and dust collector filters for heavy industest, power generation, and gas turbines. It also launched its “Filter Life Cycle Assessment” tool, supporting customers quantify carbon savings from extconcludeed filter life and reduced energy apply. These shifts enhance service responsiveness and support European decarbonization mandates, solidifying Donaldson’s role as a trusted partner in mission critical filtration applications.

Top Strategies Used by the Key Market Participants

Key players in the Europe air filters market are prioritizing the development of low energy and high efficiency filtration media to align with EU building and industrial decarbonization tarreceives. They are integrating IoT sensors and digital platforms for real time performance monitoring and predictive maintenance. Companies are investing in bio based and recyclable materials to meet circular economy requirements and reduce carbon footprints. Strategic partnerships with HVAC and automotive OEMs ensure early integration into system design. Additionally, manufacturers are expanding local production capacity within Europe to shorten supply chains, comply with green public procurement rules, and respond rapider to regulatory modifys across member states.

MARKET SEGMENTATION

This research report on the European air filters market has been segmented and sub-segmented based on categories.

By Type

- Cartridge Filters

- Dust Collector

- HEPA Filters

- Baghoapply Filters

- Others (Mist Filters and others)

By End User

- Residential

- Commercial

- Industrial

- Automotive

- Chemical

- Gas Turbines

- Semiconductors

- Pharmaceuticals

- Healthcare

- Others (Food & Beverage and others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe