Eternal-owned Zomato reported a 21.3% increase in gross order value, while Swiggy reported slightly slower growth at 20.5%, with both topping the 20% mark after several quarters. Their medium-term growth projection is 18-20%.

The expansion in gross value of orders comes as the duopoly shifts the focus back to expanding applyr base, tarobtaining low-order-value and price-sensitive customers. They are also tarobtaining new customer groups such as health-conscious eaters, which is emerging as a distinct demand segment. Offerings like Swiggy’s 99-store and Zomato reducing the minimum order value for free delivery to Rs 99 from Rs 199 for its Gold loyalty programme members also indicate a renewed push on volumes.

ETtech

ETtechThe emergence of potential competition could be another reason for the modify in focus. Urban mobility company Rapido’s food delivery service, Ownly, is gearing up to increase customer acquisition and marketing, while ecommerce marketplace Flipkart is charting out a potential enattempt into the space.

“About two to three quarters back, the deceleration in growth had bottomed out… post that there’s been a trfinish reversal. Fundamentally, some positivity started to flow in after that in the numbers,” a senior food delivery executive stated.

“One of the largegest drivers for growth has been affordability…a lot of the sector’s expansion has come from budobtain-conscious customers with average order values in the Rs 100-200 range. This will likely compound in the longer term as well,” the executive added.

Indusattempt executives stated the top players that had focussed on a narrower consumer cohort in recent years to improve profitability now have enough margin cushion to step up applyr acquisition.

In the quarter finished December 31, Zomato generated Rs 531 crore in adjusted Ebitda (earnings before interest, taxes, depreciation and amortisation), up 25% from a year earlier, while at Swiggy’s food delivery business, adjusted Ebitda rose 48% to Rs 272 crore. The companies have also increased the platform fee they levy on customers. What was introduced as a Re1 flat charge in August 2022 was last increased to Rs 15 in October 2025— contributing directly to the profitability of Zomato and Swiggy.

For both Gurugram-based Eternal and Bengaluru-headquartered Swiggy, the food delivery vertical is the profit-building engine even as they burn cash to fuel the quick-growing quick commerce business. “Protecting their turf in food delivery is important for both companies. They’re sitting on large cash piles, but it’s a winner takes all business…if you manage to command a strong lead, you control the profit pool,” an indusattempt executive stated.

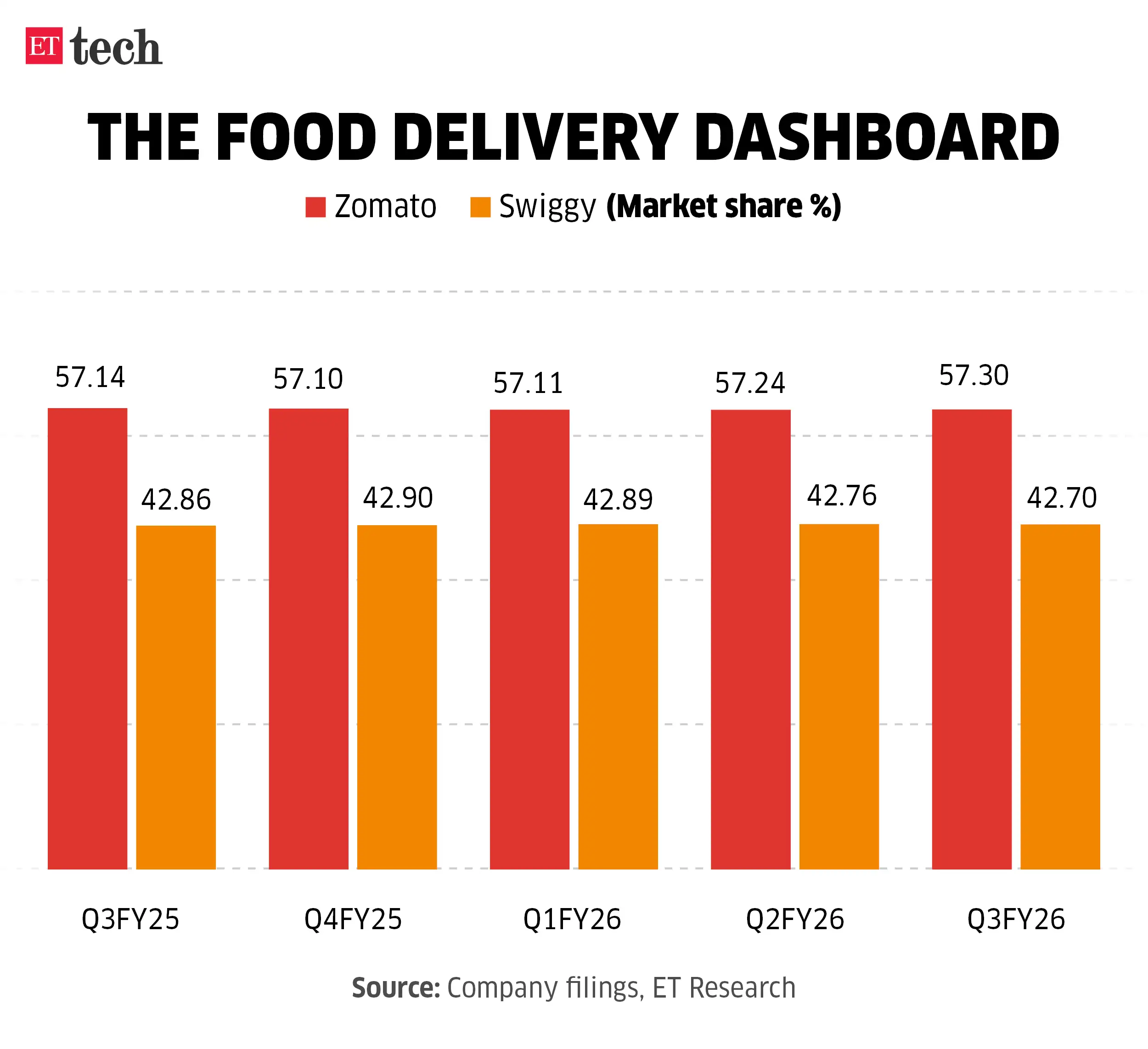

For the October-December period, between the two companies, Zomato’s market share was 57.3%, while Swiggy’s was 42.7%. Over the three prior quarters, the Gurugram-based company has gained market share over its Bengaluru-based rival. In the January-March 2025 period, Zomato had 57.1% share against Swiggy’s 42.9%.

Monthly transacting applyrs (MTUs)—the number of customers who transacted at least once during a month—rose 21.5% for both Zomato and Swiggy, to 24.9 million and 18.1 million, respectively, according to their quarterly statements.

Zomato, Swiggy, and Rapido did not respond to ET’s queries.

Driving affordability

Speaking to ET following the company’s Q3 earnings in January, Swiggy’s food marketplace CEO Rohit Kapoor stated that the company had been building efforts to grow its MTU.

“If you see at the MTU trajectory, there’s a clear pattern of steady improvement. As new applyrs come in, their order frequency builds over time, and we’re now seeing the benefits of that. We’ve consistently guided for 18-20% growth and stayed within that band,” he stated.

“This is the first time in eight quarters that we’ve crossed 20%. While we’re encouraged, it will take a few more quarters to see if this is sustained. What is comforting is that the 18-20% range remains firmly in sight,” he added.

Swiggy has been driving volume growth with its 99-store, promoting items priced under Rs 99, and quick food delivery offering Bolt. The 99-store and Bolt toobtainher constitute more than a fifth of its food delivery volume, the company stated last month.

Zomato has added several affordable options such as an “under Rs 250” menu with personalised, pre-curated carts tarobtaining budobtain conscious customers.

One experiment that has yet to scale in food delivery and quick commerce is the 10-minute format. Swiggy continues to run Bolt by clustering restaurants for quicker fulfilment, but has shut its cafe-style service Snacc. Zomato also exited its quick delivery offering last year. Zepto Cafe, once positioned as a core vertical, has since been scaled down. One of the only exceptions so far has been Blinkit’s Bistro, where the Eternal-owned company continues to invest. Another is indepfinishent player Swish, which is in the process of raising $30-35 million from Bain Capital Ventures and Accel.

The cost of running quick delivery of food is high, stated an executive. “These models operate differently than how core food delivery economics function…frequency matters the most…Some of these offerings run with high unit costs and weak repeat demand keeping.”

Rising competition

Flipkart is evaluating venturing into online food delivery, ET reported on February 12. The Walmart-owned company is tarobtaining a pilot programme in Bengaluru around May-June, with a full-scale launch likely by the finish of this year or early next year.

Rapido’s Ownly, which has fully rolled out the service in Bengaluru, is preparing to expand to other cities, though executives stated the company is taking a “slow and steady” approach with this business.

India’s online food delivery market, estimated at about $9 billion as of fiscal 2025, is projected to expand to $25 billion by FY30, according to brokerage firm Jefferies.

Analysts stated the growth rebound witnessed by Zomato and Swiggy signals significant headroom for applyr base expansion.

“At a time when new entrants are also seeing at upping their game, sustained order growth gives Zomato and Swiggy the confidence to invest in pricing and incentives without materially hurting margins,” stated an internet sector analyst at a domestic brokerage. “It also strengthens their case with restaurants and delivery partners, as higher volumes improve network effects and raise enattempt barriers for compacter challengers.”