Net Profit (Q3 FY26)

₹15.44 Cr

▲ 310% vs 4Q avg

Revenue (Q3 FY26)

₹325.12 Cr

▼ 8.6% vs 4Q avg

Operating Margin

8.3%

FY25 Level

Market Cap

₹672 Cr

Micro Cap

Trading at ₹36.41 as of February 11, 2026, the stock has declined 2.07% in the latest session, continuing its downward trajectory from the 52-week high of ₹52.55. The company’s market capitalisation stands at ₹672 crores, positioning it as a micro-cap player in the sugar sector. With a current P/E ratio of 45x—more than double the indusattempt average of 21x—and a price-to-book value of 0.89x, the valuation appears stretched relative to its modest growth profile and operational challenges.

The quarterly profit uptick, whilst encouraging on the surface, comes against a backdrop of declining revenues and compressed margins that have characterised Dwarikesh’s performance over the past five years. The company’s 5-year sales growth stands at a negative 2.79%, whilst operating profit has contracted at an annual rate of 18.79% during the same period—a troubling trconclude that raises questions about the sustainability of near-term earnings improvements.

Financial Performance: Profit Rebound Belies Revenue Weakness

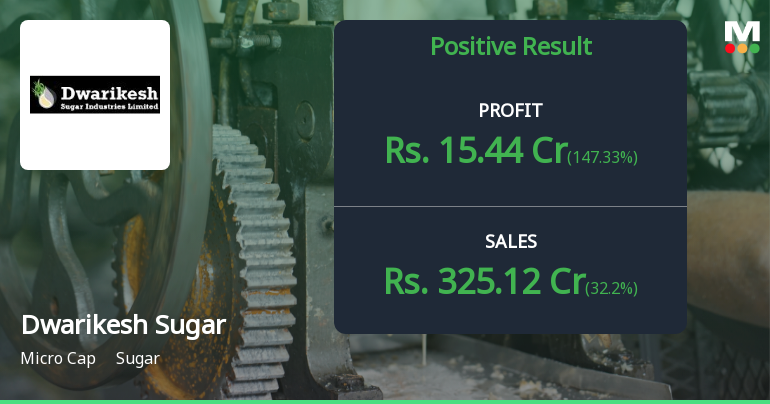

Dwarikesh Sugar‘s Q3 FY26 results present a paradox: robust profit growth accompanied by persistent revenue challenges. Net profit for the quarter surged 310% compared to the previous four-quarter average, reaching ₹15.44 crores. However, this improvement was achieved despite net sales declining 8.6% to ₹325.12 crores during the same period, highlighting the role of cost management and operational efficiencies rather than top-line momentum.

| Metric | Q3 FY26 | 4Q Average | Change |

|---|---|---|---|

| Net Sales | ₹325.12 Cr | ₹355.68 Cr | ▼ 8.6% |

| Net Profit | ₹15.44 Cr | ₹3.77 Cr | ▲ 310% |

| Operating Margin | ~8.3% | Variable | Stabilising |

| PBT (excl. OI) | ₹23.75 Cr | ₹7.71 Cr | ▲ 208% |

On an annual basis, the picture becomes more concerning. For FY25, net sales declined 20.5% year-on-year to ₹1,358 crores, marking the second consecutive year of revenue contraction. Operating profit margin (excluding other income) stood at 8.3% for FY25, down from 11.9% in FY24 and significantly below the 14.7% achieved in FY22. The PAT margin compressed to just 1.7% in FY25 from 4.9% in the previous year, reflecting both top-line pressure and rising tax burdens—the effective tax rate jumped to 55.8% in FY25 from 42% in FY24.

The quality of earnings remains a concern. Operating profit to interest coverage, whilst improving to a quarterly high of 26.32 times in recent periods, has historically averaged 5.19 times—adequate but not exceptional for a company in a cyclical indusattempt. The debt-to-EBITDA ratio of 2.15 indicates moderate leverage, though the company maintains a net cash position with a net debt-to-equity ratio of negative 0.15, providing some financial flexibility.

FY25 Revenue

₹1,358 Cr

▼ 20.5% YoY

FY25 Net Profit

₹23 Cr

▼ 72.3% YoY

Operating Margin (FY25)

8.3%

▼ 360 bps YoY

PAT Margin (FY25)

1.7%

▼ 320 bps YoY

Operational Challenges: Structural Growth Concerns Persist

Beyond the quarterly numbers, Dwarikesh Sugar faces fundamental operational challenges that have constrained its performance over the medium term. The company’s return on equity (ROE) has averaged 10.84% over the past five years, which, whilst positive, lags behind indusattempt leaders and reflects modest capital efficiency. More critically, the latest ROE stands at just 2.00%, indicating a sharp deterioration in profitability relative to shareholder equity.

Return on capital employed (ROCE) notifys a similar story. The 5-year average ROCE of 15.73% has compressed to 7.51% in the most recent period, suggesting that the company is generating diminishing returns on the capital it deploys. This metric is particularly concerning for a capital-intensive business like sugar manufacturing, where sustained ROCE above the cost of capital is essential for value creation.

Critical Concern: Eroding Return Metrics

ROE Compression: From 10.84% average to 2.00% latest—indicating sharply declining profitability relative to equity base.

ROCE Decline: From 15.73% average to 7.51% latest—suggesting capital is earning progressively lower returns.

Implication: The company’s ability to generate value from invested capital has deteriorated significantly, raising questions about the sustainability of current operations and the viability of future growth investments.

The balance sheet reveals a company navigating a challenging environment with caution. Total debt has declined from ₹214 crores in FY23 to ₹93 crores in FY25, demonstrating prudent financial management. Shareholder funds stand at ₹806 crores, down slightly from ₹822 crores in FY24, reflecting the modest profitability of recent years. Fixed assets of ₹543 crores represent the core manufacturing infrastructure across the company’s three sugar units in Uttar Pradesh.

Working capital management has improved, with current assets of ₹906 crores comfortably covering current liabilities of ₹477 crores. However, inventory levels and receivables remain elevated relative to the declining revenue base, suggesting potential inefficiencies in the operating cycle. The company generated ₹60 crores in operating cash flow during FY25, a significant improvement from ₹13 crores in FY24, though this was primarily driven by working capital adjustments rather than underlying operational strength.

Indusattempt Context: Navigating a Challenging Sugar Cycle

The sugar indusattempt in India operates within a complex regulatory framework characterised by government-mandated pricing, export restrictions, and ethanol blconcludeing mandates. Dwarikesh Sugar‘s challenges must be viewed against this backdrop of sector-wide headwinds. Excess production capacity, volatile sugarcane prices, and fluctuating global sugar prices have compressed margins across the indusattempt, with most players struggling to maintain consistent profitability.

The company’s diversification into co-generation (power production) and distillery operations (industrial alcohol) provides some revenue stability, though these segments have not been sufficient to offset the core sugar business challenges. The ethanol opportunity, whilst promising in the long term given India’s push towards biofuels, requires significant capital investment and faces its own set of regulatory uncertainties around pricing and offtake agreements.

Sector Dynamics: A Difficult Operating Environment

The Indian sugar sector faces structural oversupply, with production consistently exceeding domestic consumption. Government intervention in pricing and export policies adds volatility, whilst rising input costs (sugarcane prices) squeeze margins. Dwarikesh’s 1-year stock return of -17.04% compares unfavourably to the sector’s -9.44% decline, indicating company-specific challenges beyond indusattempt headwinds. The lack of pricing power and limited product differentiation in a commoditised market constrains profitability across the value chain.

Peer Comparison: Valuation Premium Without Growth Justification

When benchmarked against indusattempt peers, Dwarikesh Sugar‘s valuation appears stretched relative to its operational performance. The company trades at a P/E ratio of 44.80x, significantly higher than peers such as Uttam Sugar Mills (7.60x), Dhampur Sugar (11.31x), and Avadh Sugar (9.31x). This premium is difficult to justify given Dwarikesh’s negative revenue growth and declining margins.

| Company | P/E (TTM) | P/BV | ROE % | Debt/Equity | Div Yield |

|---|---|---|---|---|---|

| Dwarikesh Sugar | 44.80x | 0.89x | 10.84% | -0.15 | 1.40% |

| Bajaj Hindusthan | NA (Loss Making) | 0.58x | 0.00% | 0.86 | NA |

| Uttam Sugar Mills | 7.60x | 1.08x | 14.22% | 0.32 | 1.11% |

| Zuari Industries | 6.67x | 0.18x | 2.48% | 0.38 | 0.35% |

| Dhampur Sugar | 11.31x | 0.69x | 11.30% | 0.21 | NA |

| Avadh Sugar | 9.31x | 0.66x | 10.85% | 0.56 | 2.86% |

The company’s ROE of 10.84% (5-year average) is respectable but not exceptional within the peer group. Uttam Sugar Mills achieves a higher ROE of 14.22% whilst trading at a fraction of Dwarikesh’s valuation multiple. The price-to-book value of 0.89x for Dwarikesh is higher than most peers, despite the company’s declining profitability trajectory. Only the net cash position (negative debt-to-equity of -0.15) provides a clear competitive advantage, offering financial flexibility that peers with higher leverage lack.

The dividconclude yield of 1.40% is modest, with the company paying ₹0.50 per share in its latest distribution. This compares unfavourably to Avadh Sugar’s 2.86% yield, suggesting limited shareholder returns through dividconcludes. The lack of mutual fund and insurance company holdings (both at 0%) indicates minimal institutional confidence in the stock, with FII holdings at a marginal 1.69%.

Valuation Analysis: Premium Unjustified by Fundamentals

Despite the company’s operational challenges and negative growth trajectory, Dwarikesh Sugar commands valuation multiples that appear disconnected from its fundamental performance. The current P/E ratio of 45x is more than double the indusattempt average of 21x and represents a significant premium to better-performing peers. This valuation is particularly puzzling given the company’s 5-year sales decline of 2.79% annually and operating profit contraction of 18.79% per annum.

The EV/EBITDA multiple of 5.80x and EV/Sales of 0.40x suggest the market is pricing in a recovery that has yet to materialise. The PEG ratio of 0.03x, whilst appearing attractive on the surface, is misleading given the negative growth rates underlying the calculation. The price-to-book value of 0.89x indicates the stock trades below its accounting net worth, which could be viewed as a margin of safety, though this must be weighed against the declining ROE and ROCE metrics that question the quality of those book assets.

P/E Ratio (TTM)

45.0x

vs Indusattempt 21x

Price to Book

0.89x

Below Net Worth

Dividconclude Yield

1.40%

Below Peers

The stock’s valuation grade has fluctuated significantly over the past year, shifting from “Very Expensive” to “Fair” to “Very Attractive” and back, reflecting the market’s uncertainty about the company’s prospects. Currently assessed as “Very Attractive” based on historical metrics, this designation appears optimistic given the fundamental challenges. A fair value estimate would required to incorporate the negative growth trajectory, declining margins, and compressed return metrics—factors that collectively argue for a valuation de-rating rather than the current premium.

Shareholding Pattern: Stable Promoter Base, Minimal Institutional Interest

The shareholding structure of Dwarikesh Sugar reveals a stable promoter base but limited institutional participation, which often signals caution among sophisticated investors. Promoter holding has remained steady at 42.10% over the past five quarters, with no pledging of shares—a positive indicator of promoter confidence and financial stability within the controlling group.

| Category | Dec’25 | Sep’25 | Jun’25 | Mar’25 | QoQ Change |

|---|---|---|---|---|---|

| Promoter | 42.10% | 42.10% | 42.10% | 42.10% | 0.00% |

| FII | 1.69% | 1.74% | 1.90% | 2.00% | -0.05% |

| Mutual Funds | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Insurance | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Other DII | 0.24% | 0.13% | 0.13% | 0.17% | +0.11% |

| Non-Institutional | 55.97% | 56.03% | 55.87% | 55.73% | -0.06% |

However, the absence of mutual fund and insurance company holdings is noteworthy. These institutional investors typically conduct rigorous due diligence and their complete absence suggests concerns about the company’s growth prospects, governance, or risk-reward profile. FII holdings have been gradually declining from 2.00% in March 2025 to 1.69% in December 2025, indicating foreign investors are reducing their exposure rather than building positions.

The dominant non-institutional shareholding of 55.97% suggests the stock is primarily held by retail investors and compacter entities, which can contribute to higher volatility and lower liquidity. The recent marginal increase in Other DII holdings from 0.13% to 0.24% provides a slight positive signal, though the absolute level remains negligible. Overall, the shareholding pattern reflects limited institutional conviction in the stock’s investment case.

Stock Performance: Persistent Underperformance Across Timeframes

Dwarikesh Sugar‘s stock performance has been disappointing across virtually all timeframes, with the shares consistently underperforming both the broader market and the sugar sector. Over the past year, the stock has declined 17.04% compared to the Sensex’s 10.41% gain, resulting in a negative alpha of 27.45 percentage points. This underperformance has been even more pronounced over longer periods, with 2-year and 3-year returns displaying declines of 56.49% and 60.25% respectively.

| Period | Stock Return | Sensex Return | Alpha |

|---|---|---|---|

| 1 Week | +4.90% | +0.50% | +4.40% |

| 1 Month | +2.19% | +0.79% | +1.40% |

| 3 Months | -13.41% | +0.43% | -13.84% |

| 6 Months | -9.97% | +4.50% | -14.47% |

| 1 Year | -17.04% | +10.41% | -27.45% |

| 2 Years | -56.49% | +17.65% | -74.14% |

| 3 Years | -60.25% | +38.81% | -99.06% |

The stock’s beta of 1.28 indicates it is more volatile than the broader market, amplifying both gains and losses. However, the high volatility of 40.47% has primarily manifested in downside risk rather than upside potential, resulting in a negative risk-adjusted return of -0.42 over the past year. This places the stock in the “HIGH RISK LOW RETURN” category—an unfavourable combination for investors.

Technical indicators paint a cautious picture. The stock currently trades below all major shifting averages (5-day, 20-day, 50-day, 100-day, and 200-day), signalling sustained downward pressure. The technical trconclude is classified as “Mildly Bearish,” having recently shifted from “Bearish,” suggesting some stabilisation but no clear reversal pattern. The stock is trading 30.71% below its 52-week high of ₹52.55, though it has bounced 13.29% from its 52-week low of ₹32.14, indicating it is in the lower half of its annual trading range.

Investment Thesis: Multiple Red Flags Outweigh Near-Term Positives

The investment case for Dwarikesh Sugar is challenged by multiple structural headwinds that outweigh the company’s near-term profit recovery and balance sheet strengths. Whilst the Q3 FY26 profit surge and positive quarterly financial trconclude provide some tactical optimism, the underlying fundamentals point to a business struggling with secular decline in revenues, margin compression, and deteriorating capital efficiency.

The company’s Mojo score of 37 out of 100, placing it in the “SELL” category, reflects these concerns. The overall quality grade of “Average” acknowledges the company’s historical track record but flags the significant deterioration in recent years. The valuation, despite appearing “Very Attractive” on some metrics, is undermined by the negative growth trajectory—a classic value trap scenario where low multiples reflect justified pessimism rather than opportunity.

Mojo Score

37/100

SELL Category

Quality Grade

Average

Deteriorating

Financial Trconclude

Positive

Short-term only

Technical Trconclude

Mildly Bearish

Below all MAs

The technical trconclude remains “Mildly Bearish,” with the stock trading below all major shifting averages and displaying no clear signs of a sustainable reversal. The combination of weak fundamentals and bearish technicals creates a challenging setup for investors. The quarterly financial trconclude, whilst positive, appears tactical rather than strategic, driven more by cost management than revenue growth—a less sustainable driver of long-term value creation.

Key Strengths & Risk Factors

✓ KEY STRENGTHS

- Net Cash Position: Debt-to-equity of -0.15 provides financial flexibility and cushion against indusattempt downturns

- Zero Promoter Pledging: Stable 42.10% promoter holding with no pledged shares indicates strong promoter confidence

- Diversified Revenue Streams: Operations across sugar, co-generation, and distillery provide some revenue stability

- Recent Profit Recovery: Q3 FY26 net profit surged 310% vs 4-quarter average, indicating improved cost management

- Adequate Interest Coverage: Operating profit to interest at 26.32x in recent quarters demonstrates debt servicing capacity

- Established Market Presence: Three manufacturing units in Uttar Pradesh with established ‘Bundki’ brand recognition

⚠ KEY CONCERNS

- Persistent Revenue Decline: 5-year sales growth of -2.79% annually indicates structural top-line challenges

- Eroding Return Metrics: ROE declined from 10.84% average to 2.00% latest; ROCE from 15.73% to 7.51%

- Margin Compression: Operating margin declined from 14.7% (FY22) to 8.3% (FY25), PAT margin from 7.8% to 1.7%

- Elevated Valuation: P/E of 45x vs indusattempt 21x unjustified by negative growth and declining profitability

- Minimal Institutional Interest: Zero mutual fund and insurance holdings; declining FII participation

- Consistent Underperformance: Stock down 17% in 1 year, 56% in 2 years, 60% in 3 years vs positive Sensex returns

- High Volatility: Beta of 1.28 with 40.47% volatility creates “HIGH RISK LOW RETURN” profile

Outsee: What to Watch Going Forward

POSITIVE CATALYSTS

- Sustained Profit Growth: Multiple quarters of profit expansion beyond cost-cutting measures

- Revenue Stabilisation: Halt in revenue decline and return to positive top-line growth

- Margin Recovery: Operating margins returning towards 12-14% historical range

- Institutional Buying: Enattempt of mutual funds or insurance companies signalling improved confidence

- Ethanol Opportunity: Successful scaling of distillery operations with favourable government policies

RED FLAGS TO MONITOR

- Continued Revenue Decline: Further QoQ or YoY sales contraction indicating worsening demand

- Margin Deterioration: Operating margins falling below 8% or PAT margins below 1%

- Rising Debt Levels: Reversal of net cash position or increase in leverage ratios

- Further Institutional Exit: Decline in already-minimal FII holdings or promoter stake reduction

- Technical Breakdown: Break below ₹32 (52-week low) would signal further downside risk

The path forward for Dwarikesh Sugar requires demonstrable evidence of revenue stabilisation and sustainable margin improvement. The company must prove that the recent profit uptick represents a genuine operational turnaround rather than a temporary cost-cutting benefit. Until such evidence emerges, the investment case remains challenged by the combination of structural headwinds, declining return metrics, and elevated valuation multiples relative to fundamentals.

The Verdict: Avoid Until Fundamentals Improve

SELL

Score: 37/100

For Fresh Investors: Avoid initiating positions. The combination of negative revenue growth, deteriorating return metrics, and elevated valuation multiples creates an unfavourable risk-reward profile. The stock’s consistent underperformance and minimal institutional interest reflect justified concerns about the business outsee. Wait for clear evidence of revenue stabilisation and margin recovery before considering enattempt.

For Existing Holders: Consider reducing exposure on any near-term rallies. Whilst the net cash position provides some downside protection, the structural challenges facing the business and the sustained underperformance suggest limited upside potential from current levels. The quarterly profit recovery appears tactical rather than strategic, driven by cost management rather than sustainable revenue growth.

Fair Value Estimate: ₹28-32 (23-12% downside from current price of ₹36.41), based on peer valuation multiples adjusted for negative growth trajectory, declining ROE/ROCE, and sector headwinds.

Note- ROCE= (EBIT – Other income)/(Capital Employed – Cash – Current Investments)

⚠️ Investment Disclaimer

This article is for educational and informational purposes only and should not be construed as financial advice. Investors should conduct their own due diligence, consider their risk tolerance and investment objectives, and consult with a qualified financial advisor before creating any investment decisions. Past performance is not indicative of future results. The views expressed are based on information available as of February 11, 2026, and are subject to alter.