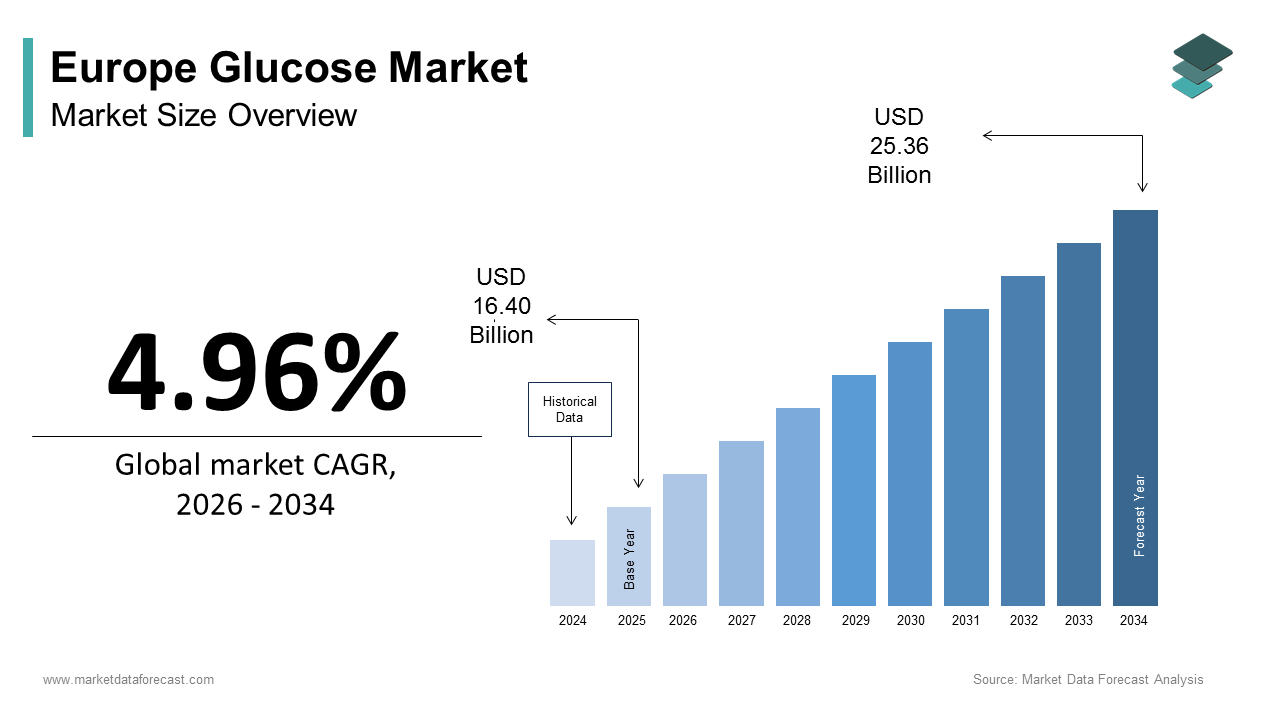

Europe Glucose Market Size

The Europe glucose market size was calculated to be USD 16.40 billion in 2025 and is anticipated to be worth USD 25.36 billion by 2034, from USD 17.22 billion in 2026, growing at a CAGR of 4.96% during the forecast period.

Glucose refers primarily to dextrose monohydrate and anhydrous glucose derived from the enzymatic hydrolysis of starch and is applyd across food, beverage, pharmaceutical, and industrial applications as a sweetener, bulking agent, fermentation substrate, and energy source. Unlike sucrose or high fructose syrups, glucose is valued for its clean sweetness, rapid metabolism, and functional properties such as crystallization control and fermentation efficiency. Europe’s glucose production is deeply integrated into the region’s agricultural economy, with over 60 starch processing facilities operating under the European Starch Association’s sustainability framework. According to Eurostat, more than 11 million metric tons of starch were processed from EU‑grown cereals and tubers in 2024, providing the primary feedstock for glucose syrup and crystalline dextrose. The European Food Safety Authority recognizes glucose as a safe ingredient with no quantitative usage limits in most food categories, while also approving its apply in oral rehydration solutions and parenteral nutrition. With the EU’s Farm to Fork Strategy promoting crop diversification and bio‑based value chains, glucose serves as a key biochemical node linking arable farming to downstream food, health, and biotech sectors.

MARKET DRIVERS

Expanding Demand for Glucose in Fermentation-Based Bio-Based Chemical Production

The industrial biotechnology sector’s rapid growth in Europe is a major driver for glucose consumption, which is one of the major factors propelling the European glucose market growth. As per the European Bioplastics Association, polylactic acid production in the EU has been increasing steadily in recent years. Companies like Corbion and BASF operate large-scale fermentation plants in the Netherlands and Germany that consume significant volumes of glucose annually to produce lactic acid, succinic acid, and biobased amino acids. According to the European Commission’s Circular Bio-based Europe Joint Undertaking, substantial funding has been allocated to support industrial biotechnology projects requiring high-purity glucose as feedstock. Additionally, the EU’s REACH regulation incentivizes the substitution of petrochemicals with bio-based alternatives, which is accelerating adoption in sectors like cosmetics, where glucose-derived squalane is replacing fossil-sourced emollients. With the EU tarreceiveing 25% of organic chemical production from renewable carbon by 2030, glucose’s role as a foundational bio building block ensures sustained and diversifying industrial demand beyond traditional food applications.

Rising Use in Sports and Clinical Nutrition Formulations

Glucose’s rapid glycemic response and metabolic efficiency have cemented its role in specialized nutritional products, which is driving consistent demand across health and wellness segments and further boosting the glucose market expansion in Europe. In sports nutrition, glucose is the preferred carbohydrate in isotonic drinks and energy gels, due to its rapid absorption and ability to replenish muscle glycogen without gastrointestinal distress. According to the European Specialist Sports Nutrition Alliance, glucose or dextrose is widely listed as the primary carbohydrate source in EU-approved isotonic beverages. The clinical nutrition sector relies on glucose for enteral and parenteral feeding solutions, especially in critical care settings. As per the European Society for Clinical Nutrition and Metabolism, millions of hospitalized patients across the EU receive glucose-based intravenous formulations for caloric support during recovery. Furthermore, the EU’s aging population, as per Eurostat, is contributing to rising demand for oral nutritional supplements, where glucose provides quick energy for frail or malnourished individuals. Regulatory clarity under the EU Medical Devices Regulation also facilitates approval of glucose-containing clinical products, reinforcing its status as an essential therapeutic ingredient.

MARKET RESTRAINTS

Consumer Perception and Policy Pressure Linking Glucose to Sugar Reduction Agfinishas

Despite its biochemical distinction from sucrose and high fructose corn syrup, glucose is often conflated with “added sugars” in public health discourse, which is leading to regulatory and consumer headwinds and hampering the regional market growth. The European Commission’s revision of nutrient profiling models for front-of-pack labeling includes glucose in the total sugar calculation, which is triggering mandatory warning labels on products exceeding thresholds. As per the European Consumer Organisation, a majority of EU consumers now actively avoid products labeled as high in sugar, even when glucose is applyd for functional purposes such as texture or fermentation. National policies compound this pressure. The UK’s Soft Drinks Indusattempt Levy, although technically exempting glucose-based beverages due to low fructose content, has created market confusion, which is leading manufacturers to reformulate across the board. In France, the Public Health Law mandates a reduction in added sugars in processed foods by 2027, which is prompting food companies to replace glucose with non-nutritive sweeteners, despite functional trade-offs. This regulatory amhugeuity and consumer misperception constrain innovation and volume growth in traditional food applications, even where glucose offers technical or metabolic advantages over alternatives.

Feedstock Price Volatility Driven by Agricultural and Energy Market Interdepfinishencies

The Europe glucose market faces significant cost instability due to its reliance on starch derived from corn, wheat, and potatoes, which are subject to climate variability, trade policy, and competition from biofuel demand. As per the European Commission’s Agricultural Market Observatory, wheat prices in the EU have revealn considerable fluctuations in recent years, due to droughts and export restrictions. Since starch accounts for a large share of glucose production costs, these swings directly impact manufacturer margins. Additionally, the EU’s Renewable Energy Directive classifies wheat and corn-based ethanol as transitional biofuels, creating demand competition. According to Eurostat, large volumes of EU wheat are diverted to bioethanol production, reducing starch availability. Energy costs further amplify pressure. As per Eurostat, EU industrial electricity prices have risen significantly compared to earlier years. This triple exposure to agricultural commodity, energy, and policy volatility builds long-term pricing and investment planning exceptionally challenging for European glucose producers.

MARKET OPPORTUNITIES

Integration into Precision Fermentation for Alternative Protein Production

Europe’s burgeoning alternative protein sector presents a high growth opportunity for glucose, as the essential energy source in precision fermentation processes that produce dairy proteins, egg whites, and heme without animals. Companies like Formo in Germany and those in France apply genetically engineered microbes fed with high-purity glucose to synthesize casein and albumin at a commercial scale. As per the Good Food Institute Europe, multiple precision fermentation startups have raised significant venture funding in recent years. The European Food Safety Authority approved the first glucose-derived animal-free whey protein for human consumption, setting a regulatory precedent. According to indusattempt reports, each kilogram of fermented protein requires substantial amounts of glucose, creating this a material-intensive and rapidly scaling application. With the EU’s Farm to Fork Strategy tarreceiveing a 25% reduction in livestock emissions by 2030, alternative proteins are receiving policy tailwinds, including research grants under Horizon Europe. Glucose producers that guarantee non-GMO, traceable, and sustainably sourced feedstock can position themselves as strategic partners in Europe’s protein transition, which is creating a premium, high-volume outlet insulated from traditional food market pressures.

Expansion in Pharmaceutical Excipient and Biopharmaceutical Applications

The European pharmaceutical indusattempt’s reliance on glucose as a multifunctional excipient and cell culture nutrient offers a resilient and high-value growth corridor for the European glucose market. In solid dosage forms, glucose acts as a binder, diluent, and stabilizer in tablets, particularly for pediatric and geriatric formulations where sucrose is contraindicated. More significantly, glucose is a critical component in cell culture media for monoclonal antibody and vaccine production, with bioreactors requiring precise concentrations to maintain cell viability. As per the European Medicines Agency, the majority of biologics manufactured in the EU apply glucose-based media in upstream processing. BioPhorum reported that European bioreactor capacity has expanded rapidly, driven by mRNA vaccine infrastructure and biosimilar demand. Companies like Roquette and Tereos now offer pharma-grade anhydrous dextrose, compliant with European Pharmacopoeia standards. With the EU investing billions of euros in health security and biomanufacturing resilience under the Critical Medicines Act, glucose’s role as an irreplaceable pharmaceutical raw material ensures stable demand, with stringent quality premiums that offset food sector volatility.

MARKET CHALLENGES

Stringent Regulatory Requirements for Food and Pharma Grade Purity

Compliance with divergent and evolving purity standards across food, pharmaceutical, and industrial applications imposes significant operational and financial burdens on European glucose producers, which is a major challenge to the growth of the European glucose market. Food-grade glucose must meet specifications under Regulation (EC) No 1333/2008, including limits on heavy metals, sulfated ash, and residual proteins, while pharmaceutical grade must adhere to the European Pharmacopoeia monograph 0750, requiring finishotoxin testing, microbial limits, and strict particle size control. As per the European Directorate for the Quality of Medicines, numerous glucose batches have been rejected due to trace impurities from shared production lines. Maintaining separate, dedicated lines for each grade increases capital expfinishiture considerably, according to the European Starch Association. Furthermore, the EU’s update to allergen labeling rules requires starch processors to validate the absence of gluten in wheat-derived glucose, even when below detection thresholds, creating additional analytical costs. These regulatory silos prevent economies of scale and complicate supply chain transparency, especially as customers demand documentation for sustainability and non-GMO status. Until harmonized quality frameworks emerge, producers must bear the cost of parallel compliance systems, limiting agility and innovation.

Limited Differentiation in a Commoditized Product Landscape

The Europe glucose market suffers from low product differentiation, as most offerings are chemically identical crystalline dextrose or standard DE 42 glucose syrups, creating price the primary competitive lever. Unlike specialty sweeteners such as allulose or tagatose, which command premium pricing through unique functional or metabolic properties, glucose is perceived as a bulk commodity with minimal branding potential. As per the European Commission’s competition authority, major producers have been scrutinized for potential price coordination due to the homogeneous nature of the product and high market concentration. This commoditization suppresses margins, with EBITDA rates remaining low for food-grade glucose, according to indusattempt financial disclosures. While some players attempt differentiation through sustainability certifications, such as ISCC or non-GMO, the cost premium rarely offsets raw material volatility. Consequently, investment in R and D for novel glucose derivatives remains limited compared to fructose or polyol segments. Without breakthrough applications that unlock functional uniqueness or regulatory exclusivity, the market will remain trapped in a low-margin, high-volume cycle, vulnerable to substitution and external shocks.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.96% |

|

Segments Covered |

By Source, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Cargill, Incorporated, Archer Daniels Midland Company, Tate & Lyle PLC, Roquette Frères, Ingredion Incorporated, Tereos Group, Südzucker AG, Agrana Beteiligungs-AG, BENEO GmbH, Gulshan Polyols Ltd. |

SEGMENTAL ANALYSIS

By Source Insights

The wheat starch segment accounted for 50.8% of the regional market share in 2025. The dominating position of the wheat starch segment in the European market is driven by Europe’s agronomic structure, where wheat is the most widely cultivated cereal. Unlike North America, which relies heavily on corn, Europe’s Common Agricultural Policy historically incentivized wheat production, which is creating abundant and cost-stable feedstock for starch processors. As per the European Commission’s crop statistics, wheat production in countries like France, Germany, and Poland remains substantial, with a notable share diverted to non-food industrial applys, including starch extraction. Wheat starch also aligns with EU sustainability goals, as it utilizes co-products from flour milling that would otherwise be animal feed. Additionally, wheat-derived glucose carries a non-GMO assurance, which is critical in European markets where consumer resistance to genetically modified corn remains high. As per the European Consumer Organisation, a majority of EU consumers prefer products labeled as non-GMO, even when scientifically equivalent. This feedstock availability, regulatory alignment, and consumer preference collectively cement wheat starch as the primary glucose source in Europe.

The corn starch segment is the rapidest-growing source segment in the Europe glucose market and is estimated to record a CAGR of 5.15% over the forecast period. The growth of the corn starch segment in the European market can be credited to the growing demand for high dextrose equivalent glucose syrups applyd in industrial fermentation and confectionery applications, where corn offers superior saccharification yields compared to wheat. As per Eurostat, corn cultivation in Europe is compacter in scale, but its starch content is higher than wheat, enabling more efficient glucose production per ton of raw material. Moreover, the bioplastics sector increasingly prefers corn-derived glucose due to its consistent amylopectin profile, which enhances lactic acid fermentation efficiency. Companies like Corbion in the Netherlands source non-GMO corn under traceable supply contracts to meet EU bio-based product certification requirements. As per the European Bioplastics Association, corn-based polylactic acid production has been growing steadily, which is fueled by demand from packaging giants seeking renewable content. As precision fermentation for alternative proteins scales, corn starch offers a reliable, high-purity feedstock, driving its accelerated adoption despite Europe’s traditional wheat dominance.

By Application Insights

The food and beverages segment commanded the highest share of 66.6% of the regional market in 2025. Glucose is a foundational ingredient across confectionery, bakery, dairy, and beverage categories due to its functional properties, including controlled crystallization, moisture retention, and rapid fermentability. In baked goods, glucose syrup prevents staling and enhances browning, while in sports drinks, crystalline dextrose provides immediate energy with minimal osmotic load. As per the European Commission, glucose usage in EU food manufacturing remains significant, with confectionery alone consuming large volumes for chewy candies and fondants that require non-crystallizing syrups. The segment’s scale is further reinforced by glucose’s role as a fermentation substrate in yogurt, kefir, and sourdough production, where it feeds lactic acid bacteria to develop flavor and texture. Unlike artificial sweeteners, glucose is exempt from EU maximum usage limits and carries a clean label appeal, as “glucose syrup from wheat” resonates with consumers seeking recognizable ingredients. This deep integration into traditional and functional food systems ensures its continued dominance, despite sugar reduction trfinishs.

The pharmaceuticals segment is the rapidest growing application in the Europe glucose market and is expected to exhibit a CAGR of 8.18% over the forecast period. The irreplaceable role of glucose as an excipient in solid and liquid formulations, and as a critical nutrient in biopharmaceutical cell culture media are driving the expansion of pharmaceuticals segment in the European market. In parenteral nutrition, glucose solutions provide essential caloric support to hospitalized patients across the EU, as documented by the European Society for Clinical Nutrition and Metabolism. More significantly, the continent’s expanding biomanufacturing capacity for monoclonal antibodies, vaccines, and recombinant proteins relies on high-purity glucose to maintain cell viability in bioreactors. As per BioPhorum, European bioreactor capacity has been expanding rapidly, with each large batch requiring substantial amounts of pharma-grade dextrose. The European Pharmacopoeia’s strict monograph 0750 mandates finishotoxin levels below defined thresholds, driving demand for dedicated, non-shared production lines. With the EU’s Critical Medicines Act allocating billions of euros to strengthen biomanufacturing resilience, glucose’s status as a mission-critical raw material ensures premium growth, insulated from food sector volatility.

REGIONAL ANALYSIS

France Glucose Market Analysis

France led the glucose market in Europe in 2025 by accounting for 25.1% of the regional market share. The leadership of France in the European market is anchored in its position as the EU’s top wheat producer and home to global starch processors like Tereos and Roquette. These companies operate integrated biorefineries in the Hauts de France and Grand Est regions, converting large volumes of cereals annually into glucose syrups, dextrose, and bio-based derivatives. France’s strategic alignment with the Farm to Fork Strategy has accelerated investment in non-GMO, traceable glucose for food and fermentation applys. As per indusattempt reports, Tereos has expanded glucose production capacity dedicated to precision fermentation feedstock for alternative protein startups. The French Agency for Food, Environmental, and Occupational Health and Safety maintains stringent purity standards that position French glucose as a premium for pharmaceutical applications. With a significant share of EU glucose exports originating from France, and strong R and D collaboration with INRAE, the counattempt remains the continent’s agricultural and industrial nucleus for glucose value chains.

Germany Glucose Market Analysis

Germany held the second largest share of the Europe glucose market in 2025. The counattempt’s demand is driven less by food applications and more by its world-class industrial biotechnology and pharmaceutical sectors. Numerous biotech firms, including Evonik, BASF, and BRAIN Biotech, operate fermentation facilities that consume high-purity glucose for producing enzymes, amino acids, and biopolymers. Germany also hosts Europe’s largest biopharmaceutical manufacturing base, with companies like BioNTech and CureVac requiring glucose-based cell culture media for mRNA and protein production. As per the German Chemical Indusattempt Association, industrial glucose demand has been growing rapider than food sector demand. Domestic starch processors like AGRANA and Cargill Germany source wheat under long-term contracts, ensuring stable feedstock. The German government’s National Research Strategy BioEconomy 2030 has allocated substantial funding to bio-based production systems, further solidifying glucose’s role as a renewable carbon source. This industrial orientation builds Germany a high-value strategic market beyond traditional food applys.

Netherlands Glucose Market Analysis

The Netherlands is estimated to grow at a promising CAGR in the European glucose market over the forecast period, owing to its role as a logistics and export hub, featuring Europe’s largest starch processing cluster in the port of Rotterdam. Companies like CSM and Corbion operate state of the art glucose plants that process imported and domestic wheat and corn into food-grade and fermentation-grade dextrose for distribution across Europe and globally. As per indusattempt reports, Corbion’s Delfzijl facility produces large volumes of lactic acid annually from glucose, feeding the EU’s bioplastics demand. The Netherlands also leads in precision fermentation, with startups utilizing Dutch glucose to produce animal-free proteins. The Dutch Minisattempt of Agriculture’s circular agriculture policy mandates full traceability of starch feedstocks by 2026, driving investment in blockchain-enabled supply chains. With the Port of Rotterdam handling a majority of EU glucose exports and strong integration into Gaia-X data infrastructure, the Netherlands functions as Europe’s glucose distribution and innovation nexus.

Italy Glucose Market Analysis

Italy is predicted to account for a prominent share of the European glucose market during the forecast period. The counattempt’s demand is shaped by its dense network of compact and medium food manufacturers specializing in confectionery, bakery, and dairy products that rely on glucose syrup for texture and shelf life. Thousands of artisanal candy producers in regions like Lombardy and Emilia Romagna apply glucose syrups to create traditional torrone and soft jellies that require non-crystallizing sugars. Italy also produces significant volumes of wheat annually, with a notable share grown under non-GMO protocols ensuring clean label compliance. The Italian Minisattempt of Health’s guidelines for school meals recommfinish glucose over sucrose in children’s snacks, due to lower cariogenicity, which is boosting institutional demand. Additionally, southern Italy’s growing biotech sector is piloting glucose-based fermentation for natural preservatives. With strong artisanal food traditions and increasing regulatory support for functional sugars, Italy maintains steady glucose consumption rooted in culinary heritage and public health alignment.

United Kingdom Glucose Market Analysis

The United Kingdom is expected to register a healthy CAGR in the European glucose market over the forecast period. Despite Brexit, the UK remains a key consumer due to its advanced pharmaceutical indusattempt and leadership in sports nutrition. A majority of the UK’s glucose imports are pharma-grade dextrose, applyd by companies like GSK and AstraZeneca in tablet formulations and intravenous solutions. The UK is also home to Europe’s largest sports nutrition market, with brands like Science in Sport and Myprotein utilizing crystalline glucose in isotonic drinks and recovery gels. As per the European Specialist Sports Nutrition Alliance, glucose is widely listed as the primary carbohydrate in UK sports drinks. Post Brexit, the UK adopted its own sugar reduction strategy but exempted glucose in clinical and performance contexts, recognizing its metabolic necessity. The Medicines and Healthcare products Regulatory Agency enforces strict finishotoxin limits, aligning with European Pharmacopoeia standards, ensuring continued demand for high-purity glucose. With London emerging as a biomanufacturing cluster and strong R and D links to universities, the UK sustains a specialized, high-value glucose niche focapplyd on health and performance applications.

COMPETITION OVERVIEW

The Europe glucose market is characterized by an oligopolistic structure dominated by large agricultural cooperatives and integrated starch processors with deep ties to regional farming systems. Competition is shaped by access to non-GMO cereal feedstock, technological capability in purification and functional modification, and compliance with stringent EU food and pharma standards. While price remains a factor, differentiation increasingly hinges on sustainability certifications, traceability, and application-specific formulations for emerging sectors like precision fermentation. Barriers to enattempt are high due to capital-intensive biorefinery requirements, long-term farmer contracts, and regulatory validation processes. The market exhibits moderate rivalry as incumbents focus on vertical integration and value-added derivatives rather than volume competition. However, pressure from sugar reduction policies and consumer misperception of glucose as “added sugar” constrains traditional food application,s driving players toward higher margin industrial and health segments. This strategic pivot defines a competitive environment that rewards innovation agil,ity and alignment with Europe’s bio economy and health priorities.

KEY MARKET PLAYERS

A few major players of the Europe glucose market include

- Cargill

- Incorporated

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Roquette Frères

- Ingredion Incorporated

- Tereos Group

- Südzucker AG

- Agrana Beteiligungs-AG

- BENEO GmbH

- Gulshan Polyols Ltd

Top Strategies Used by the Key Market Participants

Key players in the Europe glucose market are investing in non-GMO and traceable feedstock sourcing to meet clean label and regulatory demands across the food and pharmaceutical sectors. Companies are expanding production capacity specifically for high-purity glucose tailored to precision fermentation and biopharmaceutical applications. Vertical integration from agricultural raw materials to finished ingredients ensures supply chain resilience and cost control. Strategic partnerships with alternative protein and bioplastics startups create new high-growth outlets beyond traditional food applys. Additionally, firms are implementing digital traceability systems utilizing blockchain to certify sustainability and origin, enhancing transparency for EU consumers and regulators. These strategies collectively address market diversification, sustainability compliance, and value addition in a competitive and evolving landscape.

Leading Players in the Market

- Tereos is a French agricultural cooperative and a leading global producer of starch, glucose, and bio-based ingredients with extensive operations across Europe. The company processes over 7 million metric tons of wheat, corn, and potatoes annually through its 20+ biorefineries in France, Belgium, and Germany to produce food-grade glucose syrups, crystalline dextrose, and fermentation feedstocks. In 202,4 Tereos commissioned a dedicated non-GMO glucose line at its Vic-sur-Aisne facility to supply precision fermentation startups developing alternative proteins. The company also launched a traceability platform utilizing blockchain to certify the origin and sustainability of its glucose for pharmaceutical and clean-label food customers. Through vertical integration from farm to formulation, Tereos strengthens its position as a reliable producer of high-purity glucose aligned with EU agricultural and health policies.

- Roquette is a France-headquartered global leader in plant-based ingredients with a strong footprint in the European glucose market through its extensive starch processing network. The company produces a wide range of glucose products, including pharma-grade dextrose for parenteral nutrition and high-purity syrups for confectionery and fermentation applications. In 2023, Roquette expanded its Lestrem biorefinery to increase glucose capacity by 90000 metric tons annually with a focus on bio-based chemicals and clinical nutrition. The firm also partnered with the European Society for Clinical Nutrition to develop glucose formulations for geriatric oral supplements addressing malnutrition in aging populations. By leveraging its expertise in pharmaceutical excipients and sustainable starch sourcing, Roquette reinforces its dual leadership in health and industrial glucose segments across Europe.

- AGRANA Group is an Austria-based international producer of starch, fruit, and sugar products with significant glucose operations in Germany, Hungary, and Romania. The company supplies glucose syrups and dextrose to the food, beverage, and fermentation industries across Central and Eastern Europe. In 2024, AGRANA launched a new high-dextrose-equivalent glucose syrup optimized for lactic acid fermentation applyd in bioplastics production under its AGRANA Starch division. The firm also enhanced its wheat starch processing in Zörhuge, Germany, to achieve full non-GMO certification, meeting EU clean label demands. AGRANA’s strategy focapplys on regional integration utilizing locally sourced cereals and providing tailored glucose solutions for compact and medium food manufacturers. This localized yet technologically advanced approach allows AGRANA to serve diverse European markets with agility and compliance.

MARKET SEGMENTATION

This research report on the Europe glucose market has been segmented and sub-segmented based on source, application, and region.

By Source

- Corn Starch

- Wheat Starch

- Others

By Application

- Food and Beverages

- Pharmaceuticals

- Beauty and Cosmetics

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe