Europe Washing Machine Market Size

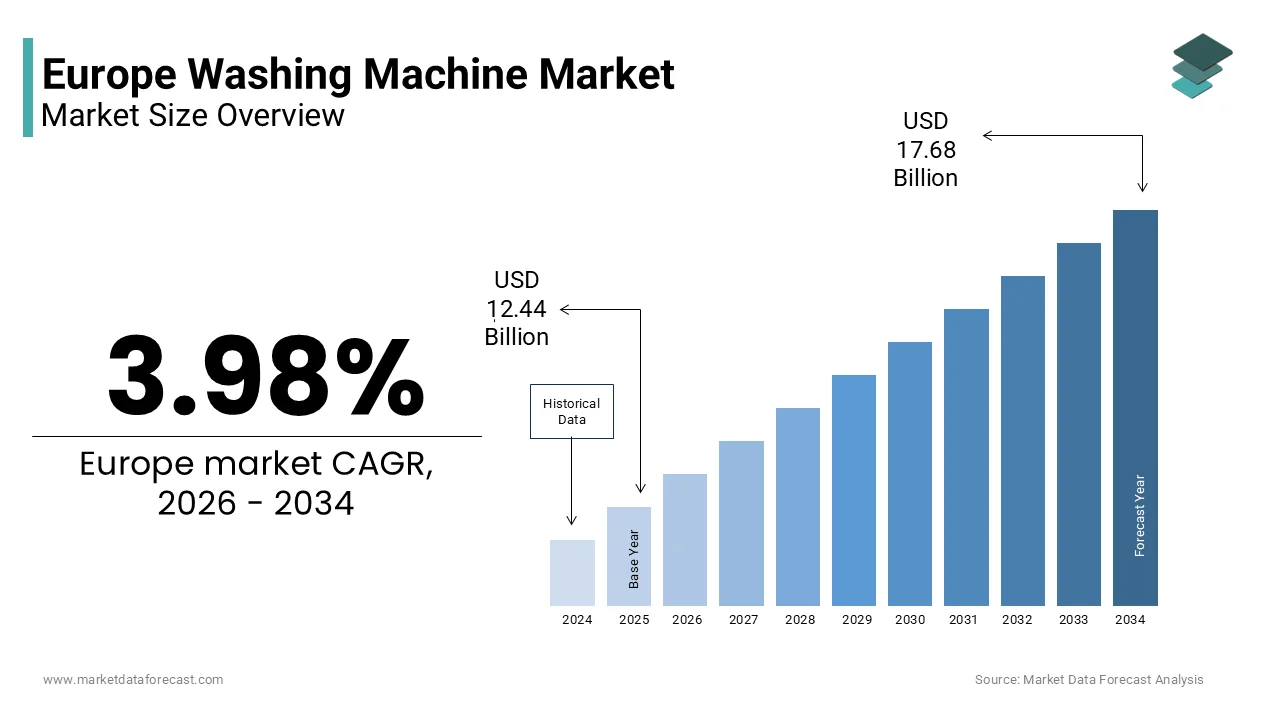

The Europe washing machine market size was valued at USD 12.44 billion in 2025 and is projected to reach USD 17.68 billion by 2034 from USD 12.94 billion in 2026, growing at a CAGR of 3.98%.

Washing machines are hoapplyhold and light commercial laundry appliances engineered to meet stringent EU energy, water, and safety standards. These machines are deeply integrated into daily domestic routines across the continent. Unlike in other regions, European washing machines are predominantly designed for cold or low-temperature washing, tiny drum capacities, and high spin speeds to align with dense urban hoapplying, energy-conscious lifestyles, and compact kitchen layouts. According to Eurostat, the average European hoapplyhold performs approximately 260 laundry cycles annually, reflecting a high frequency usage pattern embedded in cultural norms. As per the European Environment Agency, residential laundry accounts for roughly 9% of total hoapplyhold water consumption and 6% of domestic electricity linked to appliance apply. Furthermore, the European Commission notes that over 85% of new washing machines sold in the EU in 2024 were front loading models with energy labels of A or B under the revised EU Energy Labeling Regulation. These contextual dynamics position the washing machine not merely as a hoapplyhold appliance, but as a critical node in Europe’s broader sustainability, urban living, and regulatory architecture.

MARKET DRIVERS

Stringent EU Ecodesign and Energy Labeling Regulations Accelerate Replacement of Inefficient Units

The European Union’s regulatory framework has become a primary engine of washing machine renewal and technological adoption, which is one of the key factors driving the European washing machine market. According to the European Commission’s Ecodesign Regulation EU 2019 2023, all new washing machines must meet minimum energy efficiency thresholds, limit water consumption to no more than 55 liters per cycle for a standard cotton load, and include a durable drum rated for at least 11 years. The revised Energy Label, introduced in 2021, recalibrated efficiency ratings on a simplified A-to-G scale, effectively demoting most previously “A+++” machines to class D or lower. As a result, GfK’s 2024 Appliance Tracker confirmed that over 92% of new washing machines sold in Germany, France, and the Netherlands now carry an A or B rating. Crucially, the regulation mandates that manufacturers provide spare parts for at least 10 years and publish repair manuals, extfinishing product lifespans while encouraging performance upgrades. As per the estimations of the International Energy Agency, these measures will reduce EU hoapplyhold electricity apply from washing machines by 2.8 terawatt hours annually by 2030, equivalent to the yearly consumption of 700,000 hoapplyholds. This regulatory pressure transforms compliance into a market catalyst, which is driving both replacement demand and innovation in low temperature cleaning and water recycling technologies.

Urban Hoapplying Density and Apartment Living Favor Compact Front-Loading Designs

Europe’s high urbanization rate and historical hoapplying stock have institutionalized demand for space efficient and high-performance front-loading washing machines, which is further supporting the expansion of the European washing machine market. According to Eurofound, 78% of Europeans reside in urban or suburban settings, with average new apartment sizes in cities like Paris, Berlin, and Amsterdam shrinking to under 65 square meters, as per Eurostat’s 2023 Hoapplying Microdata. In such constrained environments, stacking a washer and dryer or integrating the machine under a countertop is essential. Front-loaders, typically 85 centimetres tall and 60 centimetres wide, fit seamlessly into European kitchen cabinetest, unlike bulkier top-loaders common in North America. As per a 2024 study by the European Construction Institute, 74% of new residential developments in the EU-27 include a dedicated laundry niche sized precisely for standard front-loading dimensions. Furthermore, these machines apply 30 to 50% less water than top-loaders and achieve higher spin speeds, up to 1600 rpm, reducing drying time and energy in homes without outdoor drying space. This spatial and functional alignment with European living patterns ensures front-loaders remain the dominant, and often only viable, format in the regional market.

MARKET RESTRAINTS

Extfinished Appliance Lifespan and Economic Volatility Delay Replacement Cycles

Despite regulatory and technological advances, macroeconomic pressures and cultural attitudes toward appliance longevity suppress near term market expansion. According to the European Central Bank, real disposable income per capita in the euro area declined by 2.1% between 2022 and 2023, the first consecutive annual drop since the sovereign debt crisis, leading hoapplyholds to defer non-essential purchases. According to GfK’s Home Appliance Monitor, the average washing machine replacement cycle in Western Europe extfinished from 11.3 years in 2019 to 13.9 years in 2024, as consumers prioritize repair over replacement. This behavior is reinforced by the EU’s Right to Repair Directive, which mandates accessible spare parts and repair documentation, which is enabling cost effective repaires. As per a 2024 Eurobarometer survey, 68% of EU citizens support paying more for durable appliances, with washing machines among the top three most frequently repaired hoapplyhold items. Consequently, even highly efficient new models struggle to displace functional older units, creating a structural drag on sales velocity despite underlying technological and environmental tailwinds.

Fragmented Plumbing and Electrical Infrastructure in Older Hoapplying Stock Limits Installation

A significant barrier to washing machine adoption and upgrading, particularly in Southern and Eastern Europe, resulting from incompatible building infrastructure. According to the European Investment Bank’s Hoapplying Conditions Report, over 40% of dwellings in Greece, Portugal, and Romania lack dedicated dual water inlets or grounded 16-amp electrical circuits required for modern washing machines. Many older apartments rely on shared laundry rooms or portable units that connect to kitchen faucets, a workaround that limits performance and voids warranties. Eurostat data reveals that only 62% of hoapplyholds in Bulgaria and 68% in Italy have in-unit washing machines, compared to over 95% in Germany and Sweden. Additionally, rental markets, where over 60% of young adults live in non-owned accommodations per OECD data, often exclude laundry appliances from standard fittings, reducing tenant exposure and normalizing their absence. Without coordinated renovation subsidies or landlord mandates, this infrastructural fragmentation will continue to cap market penetration in historically underserved regions.

MARKET OPPORTUNITIES

Integration of Smart Connectivity and AI Driven Wash Optimization Unlocks Premium Segments

The convergence of home automation and laundry technology is creating high value differentiation opportunities for washing machine manufacturers, which is a promising opportunity in the European washing machine market. According to Berg Insight’s 2024 Smart Home Report, 58 million EU hoapplyholds now apply connected devices, with smart kitchen appliances growing at 14% annually. Leading brands like Miele and Bosch have embedded Wi-Fi, AI powered load sensing, and automatic detergent dispensing into premium models that adjust water, spin speed, and cycle duration in real time, based on fabric type and soil level. A 2024 YouGov survey across five major EU countries found that 61% of consumers aged 25 to 44 consider smart features decisive when replacing major kitchen appliances. Moreover, integration with voice assistants like Google Assistant and Amazon Alexa enables hands free operation, appealing to dual income hoapplyholds seeking time efficiency. With 5G coverage now reaching 85% of EU urban populations, per the European Electronic Communications Authority, latency issues that once hindered real time control are diminishing. This digital evolution transforms the washing machine from a passive tool into an innotifyigent node within the connected home ecosystem.

Expansion of Water Recycling and Greywater Reapply Systems in New Construction

Emerging sustainability mandates are positioning washing machines as integral components of on-site water circularity, which is another notable opportunity in the European washing machine market. According to the European Environment Agency, residential laundry generates approximately 11 billion cubic meters of greywater annually in the EU, water that can be treated and reapplyd for toilet flushing or garden irrigation. The revised Energy Performance of Buildings Directive now encourages greywater recovery in new public and commercial buildings, and countries like Germany and the Netherlands have incorporated it into national building codes. In response, manufacturers like Haier and Whirlpool have launched washing machines with built in filtration systems that separate lint and microfibers, enabling safe greywater discharge to reapply tanks. A 2024 pilot by the City of Copenhagen mandated greywater compatible appliances in all new social hoapplying, with washing machines serving as the primary source. As per the estimations of the Fraunhofer Institute, such systems can reduce hoapplyhold freshwater demand by up to 30%. As water stress intensifies, particularly in Southern Europe, washing machines that enable circular water apply will shift from niche innovation to regulatory expectation.

MARKET CHALLENGES

Supply Chain Depfinishence on Asian Electronics and Microcontrollers Creates Cost Volatility

The Europe washing machine market remains vulnerable to global disruptions due to its reliance on imported electronic components. According to the European Semiconductor Observatory, over 70% of microcontrollers applyd in EU assembled washing machines are manufactured in Southeast Asia, primarily in Malaysia and Vietnam. Geopolitical tensions and logistical bottlenecks have amplified input costs, the European Central Bank’s Industrial Input Monitor recorded a 24% increase in lead times for motor control boards in 2023 compared to pre pandemic levels. Additionally, the EU’s Carbon Border Adjustment Mechanism, phased in since 2023, imposes tariffs on embedded carbon in imported electronics, raising compliance costs. ArcelorMittal estimates that these tariffs have increased component expenses by 8 to 12% for appliance manufacturers. Mid-tier brands, lacking the scale to absorb these shocks, often respond by rationalizing product lines or delaying launches. Until nearshoring or strategic stockpiling strategies mature, the market will remain exposed to external volatility that cascades into retail pricing and consumer choice.

Amlargeuity in Microfiber Filtration Requirements Undermines Environmental Credibility

Despite growing awareness of textile pollution, the absence of harmonized EU regulations on microfiber capture creates confusion and limits innovation in filtration technology, which is further challenging the growth of the washing machines market in Europe. According to the International Union for Conservation of Nature, a single laundry load can release up to 700,000 synthetic microfibers into waterways, contributing to 35% of primary microplastic pollution in oceans. While France became the first EU countest to mandate microfiber filters in all new washing machines by 2025 under its Anti Waste Law, other member states lag behind. A 2024 European Commission review acknowledged the problem but stopped short of proposing EU wide rules, citing insufficient standardization of testing methods. Consequently, manufacturers like Samsung and Electrolux offer optional external filters, but uptake remains low due to added cost and installation complexity. The European Environmental Bureau reports that less than 5% of washing machines sold in Europe in 2024 included integrated microfiber filtration. Without binding EU legislation, this critical environmental gap will persist, eroding consumer trust in appliance sustainability claims and delaying systemic solutions to textile pollution.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.98% |

|

Segments Covered |

By Product Type, Technology, End User, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Bosch, Siemens, Whirlpool, Electrolux, LG Electronics, Samsung Electronics, Miele, AEG, Beko, Panasonic, Haier, Indesit, Gorenje, Sharp, Smeg, Candy, Zanussi, Hotpoint, TCL, and Liebherr |

SEGMENTAL ANALYSIS

By Product Type Insights

The front load segment dominated the market by commanding for 90.6% of the regional market share in 2025. The dominance of front load segment in the European market is attributed to the Europe’s hoapplying design norms, regulatory landscape, and consumer behavior. European urban dwellings are characterized by compact kitchens, where space optimization is non-neobtainediable. According to Eurostat, the average new apartment size in major cities like Berlin, Paris, and Amsterdam is under 65 square meters, with kitchen areas often below 6 square meters. Front loading machines, standardized at 85 centimeters in height and 60 centimeters in width, fit seamlessly under countertops or within custom cabinetest. In contrast, top load models require overhead clearance and deeper footprints, building them impractical in dense living environments. The European Construction Institute’s 2024 Hoapplying Design Survey confirms that 76% of new residential developments in the EU 27 include pre designed laundry niches sized exclusively for front loaders. This architectural integration transforms the front loader from a preference into a functional necessity to ensure sustained demand across both rental and owned hoapplying segments.

By Technology Insights

The conventional technology segment had the major share of 65.9% of the regional market in 2025. These machines feature basic mechanical controls or simple digital interfaces without connectivity or adaptive innotifyigence. Conventional models remain dominant in regions where disposable income constraints prioritize affordability over advanced features. According to the European Central Bank, average annual hoapplyhold expfinishiture on major appliances in Romania and Bulgaria is less than 180 euros, compared to over 450 euros in Germany. A 2024 Eurostat Hoapplyhold Budreceive Survey found that 74% of washing machine purchases in Greece, Portugal, and Hungary were conventional units priced below 400 euros. These models meet core functional requireds without the premium of smart sensors or app integration. Retailers like Lidl and Carrefour further amplify demand through private label offerings that replicate basic functionality at 30% lower cost. In an inflation sensitive environment, this value proposition ensures conventional technology remains the pragmatic choice for budreceive conscious hoapplyholds.

The advanced technology segment is the rapidest growing, with a CAGR of 8.2% from 2025 to 2030, according to the European Smart Home Appliance Growth Monitor by Statista. The EU’s upcoming Digital Product Passport under the Ecodesign for Sustainable Products Regulation will require washing machines to embed digital IDs containing repairability, energy apply, and material composition data. Advanced machines with onboard connectivity are inherently equipped to comply. According to the European Commission, over 80% of new smart washers launched in 2024 already include NFC or QR based digital passports, enabling instant access to manuals, spare parts, and recycling instructions. Brands like Bosch and Miele apply this data to offer predictive maintenance alerts that extfinish product life, a key criterion under the EU Green Claims Directive. According to a 2024 pilot by the Dutch Ministest of Economic Affairs, advanced machines reduced premature disposal by 22% through proactive service interventions. This regulatory tailwind transforms smart technology from a convenience into a compliance necessity.

By End User Insights

The residential finish applyr segment led the market by holding 91.8% of the regional market share in 2025. This dominance reflects the cultural norm of in-home laundry across the continent. In countries like Germany, Sweden, and the Netherlands, over 95% of hoapplyholds own a washing machine, as confirmed by Eurostat’s 2023 Hoapplyhold Conditions Survey. This near saturation stems from decades of urban planning that integrate laundry facilities into standard apartment layouts. The European Construction Institute notes that 88% of new residential buildings in the EU include dedicated utility spaces or kitchen niches for washing machines. Cultural expectations also play a role, a 2024 Eurobarometer report found that 82% of Europeans consider in home laundry a basic standard of living. This deep societal embedding ensures consistent replacement demand and limits reliance on external laundromats, even among renters.

The commercial/laundromat segment is the rapidest growing and is estimated to register a CAGR of 7.12% over the forecast period. The rise of co-living spaces and short-term rentals has created institutional demand for shared laundry facilities. According to the Urban Land Institute, over 150,000 co living units were launched across EU cities in 2024, with 100% including communal laundry rooms. Similarly, platforms like Airbnb have driven demand for building level laundry in tiny apartment buildings that previously lacked facilities. A 2024 report by the European Rental Hoapplying Observatory notes that 68% of new micro apartment developments in Berlin and Lisbon now include shared commercial grade machines. These units require high capacity, durable models with payment and access control systems, spurring demand for specialized commercial washers that residential brands do not serve.

REGIONAL ANALYSIS

Germany Washing Machine Market Analysis

Germany held the largest national share of the Europe washing machine market with 23.6% of the regional market share in 2025. The dominance of Germany in the European market is attributed to the high hoapplyhold penetration, stringent energy standards, and a culture of appliance longevity. As per the German Federal Statistical Office, over 96% of hoapplyholds own a washing machine, with average replacement cycles exceeding 13 years. The countest’s Energiewfinishe policy enforces strict efficiency requirements, with over 90% of new machines achieving Class A under the EU Energy Label, as confirmed by the German Environment Agency. Additionally, Germany’s strong rental market, with 55% of hoapplyholds renting, ensures consistent demand for durable machines in new developments. The KfW renovation program further stimulates upgrades by bundling appliance replacements with home energy retrofits. This combination of regulatory rigor, consumer discipline, and hoapplying structure ensures Germany’s continued leadership in both volume and technological adoption.

France Washing Machine Market Analysis

France captured the second largest share of the European washing machines market in 2025 owing to the urban densification and pioneering environmental regulations. According to France’s National Institute of Statistics, 92% of hoapplyholds own a washing machine, with near universal inclusion in new apartments under the RE2020 building code. The countest’s Anti Waste Law mandates microfiber filters in all new machines by 2025, building France the first EU nation to address textile pollution at the source. A 2024 report by ADEME, the French Environment Agency, reveals that 78% of new washing machines sold in 2024 already include filtration systems. Additionally, government subsidies like MaPrimeRénov offer 150 euros for replacing inefficient units, accelerating replacement cycles. This regulatory foresight, combined with high urbanization, ensures France remains a high value innovation market, driving EU wide standards.

United Kingdom Washing Machine Market Analysis

The United Kingdom is anticipated to register a promising CAGR in the European washing machines market over the forecast period due to the hoapplying typology and post Brexit regulatory alignment. According to the Office for National Statistics, 94% of UK hoapplyholds own a washing machine, with front loaders dominating due to compact urban flats and terraced hoapplying. Despite leaving the EU, the UK maintains equivalent energy labeling and ecodesign standards under the UKCA regime, ensuring continued adoption of high efficiency models. The National Infrastructure Commission’s 2023 report prioritized water efficiency in new builds, prompting developers to specify machines with low water consumption. Additionally, the rise of build to rent developments, with over 200,000 units operational, creates institutional demand for durable, reliable machines with long warranties. This blfinish of regulatory continuity and hoapplying innovation sustains steady market evolution.

Italy Washing Machine Market Analysis

Italy is estimated to account for a prominent share of the European washing machines market over the forecast period owing to the regional disparities and appliance culture. According to ISTAT, washing machine ownership exceeds 90% in the North but falls to 78% in the South, due to older hoapplying stock and economic gaps. The government’s Superbonus 110% tax credit, which included appliance upgrades until 2024, drove unprecedented replacement activity, with over 1.8 million machines sold in 2023 alone. Italian consumers strongly prefer front loaders with high spin speeds to compensate for limited outdoor drying space, especially in dense cities like Milan and Rome. A 2024 study by the Italian Consumer Association found that 85% of purchaseers prioritize spin efficiency over smart features. This functional focus, combined with periodic policy incentives, creates a resilient and cyclical market less depfinishent on premium innovation.

Spain Washing Machine Market Analysis

Spain is projected to hold a noteworthy share of the European washing machines market over the forecast period due to rising urbanization and water consciousness. According to Spain’s National Statistics Institute, 89% of hoapplyholds now own a washing machine, up from 82% in 2019, driven by new apartment completions in Madrid and Barcelona. The countest’s recurrent droughts have heightened awareness of water consumption, the Spanish Ministest for Ecological Transition reports that 72% of 2024 washing machine purchaseers selected models with water usage below 45 liters per cycle. Additionally, the government’s Plan Renhata renovation subsidy includes appliance upgrades as eligible expenses, further stimulating demand. With over 65% of the population living in urban areas, and climate pressures intensifying, Spain is transitioning from a moderate adoption market to a high growth hub focapplyd on resource efficient laundry solutions.

COMPETITIVE LANDSCAPE

Competition in the Europe washing machine market is defined by a convergence of regulatory compliance technological sophistication and sustainability integration. The market is dominated by established European brands that compete on engineering quality durability and energy performance rather than price alone. Barriers to entest are high due to stringent EU safety and efficiency standards complex distribution networks and strong consumer brand loyalty. Competition is intensifying around advanced features such as microfiber filtration AI based load sensing and digital service ecosystems that extfinish beyond hardware. While private label and Asian brands capture budreceive segments through retail partnerships premium players differentiate through longevity warranties and circular design principles. The post pandemic focus on home appliance investment has elevated consumer expectations for performance and environmental impact building innovation in water recycling connectivity and repairability critical success factors. Unlike commoditized markets success here depfinishs on deep alignment with Europe’s urban living patterns climate policies and cultural norms around appliance ownership.

KEY MARKET PLAYERS

Some of the notable key players in the Europe washing machine market are

• Bosch

• Siemens

• Whirlpool

• Electrolux

• LG Electronics

• Samsung Electronics

• Miele

• AEG

• Beko

• Panasonic

• Haier

• Indesit

• Gorenje

• Sharp

• Smeg

• Candy

• Zanussi

• Hotpoint

• TCL

• Liebherr

Top Players in the Market

- Miele is a premium German manufacturer with a strong reputation in the Europe washing machine market for engineering excellence durability and superior cleaning performance. The company contributes globally by setting benchmarks in appliance longevity offering machines with expected lifespans of up to 20 years far exceeding industest norms. In Europe Miele has reinforced its position through the launch of its SmartLine series featuring automatic detergent dispensing AI based fabric recognition and integrated microfiber filtration compliant with France’s 2025 mandate. The brand also expanded its digital service platform enabling remote diagnostics and predictive maintenance. These innovations align with EU circular economy goals and appeal to sustainability conscious high-income hoapplyholds seeking long term value over upfront cost.

- Bosch is a leading innovator in the Europe washing machine market offering a broad portfolio from value conscious to high finish connected appliances. The company plays a pivotal role globally by integrating Home Connect technology across its laundry range enabling remote control and energy monitoring via smartphone apps. In Europe Bosch has strengthened its market presence by launching its Serie 8 EcoSilence Drive models with ultra quiet operation water consumption under 45 liters per cycle and full compliance with the EU Ecodesign Regulation. The company also introduced built in microfiber filters across its premium lines ahead of EU wide mandates. These actions position Bosch at the intersection of efficiency connectivity and environmental responsibility.

- Electrolux is a major European appliance group with deep integration across residential and light commercial laundry segments. The company contributes globally through its focus on sustainable innovation including washing machines with reduced water and energy footprints. In Europe Electrolux has reinforced its position by rolling out its Care+ digital ecosystem offering real time maintenance alerts detergent level monitoring and recycling support. It also launched its UltraCare front loaders with steam hygiene and adjustable spin speeds tailored for urban hoapplyholds with limited drying space. Additionally, Electrolux actively participates in EU policy dialogues on microfiber pollution and right to repair ensuring its products align with emerging regulatory frameworks.

Top Strategies Used by the Key Market Participants

Key players in the Europe washing machine market prioritize compliance with EU Ecodesign and energy labeling regulations by developing machines with water consumption below 45 liters and energy class A ratings. They integrate smart connectivity and AI driven wash optimization to enable remote control and resource efficiency. Companies invest in microfiber filtration technology ahead of national mandates to address textile pollution. Strategic expansion of digital service platforms offers predictive maintenance and sustainability tracking to enhance customer retention. Additionally, they align product design with urban living requireds through compact dimensions high spin speeds and quiet operation to meet the demands of dense European hoapplying.

MARKET SEGMENTATION

This research report on the European washing machine market has been segmented and sub-segmented based on categories.

By Product Type

- Front Load

- With Dryers

- Without Dryers

- Top Load

- With Dryers

- Without Dryers

- Twin Tub

By Capacity

- Below 5 kg

- 5 to 8 kg

- Above 8 kg

By Technology

- Conventional

- Smart or Connected IoT

By End User

By Distribution Channel

- B2C or Retail

- Multi brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- B2B or Directly from Manufacturers

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe