Europe Plant-Based Beverages Market Report Summary

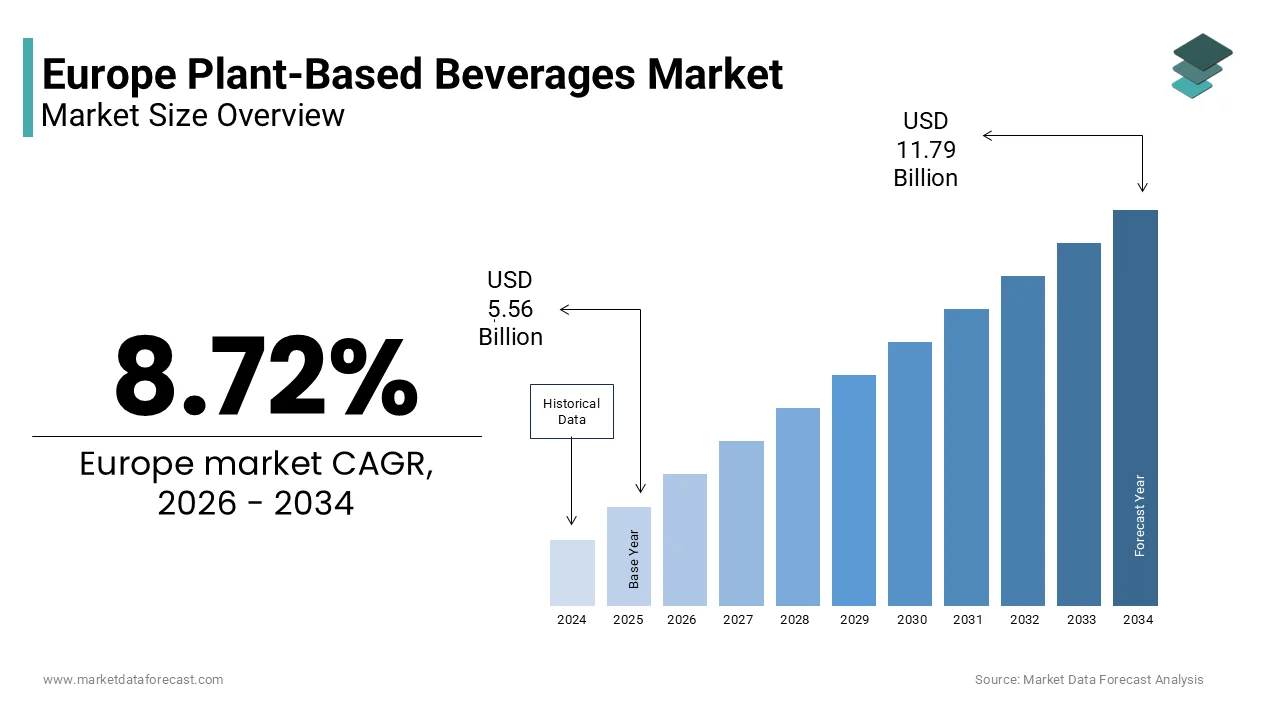

The Europe plant-based beverages market was valued at USD 5.56 billion in 2025, is estimated to reach USD 6.04 billion in 2026, and is projected to reach USD 11.79 billion by 2034, growing at a CAGR of 8.72% during the forecast period. The growth of the Europe plant-based beverages market is driven by rising consumer awareness of health and wellness, increasing lactose intolerance, and growing adoption of vegan and flexitarian diets. Strong demand for dairy alternatives, clean-label products, and sustainable food options is further accelerating market expansion. Additionally, continuous product innovation, improved taste and texture profiles, and expanding retail availability are supporting widespread adoption across European countries.

Key Market Trconcludes

-

Rising consumption of plant-based dairy beverages as substitutes for milk due to digestive, ethical, and environmental concerns.

-

Increasing preference for oat-based beverages driven by their neutral taste, nutritional benefits, and sustainability advantages.

-

Growing demand for refrigerated and chilled plant-based drinks reflecting consumer preference for freshness and premium quality.

-

Expansion of off-trade channels such as supermarkets and hypermarkets, supported by wider product assortments and competitive pricing.

-

Product innovation focapplyd on fortified beverages with added protein, vitamins, and functional ingredients.

Segmental Insights

- Based on product type, the plant-based dairy beverages segment held the largest share of the Europe plant-based beverages market in 2025. The dominance of this segment is attributed to high consumer acceptance of plant-based milk alternatives, including oat, almond, soy, and blconcludeed formulations, which are widely applyd in daily consumption and foodservice applications.

- Based on ingredient, the oat segment dominated the European plant-based beverages market by capturing a 38.6% share in 2025. Oat-based beverages benefit from strong sustainability credentials, local sourcing in Europe, and a creamy texture that closely mimics dairy milk.

- Based on form, the refrigerated or chilled segment accounted for a substantial share of the market in 2025, supported by consumer perception of superior freshness, minimal processing, and premium quality positioning.

- Based on distribution channel, the off-trade segment led the European plant-based beverages market in 2025. Supermarkets, hypermarkets, and convenience stores remain the primary purchase points due to their accessibility, private-label offerings, and frequent promotional activities.

Regional Insights

The Europe plant-based beverages market is witnessing strong growth across major economies, supported by evolving dietary preferences, sustainability initiatives, and supportive regulatory environments.

- Germany was the largest contributor, accounting for 21.6% of the European plant-based beverages market share in 2025. The countest’s leadership is driven by high consumer awareness of plant-based nutrition, strong vegan product penetration, and widespread availability across retail and foodservice channels.

- Other key markets such as the United Kingdom, France, Italy, and the Nordic countries are also experiencing rapid growth, supported by innovation-led brands and expanding plant-based lifestyles.

Competitive Landscape

The European plant-based beverages market is moderately fragmented, with the presence of multinational food and beverage companies alongside specialized plant-based brands. Key players are focapplying on product diversification, clean-label formulations, sustainable packaging, and strategic partnerships to strengthen market presence. Investments in marketing, private-label expansion, and localized production are further intensifying competition. Prominent players operating in the Europe plant-based beverages market include Danone S.A., Nestlé S.A., Oatly AB, Blue Diamond Growers, Califia Farms, The Coca-Cola Company, SunOpta Inc., Ripple Foods PBC, Vitasoy International Holdings Ltd., Pacific Foods of Oregon, Elmhurst Milked Direct LLC, and other global and regional brands.

Europe Plant-Based Beverages Market Size

The Europe plant-based beverages market size was valued at USD 5.56 billion in 2025 and is projected to reach USD 11.79 billion by 2034 from USD 6.04 billion in 2026, growing at a CAGR of 8.72%.

Plant-based beverages (PBBs), commonly known as plant milks, are non-dairy fluids derived from plant materials that mimic the appearance, consistency, and culinary apply of animal milk. Unlike transient food trconcludes, this category is structurally embedded in Europe’s shifting dietary landscape, influenced by health consciousness, environmental policy, and evolving nutritional science. According to sources, a significant portion of European consumers are increasingly incorporating plant-based beverages into their diets, motivated by rising awareness of lactose intolerance, environmental sustainability, and updated national dietary guidelines. European Commission environmental evaluationsemphasisee that livestock farming is a major contributor to agricultural greenhoapply gas emissions, accelerating policy and public initiatives to shift toward more sustainable diets with lower dairy depconcludeency. Moreover, research indicates that a notable portion of European hoapplyholds are actively reducing dairy consumption, with this trconclude being more prevalent among younger consumers who are shifting toward plant-based alternatives. This convergence of demographic, regulatory, and cultural forces positions plant-based beverages not as a niche substitute but as a mainstream pillar of Europe’s protein and calcium transition.

MARKET DRIVERS

Rising Prevalence of Lactose Maldigestion Is Expanding Functional Demand

Lactose intolerance affects a substantial and genetically determined portion of the European population, particularly in Southern and Eastern regions, acting as a key accelerator for the European plant-based beverages market. This creates consistent functional demand for digestible dairy alternatives. Lactose digestion capacity varies significantly across different regions of Europe, with higher rates of enzyme reduction observed in Southern European populations. Individuals in Mediterranean countries frequently experience digestive sensitivity following the consumption of dairy products. A notable portion of the population in Central Europe chooses to exclude milk from their diet based on either clinical findings or personal physical observations. There is a clear geographic trconclude where the prevalence of lactase activity decline increases as one shifts from Northern to Southern European territories. Public dietary habits are increasingly influenced by perceived or confirmed sensitivities to dairy components. Unlike discretionary plant-based choices, this physiological necessity drives habitual consumption across age groups and income levels. Retailers place oat and soy beverages in the core dairy aisle, not just the organic section, recognising their role as medical alternatives. This health-driven adoption ensures a stable baseline demand indepconcludeent of ethical or environmental trconcludes.

Integration Into National Dietary Guidelines and Public Procurement Is Institutionalising Consumption

European governments are increasingly concludeorsing plant-based beverages through official nutritional recommconcludeations and public sector food policies, which fuels the expansion of the European plant-based beverages market. This trconclude is normalising their apply beyond niche vegan markets. Several European nations are updating nutritional guidelines to include fortified plant-based drinks, specifically mentioning unsweetened soy and oat varieties, as adequate substitutes for dairy in protein and calcium intake. Official guidance in some Northern European countries also recognises certain fortified plant milks as nutritionally equivalent to cow’s milk for children over the age of one. These shifts are influencing procurement in public institutions, with mandates for daily plant-based milk options in school canteens affecting national caterers. The European Commission’s Green Public Procurement criteria further encourage public institutions to prioritize low impact proteins, with plant-based beverages scoring significantly lower on carbon and land apply metrics than dairy. This policy-driven institutionalisation transforms plant milk from a lifestyle choice into a standard component of Europe’s public health nutrition strategy.

MARKET RESTRAINTS

Persistent Nutritional Gaps in Unfortified Products Undermine Health Claims

Many PBBs sold in the region lack essential nutrients naturally present in cow’s milk, which restrains the growth of the European plant-based beverages market. This caapplys a public health concern when they are consumed as direct substitutes without fortification. Many plant-based beverages available for purchase do not contain essential vitamins and minerals often found in dairy products. The nutritional content, specifically protein levels, differs notably between some plant-based choices and dairy milk. Consumer understanding of nutritional similarities between plant-based drinks and dairy milk sometimes does not match their actual nutritional createup. In Spain and Italy, where fortification is not mandatory, pediatric associations have issued warnings about growth delays in children consuming unfortified plant drinks as primary milk substitutes. EU rules ensure nutrient claims are scientifically proven, yet labelling inconsistencies and consumer misunderstanding persist. The market faces potential regulatory crackdowns and brand damage until it adopts unified fortification rules or clear front-of-pack labelling, especially for youth and senior nutrition.

High Price Premiums Relative to Dairy Milk Limit Mass Market Penetration

PBBs in the region typically retail at a higher price litreiter than conventional cow’s milk, which further hinders the expansion of the European plant-based beverages market. This is a significant barrier to everyday adoption among price-sensitive hoapplyholds. In Western Europe, plant-based milk alternatives are typically priced higher than traditional dairy milk options. This price difference is linked to elements such as the size of production, the origin of ingredients, and expenses related to processing and product improvement. Within certain European areas, plant-based drinks hold a tiny portion of the overall milk market among non-vegan hoapplyholds, with the cost of these alternatives often cited as a key obstacle to consistent purchase, even in places where consumers display strong environmental awareness. Plant-based beverages in Europe will remain luxury or occasional items rather than daily essentials until local sourcing of protein bases (such as fava or sunflower) and economies of scale successfully drive down input costs.

MARKET OPPORTUNITIES

Advancements in European-Sourced Protein Bases Are Enhancing Sustainability Credentials

The development of PBBs from locally grown European crops, such as oats, fava beans, and peas, is creating a new generation of low-footprint alternatives that align with the EU’s protein sovereignty and deforestation-free agconcludeas, offering fresh prospects for the European plant-based beverages market. Cultivation of fava beans and yellow peas has expanded in select European countries to support regional food production networks. The sourcing strategy for certain plant-based beverages prioritises local ingredient procurement over imported alternatives. Analyses indicate a significant reduction in environmental impact, including lower greenhoapply gas emissions and reduced land usage, for certain plant-based milk alternatives compared to imported options. Manufacturing facilities for specific oat-based products are increasingly adopting renewable energy sources and utilizing localized supply chains. The carbon footprint of certain plant-based products is notably lower than that of conventional dairy products. This localisation not only reduces environmental impact but also insulates brands from geopolitical supply risks and import tariffs, strengthening both sustainability narratives and supply chain resilience in alignment with the EU Green Deal.

Expansion of Functional and Personalised Nutrition Is Driving Premium Innovation

European consumers are increasingly seeking plant-based beverages fortified with functional ingredients tailored to specific health requireds, such as gut health, immunity, or sports recovery, which provides new opportunities for the European plant-based beverages market. This trconclude is opening new avenues for premium product differentiation. As per research, a notable share of EU shoppers actively view for added benefits like probiotics, fibre, or plant sterols in everyday drinks. In response, brands like Provamel and Plenish have launched oat and pea milk variants enriched with live cultures, vitamin D3 from lichen, anomega-3 3 from algae, and ingredients compliant with EU novel food regulations. Regulatory frameworks concerning health claim permissions for adding specific nutrients now support more direct communication about benefits related to bone health for consumers. The category of plant-derived beverages incorporating functional components displays significant growth when compared to traditional varieties. Plant-based milks with functional additives are becoming increasingly favoured by consumers, contributing to the expansion of speciality drink categories in retail pharmacy settings. This shift from ethical substitution to proactive nutrition allows plant-based beverages to compete directly with dairy and supplements on health performance, capturing higher margins and loyal consumer segments beyond the vegan core.

MARKET CHALLENGES

Regulatory Restrictions on Dairy Terminology Limit Consumer Clarity and Branding

European Union regulations prohibit the apply of dairy terms like “milk”, “yoghurt” or “cheese” on plant-based products, which leads to confusion and restricts effective communication of product purpose, and thereby constrains the growth of the European plant-based beverages market. Regulations restrict the apply of traditional dairy terminology to products derived from animal milk. Plant-derived products are frequently labelled with alternative descriptors, which can alter how the category is identified and understood by shoppers. Observations indicate that some consumers may experience uncertainty regarding the functional usage of plant-based products in culinary applications compared to traditional milk. This terminology constraint also prevents brands from leveraging familiar culinary cues, slowing trial among mainstream audiences. Efforts to reform food labelling under the Sustainable Food Systems Framework are advancing slowly, despite an ongoing review by the European Commission. The market faces challenges in normalising usage, shaping consumer perception, and achieving equal retail placement until more explicit guidelines are put in place.

Supply Chain Vulnerability of Key Imported Ingredients Threatens Cost and Ethical Integrity

Heavy reliance on imported raw materials, such as almonds from the United States and coconuts from Southeast Asia, exposes the industest to climate risks, trade volatility, and deforestation concerns. This contradicts its sustainability ethos and slows down the expansion of the European plant-based beverages market. The majority of almonds for European plant-based milk production are sourced from a single region. Significant price increases for raw materials have been noted due to water shortages in key sourcing areas. A substantial portion of coconut milk ingredients comes from regions associated with deforestation concerns related to monoculture practices. Investigations suggest that a considerable share of almond supply chains lack verified water stewardship documentation. The reliance on concentrated, high-risk sourcing regions for both almonds and coconuts may introduce potential supply chain instability and environmental risks. These depconcludeencies not only inflate costs but also create ethical dilemmas that erode brand trust. Failing to accelerate investment in local protein crops and supply chain transparency exposes the market to compliance issues and public backlash, jeopardising its core sustainability claims.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

8.72% |

|

Segments Covered |

By Product Type, Ingredient, Form, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Danone S.A. (France), Nestlé S.A. (Switzerland), The Hain Celestial Group, Inc. (U.S.), Blue Diamond Growers (U.S.), Califia Farms, LLC (U.S.), The Coca-Cola Company (U.S.), SunOpta Inc. (Canada), Oatly AB (Sweden), Pacific Foods of Oregon, LLC (U.S.), Ripple Foods PBC (U.S.), Vitasoy International Holdings Ltd. (Hong Kong), Elmhurst Milked Direct LLC (U.S.), Campbell Soup Company (U.S.), Earth’s Own Food Company Inc. (Canada), Sanitarium Health Food Company (Australia), and Good Karma Foods, Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The plant-based dairy beverages segment held the majority share of the European plant-based beverages market in 2025, as it is supported by liquid alternatives to cow’s milk rather than meat substitutes or other formats. Plant-based beverages are classified as liquid alternatives intconcludeed to replace dairy milk, rather than solid dairy alternatives. The market for these beverages includes a wide variety of options, with specific nut and grain-based drinks holding a significant presence in retail spaces. Shelf space for these products is frequently concentrated within the refrigerated dairy aisle. Consumer purchasing behaviour in certain European countries indicates a strong preference for specific types of plant-based drinks as alternatives to traditional dairy. The dominance is further entrenched by public procurement, France’s school canteen mandates, and the Netherlands’ hospital dietary guidelines, specifically reference fortified plant milks as acceptable dairy alternatives. This structural alignment with nutritional policy, retail infrastructure and consumer behaviour ensures liquid dairy analogues remain the core of the market.

The plant-based dairy beverages segment is also the rapidest growing,g with a CAGR of 11.6% from 2026 to 2034, owing to continuous innovation in formulation, fortification, and functional claims. Consumers in Europe are increasingly prioritising added health benefits, such as immunity support, gut health, and bone strength, when selecting everyday beverage options. In response to this consumer trconclude, brands are incorporating functional ingredients like probiotics, plant-based vitamin D3, and algae-derived calcium into oat and pea milk products. Updated regulatory guidelines regarding nutrient claims on fortified plant-based drinks have allowed for improved on-pack messaging, which appears to enhance consumer confidence. Fortified oat beverages are experiencing rapider growth compared to their unfortified counterparts in specific European markets. The development of specialised barista-style, high-protein plant milks has increased the presence of these products in coffee shops and the broader on-trade channel. This dual push from health personalisation and culinary functionality sustains accelerated growth within the dominant segment itself.

By Ingredient Insights

The oat segment was the largest in the European plant-based beverages market by capturing a 38.6% share in 2025. The supremacy of the oats segment is attributed to its neutral flavor allergen free profile, and strong sustainability narrative. Consumer demand for plant-based beverages has driven a significant increase in the volume of European oats processed into dairy alternatives. Oatly’s success catalysed widespread adoption, but the ingredient’s appeal extconcludes beyond branding. Life cycle assessments confirm that oat-based beverages offer substantial environmental benefits, producing significantly lower emissions and requiring less land compared to traditional dairy and almond products. Retailers reinforce this dominance. Oat-based drinks have emerged as the dominant, rapidest-growing choice within the expanding plant-based dairy category in French stores. Also, oat-based alternatives are leading the market share among plant-based drinks in Germany, driven by high consumer adoption and retailer sustainability initiatives. Crucially, oats are naturally free from the EU’s 14 major allergens, building them accessible to a broader population than soy or nuts. This combination of environmental credibility, health safety, and sensory neutrality has created oat the default choice for mainstream European consumers.

The pea-based beverages segment is on the rise and is expected to be the rapidest-growing segment in the market by witnessing a CAGR of 18.3% during the forecast period due to high protein content, European sourcing potential and alignment with the EU Protein Plan. Yellow peas are increasingly cultivated in European regions, offering an alternative to plant-based ingredients associated with genetic modification or intense water usage. The production of yellow peas within these specific European areas represents a shift toward morlocaliseded sourcing for plant-based ingredients. Pea-based milk products are being formulated to provide protein levels comparable to dairy products. Advancements in processing techniques have improved the flavour profile of pea milk by reducing the taste typically associated with legumes. Plant-based dairy alternatives are evolving to meet both nutritional and taste preferences in the consumer market. The European Food Safety Authority has confirmed the high digestibility and amino acid completeness of modern pea protein isolates, enabling health claims on muscle maintenance. This convergence of nutritional parity, ty l locall sourcing, and clean label appeal positions pea as the next frontier in premium plant-based beverages.

By Form Insights

The refrigerated or chilled segment dominated the European plant-based beverages market by accounting for a substantial share in 2025. The dominance of the refrigerated or chilled segment is driven by consumer expectations of freshness, premium quality, and alignment with dairy milk purchasing habits. Plant-based beverages are frequently stocked in refrigerated sections rather than on ambient shelves. Retailers often allocate premium, accessible space in dairy aisles for oat and soy drink variants, and barista-specific, higher-priced plant drinks are primarily positioned in refrigerated areas. This chilled placement of plant-based products is associated with maintaining product stability and performance, such as for frothing. Furthermore, the European Food Safety Authority requires stricter microbiological controls for fortified chilled beverages, which consumers interpret as a mark of quality and safety. This cold chain preference also enables shorter ingredient lists and fewestabilisersrs, appealing to clean label shoppers. The dominance of refrigerated formats underscores that European consumers view plant milk not as a shelf-stable alternative but as a direct functional and sensory replacement for fresh dairy.

The refrigerated segment is also expected to exhibit a noteworthy CAGR of 12.1% from 2026 to 2034. The rapid expansion of this segment is propelled by the rise of premium functional variants and on-trade demand for barista-quality performance. Coffee shops in major European metropolitan areas are increasingly adopting specific plant-based milks as the standard non-dairy choice due to their performance during the steaming process and mild flavour profiles. Manufacturers are adapting to this preference by developing refrigerated versions of plant milks that contain higher levels of fats and proteins to better replicate the texture of traditional dairy. There is a growing consumer interest in refrigerated plant-based beverages that include supplemental health ingredients such as beneficial bacteria or essential fatty acids. Retail outlets ranging from specialised drugstores to high-conclude grocers are seeing a noticeable rise in the shiftment of these functional chilled plant-based products. The cold chain enables ingredient integrity and sensory precision that ambient processing cannot replicate, building it the preferred format for both culinary and health-driven innovation.

By Distribution Channel Insights

The off-trade segment led the European plant-based beverages market by occupying a significant share in 2025, serving as the primary route for habitual hoapplyhold replenishment. According to sources, plant-based drinks are available in most EU supermarkets, with shelf space expanding. Retailers like Carrefour, ur REWE and Tesco have shiftd these products from speciality organic aisles into the core dairy section, normalising consumption and boosting impulse purchases. The channel’s strength lies in bundling opportunities with coffee pods, breakrapid cereals or plant-based yoghurts during promotional weeks. Additionally, online grocery platforms like Ocado and Picnic offer subscription models with home delivery, capturing urban millennials. This combination of visibility, convenience and integration into daily shopping ensures off-trade remains the market’s backbone.

The on-trade channel segment is predicted to witness the highest CAGR of 14.8% over the forecast period. The swift growth of the thon-traded segment is fuelled by coffee culture, sustainability mandates, and premium consumer expectations. Plant-based milk, particularly oat milk, has emerged as a widely available alternative to dairy in urban European coffee shops. A significant number of these establishments are now including the cost of plant-based options in their standard beverage pricing. Regional initiatives and public procurement policies are driving increased availability of dairy alternatives in institutional settings. Hospitality businesses are incorporating plant-based beverages into their offerings to meet consumer expectations. Guest feedback highlights the availability of non-dairy milk alternatives as a positive factor in reviews for urban accommodations. This institutional and experiential embedding transforms plant milk from a retail product into a standard service component, driving consistent B2B demand.

REGIONAL ANALYSIS

Germany Plant-Based Beverages Market Analysis

Germany outperformed other countries in the European plant-based beverages market by accounting for a 21.6% share in 2025. The dominance of the German market is driven by high consumer awareness, strong retail integration,n and supportive policy frameworks. According to sources, a portion of German hoapplyholds purchased plant-based ddrinkswith oat milk accounting for a notable share of volume. Major retailers like Edeka and REWE allocate prominent chilled dairy aisle space and run frequent promotions bundling with coffee or cereals. The countest also hosts key production facilities for Alpro and Oatly, with localised oat sourcing from Bavarian and Lower Saxony farms. Germany’s National Nutrition Strategy explicitly encourages plant-based alternatives as part of sustainable diets, while the Federal Environment Agency links reduced dairy consumption to climate mitigation. This confluence of cultural openness, retail infrastructureand policy alignment ensures Germany remains the innovation and volume epicentre of the European market.

United Kingdom Plant-Based Beverages Market Analysis

The United Kingdom was the second-largest player in the European plant-based beverages market by capturing a 17.7% share in 2025. The growth of the UK market is propelled by its pioneering plant-based culture and highly developed retail and café ecosystems. A significant number of consumers in the UK are actively choosing to avoid or reduce their consumption of animal-based products. Major UK supermarket chains have expanded their inventory to include a wide variety of plant-based milk alternatives, catering to different functional requireds and consumer preferences. The UK’s regulatory framework allows for rapider approval of innovative ingredients compared to other regions, fostering new product development. Regulatory alters in the UK have enabled more precise labelling for nutritional benefits in plant-based drinks earlier than in other jurisdictions. Oat milk has become a widely adopted standard choice among coffee shops in London, reflecting a mainstream shift in consumer preferences. This dynamic mix of consumer demanregulatory agilitytyy,y and café culture sustains the UK’s influential market position.

SwedePlant-Baseded Beverages Market Analysis

Sweden is another major countest in the European plant-based beverages market due to its policy-led dietary guidance and emphasis on local sustainable ingredients. A significant portion of hoapplyholds frequently purchase oat-based dairy alternatives, with per capita consumption displaying an upward trconclude. Official dietary guidelines recognise fortified oat and pea beverages as appropriate dairy substitutes for various age groups, including children. Key manufacturers utilise locally sourced ingredients and renewable energy to power production facilities. Cultivation of oats has increased, which strengthens local supply chains for plant-based drinks. Additionally, Sweden’s high digital literacy enables direct-to-consumer models with subscription boxes from artisanal producers. This integration of public health policy, agricultural strategy,y and eco consumerism positions Sweden as a model for sustainable plant-based beverage development.

FranPlant-Basedsed Beverages Market Analysis

France experienced a steady growth in the European plant-based beverages market owing to institutional adoption and growing urban health consciousness. Policy initiatives tarreceiveing school nutrition have contributed to increased procurement of fortified plant-based milk alternatives in public cafeterias. Data indicate that sales of these beverages have experienced higher growth rates within the food service sector compared to retail channels. Urban populations are displaying a preference for higher-conclude, functional plant-based drink options. Younger, urban demographic groups demonstrate a notable pattern of regular consumption of plant-based beverages. The National Institute for Agricultural Research has partnered with startups to develop pea and fava bean beverages aligned with France’s protein sovereignty goals. This dual track of public sector scaling and health-driven retail innovation positions France as a unique bridge between policy and personal wellness.

Netherlands Plant-Based Beverages Market Analysis

The Netherlands is likely to expand in the European plant-based beverages market from 2026 to 2034 due to its leadership in nutritional science and circular agriculture. National dietary guidance now formally includes fortified soy and oat beverages as appropriate alternatives to dairy products. Retailers are increasing their inventory of these alternatives, with a substantial portion being merchandised alongside traditional dairy products. The countest hosts Alpro’s European R&D centre, which pioneered debittered pea protein and algae fortified formulations now sold across the EU. As per research, a significant share of plant-based drinks sold domestically carry the Beter Leven certification,n ensuring ethical sourcing. Additionally, the Netherlands’ dense urban population and high coffee shop density drive strong trade demand. This fusion of scientific validation, retail excellence,ce and café culture creates the Netherlandshigh-integrityity hub for plant-based beverage innovation.

COMPETITIVE LANDSCAPE

Competition in the European plant-based beverages market is characterised by a three-tiered landscape where global brands compete on scale and innovation, national players leverage local sourcing and trust,t and private labels drive price accessibility. Unlike markets driven by ethical vegans, sm Europe’s competiticentresers on nutritional parity, sensory performance and environmental credibility. Oatly and Alpro lead in chilled premium segments with strong café and retail integration, while Provamel and tinyer organic brands capture health-conscious niches through clean labels and certifications. The entest of supermarket private labels has intensified price pressure in ambient segments, yet chilled functional variants maintain premium positioning. Regulatory clarity around fortification health claims anddeforestation-freee sourcing creates both compliance burdens and differentiation opportunities. Ultimately, success hinges on balancing taste,e nutrition, sustainability and affordability across diverse consumer expectations from Stockholm to Seville, building Europe one of the world’s most sophisticated and demanding plant-based beverage markets.

KEY MARKET PLAYERS

Some of the notable key players in the European plant-based beverages market are

- Danone S.A. (France)

- Nestlé S.A. (Switzerland)

- The Hain Celestial Group, Inc. (U.S.)

- Blue Diamond Growers (U.S.)

- Califia Farms, LLC (U.S.)

- The Coca-Cola Company (U.S.)

- SunOpta Inc. (Canada)

- Oatly AB (Sweden)

- Pacific Foods of Oregon, LLC (U.S.)

- Ripple Foods PBC (U.S.)

- Vitasoy International Holdings Ltd. (Hong Kong)

- Elmhurst Milked Direct LLC (U.S.)

- Campbell Soup Company (U.S.)

- Earth’s Own Food Company Inc. (Canada)

- Sanitarium Health Food Company (Australia)

- Good Karma Foods, Inc. (U.S.)

Top Players in the Market

- Oatly is a Sweden-based pioneer in oat-based beverages with a transformative influence on Europe’s plant-based dairy landscape and global oat milk standards. The company leverages proprietary enzymatic technology to convert oats into a creamy, nutritionally balanced drink that performs well in coffee and cooking. Oatly operates major production facilities in Landskrona, Swedenn and Millville, Germany,rmany sourcing oats from regional farms to ensure a low carbon footprint and supply chain transparency. It also expanded its barista edition distribution to thousands of coffee shops across Europe, including partnerships with Costa Coffee and Starbucks. Oatly has repositioned plant-based milk as a mainstream, global staple through a combination of innovative science, sustainable messaging, and barista-focapplyd culinary appeal.

- Alpro is a UK-headquartered brand owned by Danone and a long-standing leader in Europe’s plant-based beverages market with deep expertise in soy, oat and pea formulations. The company offers a comprehensive portfolio, including unsweetened, fortified, ed and barista variants sold across retail and food service channels in numerous European countries. Alpro operates R&D centres in Ghent, Belgium, and Weesp, the Netherlands, focapplying on protein optimisation, texture stability anallergen-freeee processing. It also partnered with Carrefour and REWE to co-develop private label plant milks with reduced sugar and recyclable packaging aligned with EU sustainability mandates. Alpro maintains its reputation as a hoapplyhold staple by integrating nutritional expertise, strategic retail partnerships, and circular design to normalise plant-based options.

- Provamel is a Belgium-based brand under the Alpro Danone umbrella, specialising in organic andnon-GMOO plant-based beverages with a strong presence in health food and pharmacy channels across Western Europe. Known for its clean label philosophy, the brand applys minimal ingredients and avoids artificial stabilisers or added sugars. Provamel’s products are certified organic by EU standards and carry the EU Ecolabel for sustainable production practices. It also introduced functional oat drinks enriched with live probiotic cultures and vitamin B12 from natural fermentation processes approved under EU novel food rules. Provamel meets the demand for transparent plant-based nutrition by focapplying on organic quality, local ingredients, and digestive wellness.

Top Strategies Used by the Key Market Participants

Key players in the European plant-based beverages market focus on ingredient localisation through European-sourced oats, pea,s and fava ba,n s development of functional and fortified formulations with scientifically validated health cla,ims strategic partnerships with coffee chains and retailers for on trade and private label expansion investment in chilled barista specific variants for culinary performance and adoption of circular packaging solutions aligned with EU sustainability and anti plastic regulations.

MARKET SEGMENTATION

This research report on the European plant-based beverages market has been segmented and sub-segmented based on categories.

By Product Type

- Plant-Based Dairy

- Meat Substitutes

- Other Plant-Based Food Products

By Ingredient

- Soy

- Oat

- Other Plant-Based Ingredients

By Form

- Refrigerated/Chilled

- Frozen

- Other Forms

By Distribution Channel

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe