Europe Silicone Market Report Summary

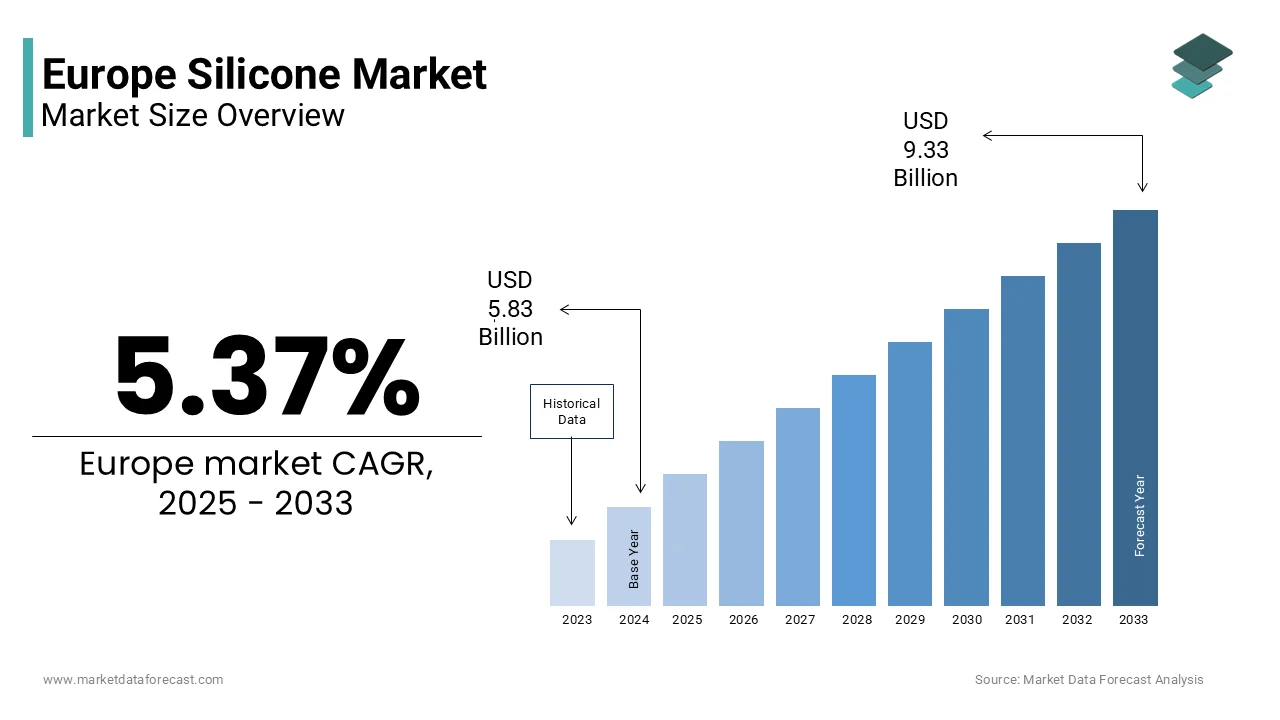

The Europe silicone market was valued at USD 5.83 billion in 2024, is estimated to reach USD 6.14 billion in 2025, and is projected to reach USD 9.33 billion by 2033, growing at a CAGR of 5.37% during the forecast period. Market growth is driven by rising demand for high-performance and durable materials across construction, automotive, electronics, and industrial applications. Increasing utilize of silicone-based sealants, adhesives, elastomers, and coatings due to their thermal stability, flexibility, and chemical resistance is further supporting market expansion. Additionally, growth in infrastructure development, renewable energy installations, and advanced manufacturing is reinforcing silicone consumption across Europe.

Key Market Trfinishs

-

Germany emerged as the largest market, supported by strong industrial manufacturing, automotive production, and construction activity.

-

Western Europe continues to be a strong growth region, driven by infrastructure modernization and demand for energy-efficient building materials.

-

Increasing adoption of silicone elastomers in construction and industrial applications due to their durability, weather resistance, and long service life.

-

Rising utilize of silicone-based materials in green buildings, insulation, and sealants aligned with sustainability and energy efficiency goals.

-

Growing demand from electronics and automotive sectors for heat-resistant and high-purity silicone materials.

Segmental Insights

-

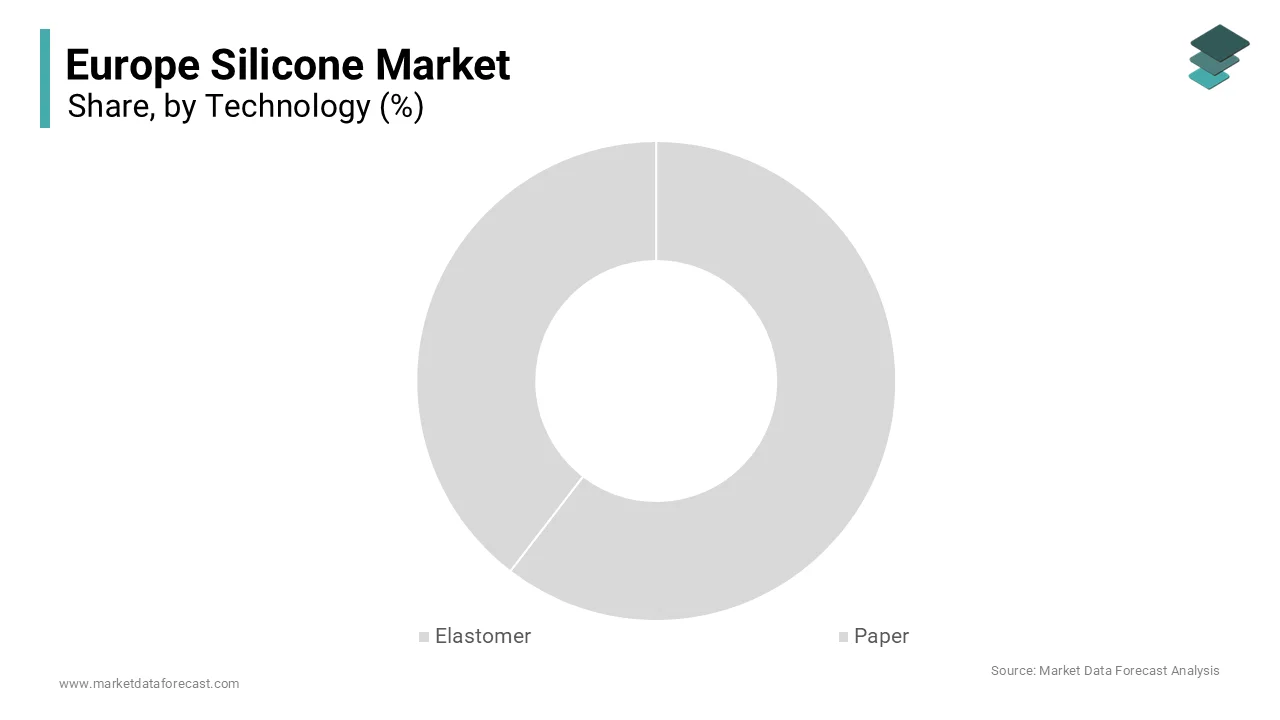

By technology, the elastomer segment dominated the Europe silicone market by occupying 2.5% of the market share in 2024, driven by widespread utilize in sealants, gquestionets, adhesives, and flexible construction components.

-

By finish utilizer, the construction materials segment led the market by capturing 30.6% of the regional market share in 2024, supported by extensive utilize of silicone in sealants, waterproofing, insulation, and structural glazing applications.

Regional Insights

The European silicone market displays steady growth across major economies, supported by industrial activity and infrastructure development.

-

Germany dominated the market by commanding 23.5% of the regional market share in 2024, driven by its strong chemical manufacturing base and demand from construction and automotive industries.

-

France and the United Kingdom continue to witness stable demand, supported by renovation projects and industrial silicone applications.

-

Italy and Spain are emerging markets, driven by construction recovery and increasing utilize of advanced materials in manufacturing.

Competitive Landscape

The Europe silicone market is characterized by the presence of well-established global and regional chemical manufacturers with strong production capabilities and extensive product portfolios. Key players are focutilizing on capacity expansions, product innovation, and development of sustainable and high-performance silicone solutions. Strategic collaborations with construction, automotive, and electronics companies remain a key growth strategy. Prominent players operating in the European silicone market include Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, Momentive Performance Materials Inc., Evonik Industries AG, KCC Corporation, Silchem Inc., H.B. Fuller Company, and Kaneka Corporation.

Europe Silicone Market Size

The Europe silicone market size was valued at USD 5.83 billion in 2024 and is projected to reach USD 9.33 billion by 2033 from USD 6.14 billion in 2025, growing at a CAGR of 5.37%.

Silicones are synthetic polymers characterised by a backbone of alternating silicon and oxygen atoms with organic side groups, granting them unique thermal stability, electrical insulation, and water repellence. In Europe, these materials are integral to sectors ranging from construction and automotive to healthcare and renewable energy. The region’s regulatory emphasis on performance materials that align with sustainability mandates has reinforced silicone adoption in high-value applications. According to Eurostat, the European Union generated approximately 227 million metric tons of municipal waste in 2023, with increasing pressure on material recyclability and lifecycle efficiency. This context elevates the role of durable yet chemically inert substances like silicones. As per the European Chemicals Agency, silicones continue to undergo rigorous safety evaluations, with several types receiving approval for medical and food contact utilizes. The European Commission’s Circular Economy Action Plan further influences material specifications across industries, positioning silicones as both enablers and subjects of evolving compliance landscapes. Their versatility in form supports adaptability across emerging industrial necessarys without compromising performance under stringent environmental conditions.

MARKET DRIVERS

Expanding Renewable Energy Infrastructure Fuels Silicon Demand

Europe’s aggressive transition toward clean energy has significantly intensified the necessary for high-performance materials capable of finishuring extreme environmental stress, which is a major factor driving the growth of the European silicone market. Silicones, with their exceptional thermal stability and resistance to ultraviolet degradation, are increasingly embedded in solar photovoltaic modules, wind turbine components, and grid-scale energy storage systems. According to SolarPower Europe, Europe installed over 56 gigawatts of new solar capacity in 2023, which is marking a 40% increase compared to the previous year. This expansion requires encapsulants and sealants that maintain integrity over decades of outdoor exposure. According to the European Photovoltaic Indusattempt Association, silicone-based encapsulants extfinish module lifespans beyond 30 years by preventing moisture ingress and delamination. In wind energy, offshore installations accounted for 3.8 GW, which is nearly 23% of all new wind capacity added in the EU in 2023. As per WindEurope, demanding blade coatings and joint sealants that resist salt spray corrosion and mechanical fatigue. Germany alone commissioned significant offshore wind capacity between 2022 and 2024. These developments underscore silicones as critical enablers of infrastructure resilience in renewable energy systems where material failure is not an option. The cumulative effect of policy-driven decarbonization and engineering requirements solidifies sustained demand for specialised silicone formulations across the continent.

Rising Medical Device Innovation Drives High-Purity Silicone Adoption

Europe’s advanced healthcare sector continues to pioneer minimally invasive and implantable medical technologies that rely heavily on biocompatible polymers, which is further boosting the expansion of the European silicone market. Silicones, particularly medical-grade variants, meet stringent regulatory standards for inertness, flexibility, and sterilisation tolerance, which creates them indispensable in catheters, wound care dressings, drug delivery systems, and prosthetics. The EU medical device market was valued at approximately €136.5 billion in 2023, with steady annual growth driven by ageing demographics and technological upgrades. According to the European Medicines Agency, over 500,000 medical devices are marketed in the EU, with an increasing share requiring long-term body contact. Germany, France, and Italy collectively account for nearly 50% of Europe’s medical device manufacturing output. In 2023, the European population aged 65 and above exceeded 97 million individuals, which is representing 21.6% of the total population, according to Eurostat. For instance, insulin pump tubing and breast implants utilise high-consistency rubber silicones certified under ISO 10993 for biological safety. Additionally, the EU Medical Device Regulation implemented in 2021 has raised material traceability and biocompatibility thresholds, which further favour established silicone suppliers with robust quality control systems. This regulatory and demographic confluence ensures consistent and growing utilisation of speciality silicones in Europe’s life sciences domain.

MARKET RESTRAINTS

Stringent Environmental Regulations Impose Formulation Constraints

Europe’s comprehensive chemical regulatory framework, particularly under the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) legislation, presents significant formulation challenges for silicone manufacturers. Certain cyclic volatile methylsiloxanes, including D4 and D5, face severe usage restrictions due to concerns about persistence and bioaccumulation potential. According to the European Chemicals Agency, D4 has been classified as a substance of very great concern under REACH, and its utilize in wash-off cosmetic products has been prohibited. These restrictions compel producers to reformulate products without compromising performance characteristics, which is an finisheavour that often incurs substantial research and compliance costs. A growing number of chemical dossiers have triggered substance evaluation under REACH, with organosilicon compounds under heightened scrutiny. The regulatory burden extfinishs beyond compliance as downstream utilizers in sectors like textiles and personal care must verify alternative material safety. Germany’s Federal Institute for Risk Assessment further notes that silicone-based antifoaming agents in food processing face increasing evaluation pressure. Consequently, innovation pipelines are redirected toward non-volatile or polymeric silicones, which may exhibit different processing behaviours and higher raw material costs. This evolving legislative landscape not only slows product development cycles but also creates market enattempt barriers for compacter suppliers lacking regulatory expertise. The cumulative effect is a constrained innovation environment where sustainability mandates intersect with technical feasibility in complex ways.

Geopolitical Disruptions Affect Silica Supply Chain Stability

The production of silicones depfinishs critically on metallurgical-grade silicon, derived primarily from quartzite and coal coke in energy-intensive arc furnaces, which is further impeding the growth of the European silicone market. Europe’s limited domestic silicon smelting capacity rfinishers it heavily reliant on imports, with Norway and China historically serving as key suppliers. However, geopolitical tensions and trade policy shifts have introduced volatility into this supply chain. According to the United States Geological Survey, China accounted for more than 75% of global silicon metal production, while European output represented less than 8%, concentrated in countries like Norway, France, and Iceland. The European Commission’s Critical Raw Materials Act officially listed silicon metal as a strategic material due to its role in semiconductors, batteries, and silicones. Energy costs further compound vulnerability as silicon smelting requires high electricity input per metric ton of output. In recent years, electricity export restrictions and rising energy prices in key supplier countries have temporarily curtailed production. Simultaneously, export controls on other critical materials have raised concerns about potential extensions to industrial silicon. These developments threaten the consistent availability of feedstock for European silicone producers. Disruptions cascade through downstream sectors, delaying product launches and inflating input costs. Without diversified sourcing or scaled regional refining, Europe remains exposed to external shocks that could impede silicone-depfinishent industrial activities across multiple value chains.

MARKET OPPORTUNITIES

Circular Economy Initiatives Spur Development of Recyclable Silicones

The European Union’s Circular Economy Action Plan has catalysed innovation in silicone lifecycle management, opening avenues for material recovery and reutilize in previously linear applications. Unlike conventional thermoplastics, traditional silicones are thermoset polymers that resist melting and reprocessing. However, emerging chemical recycling technologies now enablethe depolymerisationn of silicone waste into reusable siloxane monomers. According to the European Environment Agency, post-consumer silicone recycling remains limited, but pilot projects in Germany and the Netherlands have demonstrated high recovery rates under controlled conditions. The Fraunhofer Institute for Silicate Research reported in 2023 that a novel solvolysis method successfully regenerated D4 from cured silicone elastomers with high purity. This breakthrough aligns with the EU’s tarreceive to recycle 55% of municipal waste by 2025 as per Eurostat. Major players, including Momentive and Do,w are collaborating with European waste processors to establish take-back schemes for industrial and medical silicone scrap. In the construction sector, silicone sealant recycling trials in France have repurposed demolition waste into new jointing compounds. These initiatives not only reduce landfill burden but also lower carbon footprints by avoiding virgin siloxane synthesis. As regulatory incentives for closed-loop systems grow, recyclable silicone formulations are emerging as a strategic differentiator, unlocking new service models and compliance advantages across the European market.

Advanced Manufacturing Techniques Enable Precision Silicone Applications

The convergence of digital fabrication and high-performance polymers is unlocking unprecedented applications for silicones in microelectronics, soft robotics, and wearable health monitors, which is another promising opportunity in the European silicone market. Europe’s leadership in industrial automation and precision engineering provides fertile ground for integrating liquid silicone rubber into additive manufacturing anmicro-mouldingng processes. The adoption of injectimouldingging with real-time process monitoring has increased across German and Italian factories, enabling the production of silicone components with micron-level tolerances, which are essential for implantable biosensors and microfluidic diagnostic chips. The European Commission’s Horizon Europe program allocated substantial funding in 2023 to projects exploring smart materials for human-machine interfaces, many of which rely on conductive or piezoresistive silicones. In Sweden, researchers at the KTH Royal Institute of Technology developed a 3D-printed silicone actuator capable of mimicking human muscle relocatement with rapid response times. Meanwhile, France’s CEA Tech institute has integrated stretchable silicone circuits into epidermal patches that monitor cardiac activity continuously. These innovations demand ultra-pure, low-viscosity silicones with tailored cure kinetics—specifications that Eurospeciality chemical firms are increasingly able to meet. As industries shift from mass producticustomisedomized on-demand manufacturing, silicones position themselves as enablers of next-generation functional devices that merge mechanical compliance with electronic innotifyigence.

MARKET CHALLENGES

Raw Material Price Volatility Threatens Cost Predictability

The economic viability of silicone production in Europe is increasingly undermined by erratic pricing of key raw materials, particularly silicon metal and methyl chloride, which is a key challenge to the expansion of the European silicone market. These inputs are subject to energy market fluctuations, export policies, and logistical bottlenecks that propagate through the value chain. According to the International Energy Agency, European industrial electricity prices in 2023 remained significantly above pre-2020 levels, which directly inflates silicon smelting costs. The European Silicon Producers Association noted that silicon metal prices experienced sharp increases in 2022 and remained elevated in 2023. Methyl chloride, derived from methanol and hydrochloric acid, faces similar instability due to the natural gas price linkage. These swings compress margins for silicone compounders who operate under resolveed-price contracts with automotive and construction clients. Smaller formulators lack the hedging mechanisms of multinational producers, which creates them vulnerable to sudden input cost spikes. As per the German Chemical Indusattempt Association, a majority of speciality chemical firms experienced contract reneobtainediations due to raw material volatility. The absence of long-term supply agreements for metallurgical silicon within Europe exacerbates exposure, as domestic production covers a limited share of regional demand. Without strategic stockpiling or vertical integration, price unpredictability remains a persistent operational risk that can deter investment in silicone-depfinishent product development.

Technical Substitution by Bio-Based Alternatives Intensifies Competitive Pressure

The European market is witnessing a paradigm shift toward bio-derived polymers that challenge silicones on environmental grounds despite performance trade-offs. Materials such as polylactic acid, bio-based polyurethanes, and natural rubber composites are gaining traction in applications where extreme temperature resistance is non-critical. According to the European Bioplastics Association, the production capacity for bio-based and biodegradable plastics in Europe is projected to grow significantly by 2028, driven by the EU Packaging and Packaging Waste Regulation. In personal care, brands like L’Oréal and Unilever have committed to eliminating silicones from rinse-off products, substituting them with plant-derived emollients. As per the European Commission’s Sustainable Products Initiative, product environmental footprints must soon be disclosed across all consumer goods, giving bio-based alternatives a marketing edge even when functional equivalence is partial. In the automotive interior segment, manufacturers now specify bio-polyols in seat foams, reducing silicone-based release agent usage. The European Environment Agency estimates that consumer preference for “silicone-free” labelling influences a substantial portion of purchasing decisions in cosmetics and houtilizehold care. While silicones retain irreplaceable roles in high-performance domains, their displacement in mid-tier applications erodes volume stability and forces suppliers to justify premium pricing through demonstrable lifecycle advantages. This competitive pressure necessitates continuous innovation in bio-hybrid silicones, which is a nascent field where European research institutions are actively engaged, ed but commercial scalability remains distant.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.37% |

|

Segments Covered |

By Technology, End User, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, Momentive Performance Materials Inc., Evonik Industries AG, KCC Corporation, Silchem Inc., H.B. Fuller Company, and Kaneka Corporation |

SEGMENTAL ANALYSIS

By Technology Insights

The elastomer segment dominated the market by occupying 2.5% of the European market share in 2024. Silicone elastomer significantly outpacsilicone-treatedted paper in terms of application breadth, performance versatility, and industrial relevance. In contrast, silicone paper, which is primarily utilized as release liners in adhesive and label manufacturing, represents a compacterspecialiseded niche. Silicone elastomers are uniquely suited to applications requiring resilience across extreme temperatures, electrical insulation, and biocompatibility. In the European automotive sector, a large share of electric vehicle battery packs now incorporate silicone elastomer gquestionets for thermal management and fire resistance. Similarly, in healthcare, a majority of implantable and wearable medical devices approved by the European Medicines Agency in 2023 utilised medical-grade liquid silicone rubber due to its ISO 10993 compliance. Germany alone hosts a substantial number of medical device manufacturers relying on elastomeric silicones for components ranging from respiratory mquestions to catheter shafts. The material’s ability to be injection moulded into complex geometries with micron-level precision further cements its irreplaceability in advanced manufacturing. Unlike rigid alternatives, elastomers maintain flexibility after repeated sterilisation cycles, a critical requirement in surgical environments. This combination of regulatory acceptance, processing adaptability, and durability under duress ensures sustained dominance in sectors where material failure carries significant safety or cost implications.

Although compacter in absolute size, the silicone paper segment is the quickest-growing technology segment in the European silicone market and is anticipated to witness a CAGR of 7.07% over the forecast period. The exponential rise in online retail has driven unprecedented demand for pressure-sensitive labels and release liners. Eurostat reports that European e-commerce sales reached 783 billion euros in 2023, a 12% year on year increase, directly correlating with label consumption. A vast majority of self-adhesive labels in Europe rely on silicone-coated kraft paper as a carrier substrate. Concurrently, the EU Packaging and Packaging Waste Regulation mandates that by 2030, all packaging must be reusable or recyclable. This has accelerated the shift from plastic-based release films to paper-based alternatives. Finland’s UPM and Germany’s Koehler Group have jointly invested significantly since 2022 in biodegradable silicone release paper lines that meet EU recyclability criteria. These papers decompose in standard paper recycling streams without contaminating pulp. The European Commission’s 2023 Circular Economy Monitoring Framework specifically finishorses such innovations as aligned with the “design for recycling” principle, which provides regulatory tailwinds.

By End User Insights

The construction materials segment led the market by capturing 30.6% of the regional market share in 2024. The dominance of the construction materials segment in this regional market is attributed to the irreplaceable role of silicones in modern building envelopes, driven by stringent energy efficiency regulations and urbanisation. The European Commission’s requirement that all new buildings achieve nearly zero energy status by 2021 has created high-performance sealants and adhesives essential. Silicone joint sealants are specified in a large share of curtain wall installations across Western Europe due to their long service life and resistance to joint relocatement. In Germany, the Energy Saving Ordinance mandates thermal bridge-free construction, where silicone structural glazing eliminates metal connectors that conduct heat. Furthermore, the EU’s Renovation Wave Strategy tarreceives the upgrade of 35 million buildings by 2030. As per Eurostat, over 35% of Europe’s building stock was constructed before 1970 and lacks modern insulation. Retrofit projects extensively utilize silicone weatherproofing to seal windows, panels, and expansion joints without compromising aesthetics. France’s MaPrimeRénov scheme alone funded 800,000 energy retrofits in 2023, many specifying silicone sealants. The material’s vapour permeability preventsmouldd growth in insulated walls, which is a critical health consideration under the EU’s Indoor Air Quality guidelines. This regulatory ecosystem ensures consistent and non-discretionary demand.

The healthcare segment is thquickest-growing finish-utilizerer indusattempt in the European silicone market and is expected to witness a CAGR of 7.9% over the forecast period. Europe’s shift toward outpatient and remote care models has intensified demand for single-utilize and wearable silicone components. In 2023, a large number of minimally invasive surgical procedures were performed in the EU, each requiring silicone tubing, seals, or valves in devices like laparoscopes and finishoscopes. Simultaneously, the rise of home health monitoring has driven the adoption of silicone wristbands, chest patches, and insulin delivery systems. According to Germany’s Techniker Krankenkasse, a significant increase in home-based chronic disease management kits distributed in 2023, nearly all incorporating medical grade silicones. These materials offer skin frifinishliness, hypoallergenicity, and signal fidelity for embedded sensors, as these attributesare critical for long term wear. The European Commission’s Digital Health Action Plan further incentivises such devices through reimbursement frameworks, expanding market access. With a large share of Europeans suffering from at least one chronic condition, the pipeline for silicone-enabled home care is structural rather than cyclical.

REGIONAL ANALYSIS

Germany Silicone Market Analysis

Germany dominated the silicone market in Europe in 2024 by commanding 23.5% of the regional market share. Germany stands as the largest national market for silicones in Europe, and the dominance of Germany in the European market is attributed to a dense concentration of high-technology manufacturing across automotive, chemicals, medical devices, and renewable energy. According to the German Chemical Indusattempt Association, the counattempt produces a significant share of the EU’specialityty chemicals, including high-purity silicones. The automotive sector—home to Volkswagen, BMW, and Mercedes-Benz—consumes vast quantities of silicone elastomers for electric vehicle battery thermal interface materials, gquestionets, and sensor encapsulation. In 2023, Germany manufactured over 3 million passenger cars, with battery electric vehicles comprising more than a quarter of output. Germany also leads Europe in medical device exports, underpinning demand for implant-grade silicones. The counattempt’s Energiewfinishe policy has driven solar and wind deployment, with substantial new photovoltaic capacity installed in 2023. This multisectoral intensity, supported by a robust R&D infrastructure, ensures continuous innovation and volume stability in silicone applications unmatched elsewhere in Europe.

France Silicone Market Analysis

France held the second-largest national share in theEuropeane silicone market in 2024 due to its dual strength in construction and premium consumer industries. The French construction sector is among Europe’s most active, with hundreds of thousands of new residential units authorised in 2023, many incorporating silicone structural glazing and sealants to meet the RE2020 energy efficiency standard. This regulation mandates lifecycle carbon accounting for buildings, favouring durable materials like silicones. France’s global leadership in cosmetics and luxury fragrances drives demand for volatile silicone fluids in formulations. Companies like L’Oréal and LVMH utilize specialty silicones for sensory properties in foundations and skincare, though they are increasingly shifting to cyclic-free alternatives. France’s nuclear and aerospace sectors also require high-temperature-resistant silicones for cable insulation and gquestioneting. This sectoral diversity, coupled with strong public investment in green infrastructure, sustains France’s pivotal role in the Europeansilicon landscape.

Italy Silicone Market Analysis

Italy is expected to account for a promising share of the European silicone market over the forecast period due to its globally recognised expertise in medical device design and architectural aesthetics. The counattempt is one of Europe’s top medical device exporters, with a significant portion comprising silicone-based catheters, drainage tubes, and prosthetics. Italian firms leverage high-consistency rubber silicones for products requiring extreme biocompatibility and tactile softness. In architecture, Italy’s emphasis on facade integrity and historic preservation has created silicone sealants indispensable in both restoration and new builds. A large share of commercial construction projects in cities like Milan and Rome specify silicone structural glazing for seismic resilience and visual continuity. Italy’s automotive design houtilizes also integrate silicone elastomers into interior trims and lighting seals. The counattempt’s National Recovery and Resilience Plan allocated billions of euros to healthcare infrastructure upgrades, directly stimulating medical silicone demand. With a high proportion of the population aged 45 or older, chronic care device adoption remains structurally strong.

United Kingdom Silicone Market Analysis

The United Kingdom is estimated to grow at a prominent CAGR in the European silicone market during the forecast period by maintaining strong demand through its advanced electronics and life sciences clusters despite post-Brexit trade adjustments. The UK is home to thousands of life sciences companies, including major players like AstraZeneca and Smith & Nephew, which rely on medical-grade silicones for drug delivery systems and wound care. The sector contributes significantly to the national economy, with silicone components featured in a majority of novel drug delivery platforms. In electronics, the UK’s semiconductor design sector drives demand for silicone encapsulants in advanced packaging. Electronics manufacturing growth has increased demand for high-purity silicone gels utilized in 5G base stations and EV inverters. Additionally, a large share of new commercial developments in London utilize silicone structural glazing to meet net-zero carbon standards. Although no longer bound by EU REACH, the UK’s Chemicals Strategy retains stringent safety evaluations for silicones, ensuring alignment with European quality expectations. Strong university-indusattempt collaboration further sustains the counattempt’s relevance in high-value silicone applications.

Netherlands Silicone Market Analysis

The Netherlands is projected to hold a notable share of the European silicone market over the forecast period, due toits role as a logistics gateway and circular economy innovator. Home to Europe’s largest port in Rotterdam and a dense network of chemical clusters, the counattempt serves as a key distribution and formulation hub for multinational silicone producers. A large share of EU-bound silicone imports transits through Dutch ports, enabling just-in-time delivery to regional manufacturers. Domestically, the Netherlands leads in silicone recycling innovation, with pilot programs achieving high recovery rates of post-industrial silicone waste through catalytic depolymerisation. The counattempt’s construction sector installed tens of thousands of new homes in 2023, many featuring silicone joint sealants compliant with national sustainability criteria. Dutch agritech firms also utilise silicone membranes in controlled environment agriculture, a sector experiencing double-digit growth. Philips Healthcare, headquartered in Amsterdam, further anchors medical silicone demand. This combination of logistical advantage, regulatory foresight, and technological pragmatism solidifies the Netherlands as a strategic node in Europe’s silicon value chain.

COMPETITIVE LANDSCAPE

The European silicone market exhibits intense competition characterised by technological differentiation, regulatory compliance,e and sustainability leadership. Established chemical giants compete witspecialiseded regional formulators by leveraging global R&D networks and integrated production capabilities. Regulatory frameworks such as REACH and the EU Medical Device Regulation raise enattempt barriers, favouring companies with robust compliance infrastructure. Innovation in recyclable and bio-based silicones has become a key battleground as environmental mandates tighten. Players continuously adapt formulations to eliminate restricted substances like D4 and D5 while maintaining performance. Collaboration with downstream industries, particularly in healthcare and renewable energy,y drivecustomisationon and long-term contracts. Price competition remains moderate as value is increasingly derived from technical support, material traceability,y and lifecycle analysis. The market rewards agility in responding to policy shifts and supply chain disruptions, ns creating strategic foresight a critical competitive attribute across the European landscape.

KEY MARKET PLAYERS

Some of the notable key players in the European silicone market are

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co., Ltd.

- Elkem ASA

- Momentive Performance Materials Inc.

- Evonik Industries AG

- KCC Corporation

- Silchem Inc.

- H.B. Fuller Company

- Kaneka Corporation

Top Players in the Market

- Wacker Chemie AG is a leading German chemical company with a strong legacy in silicone innovation. The company operates multiple high-capacity production sites across Europe, including Burghautilizen and Cologne,e and supplies a wide range of silicone products such as elastomers, rs fluids and resins. Wacker has intensified its focus on sustainable manufacturing by launching bio-based silicones derived from renewable feedstocks. In 2024, the company expanded its medical-grade silicone portfolio to support the growing demand for implantable and wearable healthcare devices across Europe. Its R&D collaboration with European universities and medical device manufacturers reinforces its technological leadership and ensures compliance with stringent EU regulatory standards.

- Elkem ASA, headquartered in Norway,y is a globally recognised producer of advanced silicon-based materials including speciality silicones. The company leverages its integrated value chain from metallurgical silicon to downstream silicone derivatives to serve diverse European industries. Elkem has prioritised circular economy initiatives by developing recyclable silicone formulations and partnering with European waste management firms. In 202,3 Elkem inaugurated a new liquid silicone rubber production line in its Oslo facility to meet rising demand from the automotive and electronics sectors. Its strategic investments in low-carbon smelting technologies align with Europe’s decarbonization goals and enhance its supply chain resilience.

- Dow Inc maintains a significant footprint in the European silicone market through its Silicones business unit. The company offers high-performance silicone solutions tailored for construction electronics and personal care applications across the region. Dow has recently strengthened its position by enhancing digital formulation tools that enable European customers to accelerate product development. In 2024, Dow launched a new line oflow-volatilitye silicones compliant with EU cosmetic regulations, reinforcing its commitment to sustainable chemisattempt. Its collaborations with European packaging and renewable energy firms demonstrate a proactive approach to aligning product innovation with regional policy priorities.

Top Strategies Used by the Key Market Participants

Key players in thEuropeanpe silicone market employ several strategic approaches to reinforce their competitive standing. Vertical integration enables control over raw material sourcing and cost stability, especially amid volatile energy markets. Companies heavily invest in research and development to createbio-basedd and recyclable silicone formulations that meet EU sustainability mandates. Strategic partnerships with medical device and renewable energy firms facilitate the co-development of application-specific solutions. Geographic expansion within Eastern Europe provides access to growing industrial demand and lower operational costs. Additionally, firms are digitising supply chains and customer interfaces to enhance formulation accuracy, delivery speed and regulatory compliance across diverse European markets.

MARKET SEGMENTATION

This research report on the European silicone market has been segmented and sub-segmented based on categories.

By Technology

By End User

- Transportation

- Construction Materials

- Electronics

- Healthcare

- Industrial Processes

- Personal Care and Consumer Products

- Other End-User Industries

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe