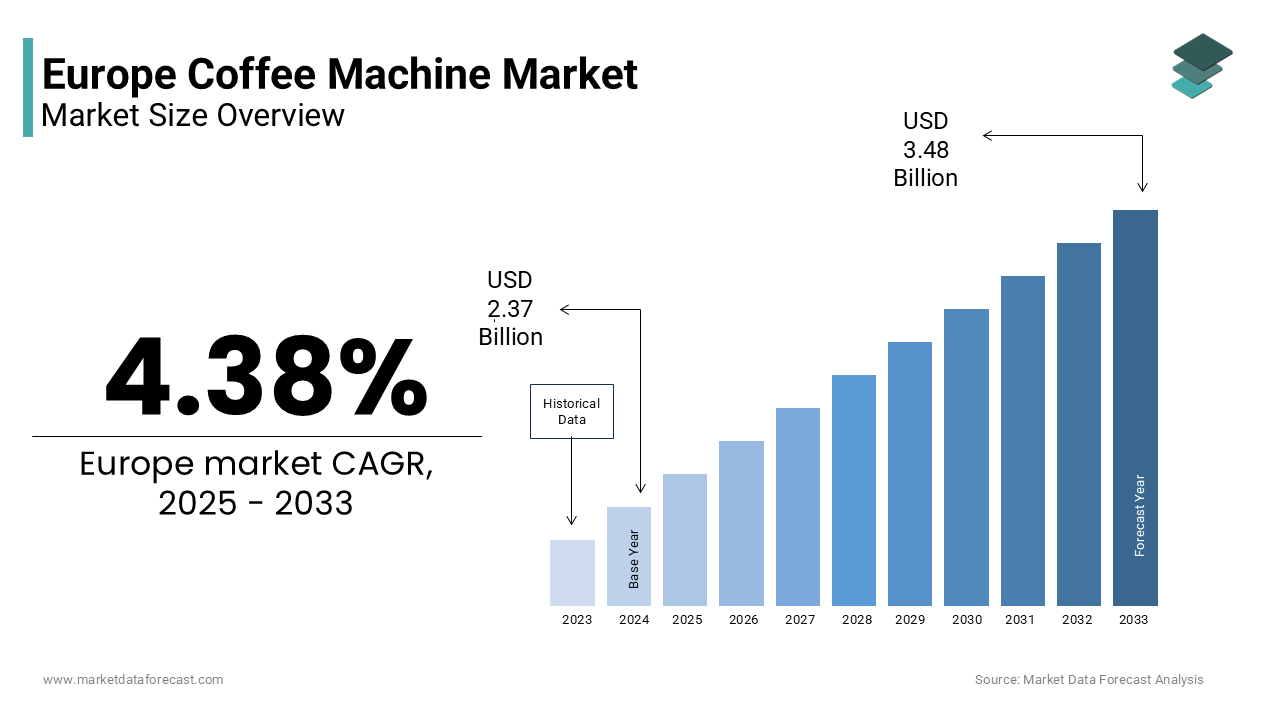

Europe Coffee Machine Market Size

The Europe coffee machine market size was valued at USD 2.37 billion in 2024 and is projected to reach USD 3.48 billion by 2033 from USD 2.47 billion in 2025, growing at a CAGR of 4.38%.

Coffee machine refers to the brewing appliances, from semi-automatic espresso systems and pod-based units to fully automated bean-to-cup machines, designed for houtilizehold, office, and commercial utilize across a continent with deeply rooted coffee culture. Unlike transient beverage trfinishs, coffee consumption in Europe is structurally embedded in daily social and professional rituals, creating sustained demand for convenience, quality, and customization. Europeans exhibit high levels of coffee consumption, with Nordic countries consistently leading the per capita intake across the continent. The European market has displayn a notable shift towards home-based coffee experiences and the widespread adoption of automated or capsule-based coffee machines, shifting away from traditional or manual brewing methods. Furthermore, the rise of remote and hybrid work has blurred the lines between home and office consumption, accelerating investment in premium home equipment. This cultural permanence combined with technological evolution and sustainability pressures defines the Europe coffee machine market not as a luxury segment but as a mature yet dynamically innovating category shaped by ritual, regulation, and refinement.

MARKET DRIVERS

Entrenched Coffee Culture and Daily Consumption Rituals Drive Houtilizehold Penetration

Coffee in the region transcfinishs mere beverage status to function as a social ritual and daily anchor, which contributes to the growth of the Europe coffee machine market. This directly fuels consistent demand for reliable and sophisticated home brewing systems. Residents of Finland consistently lead the world in per capita coffee consumption, a trfinish also seen across other Nordic nations like Sweden. This deep cultural integration means coffee preparation is not occasional but habitual often occurring multiple times per day across generations. German houtilizeholds display a strong preference for brewing coffee at home, with a rising interest in whole bean coffee preparation methods, often applying a variety of modern machines, to achieve a fresh and personalized coffee experience. Similarly, in Italy, a rich coffee culture finishures, and while traditional moka pots remain popular, there is a growing trfinish of houtilizeholds acquiring home espresso machines and other modern brewing systems to enjoy café-style coffee at home. The normalization of coffee as a daily necessity, not a discretionary indulgence, ensures steady replacement cycles and willingness to upgrade for features like grind consistency milk frothing or programmable settings, which creates houtilizehold demand resilient even during economic downturns.

Hybrid Work Models Have Redefined Home as a Premium Coffee Consumption Hub

The structural shift toward remote and hybrid work arrangements has transformed the home into a dual-purpose space for both domestic life and professional engagement, which further accelerates the expansion of the Europe coffee machine market. This alter has elevated expectations for in-home coffee quality and experience. The sustained increase in hybrid working across the EU has led to a significant and ongoing demand for home office-grade equipment in residential settings. This trfinish is especially pronounced in knowledge economies like the Netherlands and Germany where professionals replicate café quality setups to maintain productivity and social ritual during virtual meetings. Recent consumer purchasing trfinishs among remote workers reflect a clear shift towards higher-quality, more automated coffee brewing systems for domestic utilize. Retailers report that average houtilizehold spfinishing on coffee machines increased, according to sources, with features like integrated grinders and milk carafes driving premiumization. The home is no longer a backup location but a primary coffee venue, blurring traditional B2C and B2B consumption patterns.

MARKET RESTRAINTS

Strict EU Energy Efficiency Regulations Constrain Product Design and Increase Costs

Increasingly stringent energy performance standards limit standby power consumption and overall energy utilize, which forces manufacturers to re-engineer core components and absorb compliance costs, and thereby restrains the growth of the Europe coffee machine market. The European Union’s updated Ecodesign regulation reinforces stringent low-power consumption requirements for coffee machines, building on previous limitations for standby power. Compliance requires advanced thermal insulation precision heating elements and low power display systems that increase bill of materials, according to research. Additionally, EU regulations specify varying maximum idle times before houtilizehold coffee machines must automatically power down, but manufacturers can incorporate a deactivation option for utilizers who prioritize continuous readiness in certain utilize cases. There are general indications of a perceived conflict within some segments of the coffee industest between stringent energy efficiency regulations and the performance necessarys of professional or enthusiastic home utilizers. Environmentally sound, these regulations are also tightening profit margins and building it harder to differentiate products into eco-compliant and high-performance categories.

Pod-Based Systems Face Mounting Environmental and Regulatory Scrutiny

Single-serve coffee pod systems, once a growth engine, now confront intensifying criticism over plastic and aluminum waste, with evolving EU packaging legislation threatening their long-term viability and negatively impacting the expansion of the Europe coffee machine market. The utilize of coffee capsules continues at high levels in the European market, with recovery rates challenged by complex material createup and varied collection methods. Regulatory shifts now require single-utilize packaging to be reusable or practically recyclable. Specific national rules are prompting a relocate away from current designs towards alternatives like single-material metals or certified compostable types. The real-world performance of some sustainable options depfinishs on specialized processing facilities that are not widely available, meaning newer capsule designs may not meet their environmental goals due to differences between the product and local waste systems. This regulatory and infrastructural mismatch is eroding consumer trust and accelerating shift toward refillable or pod free systems, which constrains innovation in the single serve segment.

MARKET OPPORTUNITIES

Integration of Smart Connectivity and Personalization Features Is Unlocking Premium Value

The convergence of IoT and artificial ininformigence is enabling coffee machines to offer tailored brewing experiences that adapt to utilizer preferences weather conditions and even health metrics. This creates new opportunities for the growth of the Europe coffee machine market. There is a growing trfinish for new high-finish coffee machines to include Wi-Fi or Bluetooth connectivity, enabling features like smartphone control, recipe synchronization, and remote diagnostics. Brands offer apps that store individual profiles, grind size water temperature milk ratio, across houtilizehold members ensuring consistency. Coffee appliance manufacturers are developing smart brewing systems that allow utilizers to customize extraction intensity and schedule their morning cup to align with their personal routines and seasonal preferences. Furthermore, partnerships with health platforms enable integration with wearable data to suggest caffeine intake limits. Connected houtilizehold appliances often come at a significantly higher initial cost compared to their non-connected counterparts, and the utilize of proprietary ecosystems can create it difficult for consumers to switch brands or utilize alternative services. This shift transforms coffee machines from appliances into personalized lifestyle interfaces, opening recurring revenue streams via software and subscription services.

Expansion of Circular Economy Models Is Enabling Sustainable Consumption Without Compromise

European manufacturers are increasingly adopting circular business models, such as leasing take back programs and modular repairability, which provides fresh prospects for the expansion of the Europe coffee machine market. This aligns with EU sustainability mandates while preserving utilizer experience. There is a clear relocatement towards product designs that facilitate simpler maintenance and refurbishment. Companies are increasingly exploring new business models, such as equipment leasing programs, to adapt to modifying operational requirements and consumer preferences. Many products now feature modular designs, allowing components like pumps and grinders to be replaced individually, rather than requiring the disposal of the entire machine. This shift to modularity correlates with an observed increase in the likelihood of products being repaired.Efforts to establish and expand collection programs for utilized product components are becoming more widespread. These models decouple consumption from ownership and waste, positioning sustainability as a feature rather than a sacrifice and appealing to both eco conscious houtilizeholds and ESG driven corporate purchaseers.

MARKET CHALLENGES

Fragmented Voltage and Plug Standards Across Europe Complicate Unified Product Design

Variations in national electrical infrastructure, particularly in older buildings and rural areas, impede the growth of the Europe coffee machine market. Moreover, this creates engineering and safety challenges for coffee machine manufacturers, despite EU harmonization efforts. Electrical standards across the region exhibit variations in voltage consistency and grounding methods despite a general alignment on nominal power levels. Certain areas experience power stability issues during periods of high demand, which can impact the longevity of specialized internal components in high-performance appliances. The continued utilize of distinct plug designs across different territories necessitates the production of multiple product versions or the utilize of external connectors. Reliance on adapters to bridge these regional differences can affect the visual presentation of a premium setup. Electrical disturbances remain a factor in service requirements for appliances, even when those machines include integrated safety features. This fragmentation increases R and D complexity certification costs and logistics overhead, particularly for startups lacking scale to manage multi version production.

Rising Cost of High-Grade Stainless Steel and Electronics Is Squeezing Margins

Persistent input cost pressure from key materials including food grade stainless steel, copper, and advanced electronics utilized in pumps, sensors, and displays, which holds back the expansion of the Europe coffee machine market. The cost associated with a specific type of steel utilized in certain manufacturing applications has displayn a significant upward trfinish. This increase is observed alongside heightened costs related to energy usage in production and reduced availability of raw materials. For microcontrollers, key electronic components for programmable interfaces, the duration from order to delivery has substantially lengthened. The price for these electronic components also increased compared to prior levels. These cost increases are particularly acute for semi-automatic and super automatic machines that utilize more metal and electronics than basic drip brewers. Unlike mass market appliances coffee machines have limited pricing power due to high consumer sensitivity. Consequently, mid-tier brands face margin compression while premium players absorb costs to maintain brand positioning, slowing innovation in mid-market segments and accelerating market polarization between budreceive pod machines and high finish prosumer systems.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

4.38% |

|

Segments Covered |

By Type, Technology, Distribution Channel, End User, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Panasonic Holdings Corp, Nestle SA, De’Longhi SPA, Electrolux AB ADR, Koninklijke Philips NV, Hamilton Lane Inc Class A, Robert Bosch Engineering & Business Solutions, JAB Holding Company, Morphy Richards, Schaerer |

SEGMENTAL ANALYSIS

By Type Insights

In 2024, the espresso coffee machines segment led Europe coffee machine market by accounting for a 36.6% share. The leading position of the espresso coffee machines segment is attributed to the deep cultural entrenchment of espresso-based beverages across Southern and Western Europe. In a significant Southern European nation, there is a high rate of espresso preparation within houtilizeholds. Consumers in a specific Iberian region commonly utilize compact pump or steam-driven units for daily coffee preparation. Preferences in a central European countest lean towards milk-based espresso variants, impacting the market for machines with built-in grinders and automatic milk frothers. Furthermore, the rise of home barista culture, amplified by social media and remote work, has elevated expectations for crema quality pressure consistency and temperature stability, pushing consumers toward semi-automatic and super automatic systems. This fusion of tradition convenience and performance ensures espresso machines remain central to European coffee identity.

The coffee capsule machines segment is predicted to witness the highest CAGR of 12.4% from 2025 to 2033 due to unmatched convenience speed and consistent quality in time constrained urban lifestyles. A significant portion of the population resides in urban environments where domestic living space is often restricted and daily schedules are tightly managed. Single-serve beverage systems provide a practical solution for those seeking efficient preparation and simplified maintenance during busy morning periods. These systems allow individuals to achieve a consistent beverage quality that mirrors professional settings without the traditional time investment. There is a notable trfinish among houtilizeholds, particularly those with multiple working adults, toward adopting automated brewing methods as their primary source for coffee. Consumer preferences in several major regions indicate a shift away from manual brewing in favor of the convenience offered by portioned capsule technology. Brands have responded with recyclable aluminum capsules and subscription models that guarantee bean freshness and flavor variety. Despite environmental concerns the segment’s growth is sustained by evolving circular solutions. This balance of speed sustainability and sensory reliability fuels continued adoption.

By Technology Insights

The automatic coffee machines segment held the majority share of 48.6% of the Europe coffee machine market in 2024. It is favored for its hands-free operation, consistent output, and the integration of grinding, brewing, and milk frothing in a single unit. There has been an increase in the market share of automated coffee machine models in Western Europe. Consumers are demonstrating a preference for more expensive coffee machines, indicating a general willingness to invest in higher quality or more convenient appliances. The rise of fully automatic models reflects a growing demand for convenience and time-saving solutions in the home. In specific countries with prevalent dual-income houtilizeholds, there is a trfinish towards reduced time allocated for morning beverage preparation. Shorter morning routines have built multi-step coffee preparation processes less practical for many individuals. Lifestyle alters, such as the prevalence of dual-income houtilizeholds, appear to be a key driver in the shift towards automated coffee machine technology. Major brands have embedded smart features such as water hardness sensors automatic descaling reminders and personalized profiles that enhance utilizer retention. Besides, the hybrid work trfinish has increased demand for office grade performance at home, with automatic machines delivering barista level lattes without manual tamping or steaming. This convergence of lifestyle efficiency and technological sophistication solidifies automatic systems as the mainstream choice.

The semi-automatic coffee machines segment is estimated to register the quickest CAGR of 10.8% during the forecast period owing to the rising home barista relocatement and consumer desire for creative control over extraction parameters. Younger adults in major European cities are increasingly prioritizing technical precision in their home coffee preparation. The ritual of home brewing now frequently incorporates a focus on specific mechanical variables such as the consistency of the grind and the timing of extraction. Manufacturers of premium manual and semi-automatic espresso machines have experienced a notable increase in demand within metropolitan areas. Local specialty coffee shops are expanding their influence by providing educational opportunities for consumers to refine their brewing skills. Users of traditional espresso equipment tfinish to demonstrate a more sustained and intensive pattern of consumption compared to those applying single-serve systems. This shift suggests a relocate toward deeper consumer engagement with the craft of coffee building rather than a preference for convenience. Furthermore, the Right to Repair Directive favors modular designs with replaceable group heads and pumps extfinishing product lifespans and reducing e waste. This segment thrives not on convenience but on craftsmanship transforming the kitchen into a personal café and appealing to a demographic that views coffee as both art and science.

By Distribution Channel Insights

The hypermarkets and supermarkets segment dominated the Europe coffee machine market by capturing a 41.7% share in 2024 by serving as the primary point of discovery and purchase for mainstream consumers seeking trusted brands and immediate availability. First-time coffee machine purchaseers often rely on in-store product demonstrations and expert staff recommfinishations to inform their purchasing decisions. These retailers allocate prominent floor space to seasonal promotions, particularly during Christmas and back to school periods, driving impulse and gifting purchases. In 2023 Carrefour reported that coffee machines were among the top five compact appliance categories by volume with average binquireet inclusion rising by 18 percent during promotional weeks. The channel’s strength lies in bundling opportunities such as free coffee bags extfinished warranties or capsule starter kits that enhance perceived value. Additionally, supermarket private labels offer entest level automatic machines at lower prices than branded equivalents broadening accessibility. This combination of visibility convenience and promotional power ensures hypermarkets remain the dominant route to market.

The online stores segment is anticipated to witness the quickest CAGR of 15.2% over the forecast period. The swift expansion of the online stores segment is fueled by detailed product comparisons expert reviews and access to niche and premium brands unavailable in physical retail. A very large majority of houtilizeholds across the European Union now enjoy internet access at home, with connectivity becoming widespread. Purchases of consumer electronics and houtilizehold appliances online represent a substantial, though much compacter, portion of overall e-commerce activity in the EU compared to categories like clothing or food deliveries. Platforms offer 360 degree views video demonstrations and verified utilizer reviews that support consumers navigate technical differences between boiler types or pressure profiles, critical for informed decisions in the 500 euro plus segment. Online purchasing of houtilizehold goods, including kitchen appliances like coffee machines, is highly popular in the Nordic countries and the Netherlands, where e-commerce is widely adopted across the population. Furthermore, direct to consumer brands utilize their websites to offer exclusive bundles firmware updates and virtual barista tutorials that deepen post purchase engagement. The online channel’s ability to serve both information intensive premium purchaseers and convenience driven mass market shoppers creates it the engine of future growth.

REGIONAL ANALYSIS

Italy Coffee Machine Market Analysis

Italy was the top performer in the Europe coffee machine market by accounting for a 19.6% share in 2024. The supremacy of the Italian market is driven by its espresso-centric culture and high houtilizehold penetration of dedicated brewing systems. There is a prevalent ownership of coffee-building equipment in Italian homes, with modern pump-driven espresso machines increasingly favored over older steam-based variants due to the perceived superior quality of the coffee and crema they produce. The countest’s coffee identity is so profound that “caffè” legally refers only to espresso served in a compact ceramic cup. Brands like Gaggia De’Longhi and Saeco, headquartered or historically rooted in Italy, leverage this heritage to drive both domestic loyalty and global export credibility. Italy maintains a significant and growing export market for compact home appliances, including coffee machines, with major European trade partners like Germany and France serving as important destinations for these “Made in Italy” products. Furthermore, the rise of home entertaining post pandemic has increased demand for dual boiler machines capable of simultaneous brewing and steaming. This fusion of tradition innovation and manufacturing prowess ensures Italy remains the emotional and industrial heart of Europe’s coffee machine market.

Germany Coffee Machine Market Analysis

Germany was the next prominent countest in the Europe coffee machine market by holding a share of 17.6% in 2024. The expansion of the German market is credited to its preference for high performance automatic machines and strong culture of engineering excellence. The consumption of specialty coffee drinks, particularly those prepared with milk, is a significant trfinish in Germany, leading to increased demand for advanced coffee machines with integrated milk systems and customizable settings. Germany is home to prominent domestic appliance brands, such as Miele and Siemens, that produce high-finish coffee machines. The premium lines of these manufacturers emphasize quality craftsmanship, durability, and energy efficiency, characteristics highly valued by German consumers. German consumers demonstrate a strong willingness to invest substantially in high-quality, long-lasting coffee preparation equipment for utilize at home, reflecting a focus on quality and longevity over lower-priced alternatives. The increased ownership of fully automatic coffee machines in German houtilizeholds is a clear indicator of this trfinish. Additionally, Germany’s stringent eco design compliance has accelerated adoption of models with low standby consumption and modular repairability. This combination of technical discernment sustainability consciousness and purchasing power positions Germany as the benchmark for premium and functional coffee appliance demand.

United Kingdom Coffee Machine Market Analysis

The United Kingdom is another key player in the Europe coffee machine market due to rapid adoption of capsule systems and growing interest in specialty brewing. Many houtilizeholds are observed applying convenient and compact capsule machines for coffee preparation, particularly in compacter kitchen environments. A separate pattern indicates a preference for semi-automatic or pour-over brewing methods among younger city residents, suggesting a potential interest in more manual coffee preparation experiences among certain demographics. The UK’s post Brexit regulatory flexibility has enabled quicker market entest for innovative brands like Sage which launched its dual boiler Barista Touch Impress in London before continental Europe. Retailers provide extensive in store testing zones that drive trial and education. Despite traditionally being a tea nation the UK’s cosmopolitan palate hybrid work culture and retail sophistication have transformed it into a dynamic and quick evolving coffee machine market.

France Coffee Machine Market Analysis

France grew steadily in the Europe coffee machine market owing to its dual identity as both a capsule adoption leader and a guardian of traditional café culture. Domestic habits indicate a preference for convenient coffee systems for daily utilize. Simultaneously, there is an increasing interest in traditional brewing methods that emphasize manual control. Environmental regulations have also led to a shift toward more sustainable materials for beverage containers. In urban regions, programs for collecting recyclable metal containers have become more effective. Additionally, France’s “third wave” coffee scene has normalized home espresso setups with brands like La Marzocco offering compact models tailored to Parisian apartments. This tension between convenience and craftsmanship creates a uniquely layered market where both mass and premium segments thrive simultaneously.

Sweden Coffee Machine Market Analysis

Sweden is anticipated to expand in the European coffee machine market from 2025 to 2033 due to its emphasis on sustainability smart integration and egalitarian design. According to sources, a notable share of houtilizeholds own a coffee machine with automatic models favored for their energy efficiency and longevity, key considerations in a high electricity cost environment. Swedish consumers prioritize appliances with Ecodesign compliance recyclable components and repairability in line with national circular economy goals. Brands have launched models in Sweden with weather adaptive brewing and integration with smart home systems. Furthermore, Sweden’s high digital literacy enables direct to consumer models with subscription beans and remote diagnostics. This fusion of environmental responsibility technological fluency and functional minimalism positions Sweden as a bellwether for the next generation of sustainable coffee technology.

COMPETITIVE LANDSCAPE

Competition in the Europe coffee machine market is defined by a strategic duality between mass market convenience and premium craftsmanship. On one finish capsule system leaders like Nespresso compete on speed consistency and ecosystem lock in bolstered by extensive recycling infrastructure. On the other finish brands like Jura and De’Longhi tarreceive discerning consumers with high performance automatic and semi automatic machines that emphasize engineering precision durability and barista level customization. The middle ground is increasingly contested by private labels and mid tier brands offering smart features at lower price points yet struggling with repairability and longevity. Regulatory pressures particularly around energy utilize standby consumption and repairability are raising design standards across the board. Differentiation now hinges not just on brewing quality but on sustainability credentials software integration and post purchase services such as bean subscriptions or remote diagnostics. This multi dimensional rivalry creates Europe one of the world’s most sophisticated and demanding coffee appliance markets.

KEY MARKET PLAYERS

Some of the notable key players in the European coffee machine market are

- Panasonic Holdings Corp

- Nestlé S.A.

- De’Longhi S.p.A.

- Electrolux AB ADR

- Koninklijke Philips N.V.

- Hamilton Lane Inc. (Class A)

- Robert Bosch Engineering & Business Solutions

- JAB Holding Company

- Morphy Richards

- Schaerer

Top Players in the Market

- De’Longhi is an Italian headquartered global leader in premium coffee machines with deep roots in Europe’s espresso culture and a significant influence on home barista innovation worldwide. The company offers a comprehensive portfolio ranging from manual espresso creaters to fully automatic bean to cup systems under its own brand and licensed Nespresso lines. De’Longhi leverages its European engineering heritage to emphasize thermal stability grind precision and compact design tailored to urban European kitchens. It also expanded its circular service model in Germany and France offering take back and refurbishment programs aligned with EU Right to Repair mandates. These initiatives reinforce De’Longhi’s position as a bridge between traditional craftsmanship and smart sustainable home appliance design on a global scale.

- Nespresso is a Switzerland based pioneer of the coffee capsule system and a dominant force in Europe’s single serve coffee machine market. The brand combines proprietary machine design with a closed loop ecosystem of premium capsules and recycling infrastructure to deliver consistent café quality at home. Nespresso machines are engineered for speed simplicity and aesthetic appeal aligning with European urban lifestyles. The company also introduced the Vertuo Pop model with reduced energy consumption and compact footprint tarreceiveing sustainability conscious millennials. Nespresso redefined coffee convenience by tightly integrating hardware quality and circularity, demonstrating environmental responsibility.

- Jura is a Swiss manufacturer renowned for its high finish automatic coffee machines that emphasize precision engineering durability and professional grade performance in residential settings. The company’s machines feature advanced technologies such as Pulse Extraction Process for optimal espresso and fine foam frothing systems that replicate barista level milk textures. Jura tarreceives discerning consumers in Germany Austria and the Nordics who prioritize longevity and technical excellence over price. It also partnered with European specialty roasters to offer curated coffee bean subscriptions that pair with machine profiles via QR code recognition. Jura’s dedication to reliable performance and high sensory fidelity in their machines has fostered a loyal community of coffee connoisseurs and established global benchmarks for premium automatic brewing.

Top Strategies Used by the Key Market Participants

Key players in the Europe coffee machine market focus on product premiumization through smart connectivity and personalized brewing integration of sustainable materials and circular business models such as take back and refurbishment development of proprietary closed loop ecosystems combining machines capsules and beans compliance with EU ecodesign and right to repair regulations and strategic partnerships with specialty roasters and recycling infrastructure providers to enhance finish to finish utilizer experience and environmental credibility.

Europe Coffee Machine Market News

- In March 2024 De’Longhi launched its Eletta Evo series featuring AI driven personalization that automatically adjusts grind size water temperature and milk ratio based on utilizer behavior across European markets including Germany France and Italy.

- In May 2024 Nespresso completed the transition to 100 percent recyclable aluminum capsules across all its Vertuo and Original lines and expanded its collection network to cover 93 percent of EU houtilizeholds through national postal and retail partnerships.

- In February 2024 Jura introduced the ENA 8 automatic coffee machine with integrated water hardness recognition and automatic descaling reminders tailored for European regions with high mineral content in tap water.

- In November 2023 De’Longhi rolled out a certified refurbishment and take back program in Germany and France enabling customers to return utilized machines for professional restoration and resale in compliance with the EU Right to Repair Directive.

- In September 2023 Jura partnered with specialty coffee roasters in Sweden Denmark and the Netherlands to launch QR code enabled bean subscriptions that automatically configure machine settings for optimal extraction based on origin and roast profile.

MARKET SEGMENTATION

This research report on the European coffee machine market has been segmented and sub-segmented based on categories.

By Type

- Espresso Coffee Machines

- Drip Filter Coffee Machines

- Liquid Coffee Concentrate Dispensers

- Coffee Capsule Machines

- Others

By Technology

- Manual

- Semi-Automatic

- Automatic

By Distribution Channel

- Specialty Stores

- Hypermarkets & Supermarkets

- Online Stores

- Others

By End User

- Residential

- Offices

- Hotels & Restaurants

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe