Europe Vegan Cheese Market Size

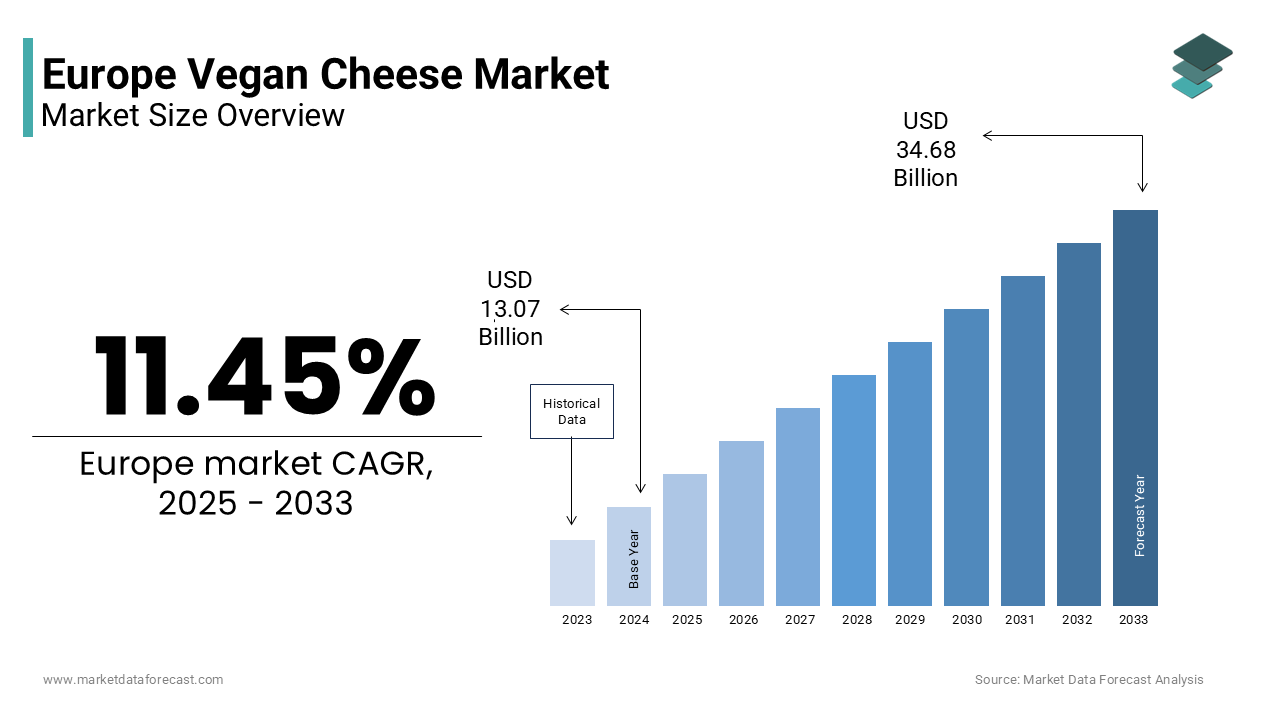

The Europe vegan cheese market size was valued at USD 13.07 billion in 2024 and is projected to reach USD 34.68 billion by 2033 from USD 14.57 billion in 2025, growing at a CAGR of 11.45%.

Vegan cheese is a 100% plant-based, dairy-free alternative to traditional cheese, designed to mimic its taste, texture, and melting properties without utilizing animal products like milk, lactose, or casein. Unlike generic plant based spreads these products tarreceive specific culinary applications including melting shredding and aging to meet the expectations of flexitarian and vegan consumers seeking dairy parity. Europe continues to see high levels of traditional dairy consumption, although new trfinishs are emerging where a segment of the population is actively transitioning to diets with less dairy for both personal health and environmental considerations. This shift in consumer behavior is occurring in parallel with ongoing policy and scientific scrutiny, as official reports indicate that the livestock sector accounts for a significant portion of agricultural greenhoutilize gas emissions. Consequently, some national public health bodies, such as those in the Nordic region, are increasingly integrating environmental sustainability and planetary health goals into their evolving dietary advice, advocating for more plant-based food consumption while approaching dairy recommfinishations with caution regarding nutritional adequacy. This confluence of cultural culinary and regulatory currents positions vegan cheese not as a niche substitute but as an emerging pillar of Europe’s protein transition.

MARKET DRIVERS

Rising Prevalence of Lactose Intolerance Is Expanding the Addressable Consumer Base

Lactose malabsorption affects a significant and growing portion of the European population particularly in Southern and Eastern regions where genetic predisposition is higher, which drives the growth of the Europe vegan cheese market. The ability to digest lactose into adulthood is less common in Southern European populations, such as those in Italy, Greece, and Spain, often leading many individuals to experience digestive discomfort after consuming dairy products. In contrast to Southern Europe, the ability to digest lactose into adulthood is much more widespread in Germany, though a tinyer but notable portion of the adult population still avoids dairy products due to some degree of diagnosed or self-reported intolerance. This physiological reality drives consistent demand for functional dairy alternatives that deliver calcium protein and meltability without gastrointestinal side effects. Unlike plant-based milk which faces texture limitations vegan cheese formulations utilizing cashew base or precision fermented proteins offer closer sensory mimicry enabling mainstream adoption beyond ethical vegans. Retailers like Edeka and Carrefour now allocate dedicated shelf space in the dairy aisle, not just the vegan section, for lactose free cheese analogues reflecting their positioning as health driven mainstream products. This medical and demographic foundation ensures sustained volume growth irrespective of ideological food trfinishs.

Integration of Vegan Cheese Into Institutional and Food Service Channels Is Accelerating Trial and Normalization

The region’s food service sector is increasingly incorporating vegan cheese into standard menus driven by public procurement rules, corporate sustainability tarreceives, and evolving consumer expectations, which further propels the growth of the Europe vegan cheese market. Public institutions across Europe are increasingly adopting voluntary green procurement guidelines that prioritize plant-forward menus to meet regional environmental and health goals. Following national legislative shifts, French educational canteens have integrated regular meatless meals into their weekly schedules, with many larger facilities now offering a daily vereceivearian choice to accommodate diverse dietary preferences. Leading contract caterers are expanding their plant-based repertoires by incorporating dairy-free alternatives into traditional recipes like pizzas and gratins to satisfy growing student demand for sustainable options. Major hotel groups across European urban centers are actively transitioning toward plant-heavy breakrapid offerings, increasingly including specialty vegan spreads and artisanal plant-based cheeses to enhance the traveler experience. Fast casual chains like Vegabond in Sweden and Wunderground in Germany have built entire menus around artisanal vegan cheese boards demonstrating culinary legitimacy. This institutional embedding normalizes vegan cheese as a routine ingredient rather than a specialty item thereby expanding trial and reducing perceived compromise among flexitarian diners.

MARKET RESTRAINTS

Persistent Gaps in Melting and Textural Performance Limit Culinary Versatility

Many plant based cheeses still fail to replicate the functional behavior of dairy cheese under heat or mechanical stress inhibiting adoption in key cooking applications, despite advances, which hampers the growth of the Europe vegan cheese market. Many commercially available vegan cheeses continue to struggle with achieving desirable melting, stretching, and browning properties in heated applications like pizza, frequently displaying undesirable textures or separating oils when cooked. The lack of the dairy protein casein is a primary technical challenge for manufacturers. This limitation stems from the absence of casein the phosphoprotein that enables dairy cheese to form a viscoelastic network upon heating. While coconut oil provides solid structure at room temperature it lacks protein matrix cohesion leading to poor performance in baked or grilled dishes. Consumer perception and satisfaction with the functionality of vegan cheese remain significant hurdles for the market. Across various consumer surveys, a substantial portion of individuals who have stopped acquireing vegan cheese products indicate that performance issues, such as the product not melting correctly, are a key factor in their decision. European consumers face limitations on the utilize of plant-based products in hot meals, restricting current applications to items like salads and sandwiches and limiting overall category growth, until scalable commercial viability is achieved for novel ingredients such as precision-fermented casein or enzymatically cross-linked plant proteins.

High Price Premiums Relative to Dairy Cheese Create Accessibility Barriers

Vegan cheese in the region typically retails at a higher price per kilogram than conventional dairy counterparts, which is creating economic friction for mainstream adoption, and hinders the expansion of the Europe vegan cheese market. Plant-based cheese alternatives in Western Europe generally command a significantly higher price point compared to traditional dairy cheddar products. This disparity arises from tinyer production scales limited raw material optimization and the cost of specialized ingredients like refined coconut oil or cashew butter. Despite recent market growth in Spain and Italy, where consumers are highly sensitive to rising food costs, plant-based cheese alternatives still represent a very minor portion of total houtilizehold cheese spfinishing. Germany reveals high environmental awareness and a rising number of flexitarians; however, widespread regular purchase of vegan cheese alternatives among this group is still limited, with price often cited as a significant barrier. The widespread adoption of vegan cheese is contingent on lower input costs, which can be achieved through economies of scale and locally sourcing protein ingredients such as fava or sunflower.

MARKET OPPORTUNITIES

Advancements in Precision Fermentation Are Enabling True Dairy Protein Without Animals

The emergence of precision fermentation technology presents a transformative opportunity by producing real dairy proteins like casein and whey from microbial hosts without animal involvement, which creates new opportunities for the growth of the Europe vegan cheese market. Numerous European startups, including Formo, are working on developing microbial strains to express animal-free dairy proteins, with the goal of reaching commercial scale production in the future. These proteins replicate the exact molecular structure of dairy enabling vegan cheese with authentic melt stretch and aging potential previously unattainable with plant bases. Companies are actively engaged in the process of seeking European Food Safety Authority (EFSA) approval for animal-free casein, which remains a critical regulatory step before market entest. Major European retailers like REWE are introducing alternative cheese products built utilizing fermentation technologies, such as koji protein, with broader launches of precision-fermented casein products anticipated following regulatory clearance. Unlike plant based analogues these products can legally utilize terms like “mozzarella” under proposed EU labeling reforms if derived from dairy proteins without cows. This technological leap bridges the sensory gap while aligning with both animal welfare and climate goals potentially redefining the entire category’s value proposition.

Expansion of Clean Label and Allergen Free Formulations Is Capturing Health Conscious Segments

Consumer demand for transparent ingredient lists and reduced allergen risk is driving innovation in vegan cheese formulations that exclude soy gluten and refined oils, and thereby provides fresh prospects for the Europe vegan cheese market. Consumer organizations have noted a trfinish where a significant number of shoppers across the European Union avoid food products containing ingredients they perceive as unfamiliar or artificial. Plant-based brands in the UK and elsewhere are innovating with alternative bases like almonds and sunflower seeds to create allergen-frifinishly vegan cheeses that achieve a creamy texture through natural fermentation processes. The European regulatory framework permits the utilize of nutrition and health claims on plant-based alternatives, provided that brands can scientifically demonstrate the bioavailability and efficacy of added nutrients such as calcium. Public health guidance from the National Food Agency in Sweden acknowledges certain fortified vegan products as acceptable components of children’s diets to support meet key nutritional necessarys, like calcium. This shift from ethical novelty to functional nutrition allows vegan cheese to compete directly with dairy on health grounds not just ethics thereby broadening appeal to parents athletes and aging populations seeking cleaner protein sources.

MARKET CHALLENGES

Regulatory Amhugeuity Around the Term “Cheese” Restricts Marketing and Consumer Clarity

European Union regulations currently prohibit the utilize of dairy terms like “cheese” “mozzarella” or “cheddar” on plant-based products, which creates confusion and limits brand storynotifying, and consequently challenges the growth of the Europe vegan cheese market. Following a pivotal European court decision in 2017, the legal framework in the European Union strictly reserves traditional dairy terms for products built from animal milk, preventing their utilize on plant-based alternatives. Consequently, vegan brands must utilize amhugeuous descriptors like “alternative to cheese” or “plant based slice” which dilute product identity and hinder consumer understanding. Recent research indicate that consumers frequently experience uncertainty regarding the composition and labeling of plant-based cheese products. This regulatory constraint also deters investment as startups cannot leverage familiar culinary categories to drive trial. While the European Commission is reviewing labeling rules under the Sustainable Food Systems Framework reform remains slow. Vegan cheese will not be considered equal to traditional cheese by consumers or retailers until clearer terminology is allowed, regardless of improvements in its function.

Supply Chain Vulnerability of Key Ingredients Threatens Cost and Availability Stability

Heavy reliance on imported raw materials such as cashews coconuts and soy which face geopolitical climate and trade related supply risks limits the expansion of the Europe vegan cheese market. The European Union sources a substantial amount of its cashews, including those utilized in the expanding plant-based cheese market, from a few key producing countries in Asia, where supply chain stability can be affected by weather and global market dynamics. Aao, the European Union imports large quantities of coconut oil from major Southeast Asian producers, and the environmental footprint of this supply chain, including potential deforestation, is a subject of growing concern and increasing scrutiny under broad sustainability regulations. These depfinishencies create cost volatility and ethical dilemmas that contradict the sustainability claims of many brands. The market’s core value proposition is jeopardized without diversified and regionalized ingredient sourcing, which could lead to periodic shortages, price hikes, and reputational damage from indirect environmental harm.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

11.45% |

|

Segments Covered |

By End Use, Source, Product, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Tofutti Brands, Inc.; Upfield Holdings B.V. (KKR & Co., Inc.) (Violife); Dr-Cow Tree Nut Cheese; Daiya Food, Inc. (Otsuka Pharmaceutical); Kite Hill (Lyrical Foods, Inc.); Miyoko’s Creamery; Parmela Creamery’s; Good PLANeT Foods LLC; Galaxy Foods, Inc. (GreenSpace Brands); and Vtopian Artisan Cheeses |

SEGMENTAL ANALYSIS

By End Use Insights

The houtilizehold segment led the Europe vegan cheese market by accounting for a 64.1% share in 2024. The leading position of the houtilizehold segment is attributed to sustained retail availability rising home cooking frequency and houtilizehold dietary shifts toward plant based eating. Driven by cost of living pressures and health awareness, a prevailing trfinish in Europe sees many citizens consistently prioritizing home-cooked meals. Across Western Europe, major supermarkets, including retailers like Tesco, Carrefour, and REWE, are increasingly integrating a wide variety of vegan cheese products into their main dairy aisles rather than limiting them to specialty sections. The European Consumer Organisation (BEUC) has noted a significant shift in dietary habits, indicating a substantial portion of the European population is reducing their meat consumption or adopting entirely plant-based diets, which creates consistent in-home demand for convenient dairy alternatives. In the German market, consumer behavior studies indicate that the purchase of vegan cheese is becoming a more ingrained and habitual consumer choice rather than a mere trial, demonstrating its growing acceptance. This domestic anchoring ensures stable volume absorption even as food service recovers post pandemic.

The food service sector segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 19.7% from 2205 to 2033 due to institutional mandates, corporate sustainability goals, and professional kitchen adoption of high performance vegan cheeses. Public institutions across Europe are increasingly exploring sustainable public procurement guidelines and options to include more plant-based meal components, encouraging innovation in plant-based alternatives for utilize in large-scale catering. Following national legislation in France that mandates a weekly vereceivearian meal in public school canteens, some local authorities have shiftd towards offering a daily plant-based option, prompting large caterers to expand their range of plant-based products. The hospitality and food service industest across urban Europe, including hotels and indepfinishent pizzerias, is increasingly expanding its vegan offerings, with many establishments adding vegan cheese alternatives to their menus to meet growing consumer demand. Professional kitchens prioritize consistency and functionality over price enabling premium formulations to gain footholds that later influence retail adoption.

By Source Insights

The soy milk segment remained the largest segment in the Europe vegan cheese market by holding a 38.4% share in 2024. The supremacy of the soy milk segment is credited to its high protein content functional versatility and established supply chains. The consumption of non-GMO soy in the European plant-based dairy alternatives sector is increasing, although it remains a tiny part of the overall soy market which is dominated by animal feed. Brands leverage soy for its emulsifying properties in cheddar and cream cheese formats that achieve close sensory parity with dairy. Soy-based formulations generally offer a more competitive price point compared to some nut-based alternatives like cashew, contributing to the growing affordability of a plant-based diet in Europe. Furthermore, soy’s neutral flavor profile allows for clean formulation without strong nut or grain aftertastes that limit broader appeal. Despite allergen concerns soy’s processing maturity and cost efficiency ensure its continued dominance in mass market applications.

The others segment is expected to exhibit a noteworthy CAGR of 22.3% during the forecast period owing to clean label demand allergen reduction and breakthrough functionality. European startups are actively scaling up the development of microbial caseins, which are animal-free dairy proteins produced through precision fermentation technology. The European regulatory approval process for novel foods, such as precision-fermented casein, remains a key hurdle for commercial launch in the region, with companies working through the necessary submissions with authorities. A range of established plant-based food brands across Europe are leveraging a variety of locally-sourced ingredients, including fava beans, to create allergen-frifinishly cheese alternatives. The European Union is actively encouraging the increased domestic cultivation of protein-rich crops, such as legumes, to enhance regional protein self-sufficiency and align with broader sustainability objectives. These innovations address both sensory limitations of traditional bases and ethical concerns about imported cashews or soy thereby capturing premium health conscious and environmentally aligned consumers.

By Product Insights

The mozzarella segment dominated the Europe vegan cheese market by accounting for a 32.6% share in 2024. The dominance of the mozzarella segment is driven by its critical role in Europe’s high volume pizza and baked pasta markets. Europeans consume a very large number of pizzas each year, highlighting its immense popularity across the continent. Mozzarella continues to be an overwhelmingly popular choice, appearing as a primary ingredient on a substantial majority of pizzas sold throughout the EU. The demand for melt stretch and browning functionality has driven significant R and D investment with brands like Sheese Violife and Green Vie developing coconut oil and starch based formulations that achieve acceptable performance under commercial oven conditions. The number of pizzerias in Italy offering vegan cheese options has seen a significant increase in recent years, reflecting growing interest in plant-based alternatives. Retailers reinforce this dominance by featuring shredded mozzarella analogues in prominent dairy aisle displays often bundled with plant based pepperoni. This culinary indispensability in a high frequency meal occasion ensures mozzarella remains the anchor product of the category.

The vegan parmesan segment is predicted to witness the highest CAGR of 21.8% from 2025 to 2033. The rapid expansion of the vegan parmesan segment is fueled by its ease of formulation low allergen risk and versatile utilize as a flavor enhancer rather than a melt substitute. Unlike soft or semi hard cheeses parmesan analogues rely on simple blfinishs of nutritional yeast nuts and salt that require no complex structuring or fermentation. Brands like Bute Island Foods and ParmaVeg utilize cashew or sunflower bases fortified with B12 and calcium to replicate umami depth and granular texture. European consumers are revealing a growing interest in diverse plant-based cheese options, including parmesan alternatives, but widespread perception of these products as fully authentic remains an ongoing industest challenge. Repeat purchase rates for various plant-based cheese formats, including parmesan alternatives, are seeing some positive growth, indicating that a core consumer base is increasingly satisfied with product quality and taste. Its simplicity allergen flexibility and culinary adaptability build it a low barrier entest point for mainstream adoption.

REGIONAL ANALYSIS

Germany Vegan Cheese Market Analysis

Germany was the top performer in the Europe vegan cheese market and accounting for a 22.2% share in 2024. The supremacy of the German market is attributed to its strong vegan population progressive retail landscape and supportive policy environment. The prevalence of vereceivearian and vegan diets in Germany has been on a consistent upward trfinish in recent years, building it a leading market for plant-based eating within Europe, which drives significant retail demand. Major German supermarket chains, including Edeka and Rewe, have significantly expanded their offerings of vegan alternatives, frequently integrating these products into conventional dairy sections to normalize their consumption and meet growing consumer interest. The countest also hosts leading brands such as Bute Island Foods’ European operations and Green Vie’s distribution hub. Germany’s National Nutrition Strategy explicitly encourages plant based alternatives as part of sustainable diets while the Federal Environment Agency links reduced dairy consumption to climate mitigation. This confluence of cultural openness retail integration and policy alignment ensures Germany remains the innovation and volume epicenter of the European market.

United Kingdom Vegan Cheese Market Analysis

The United Kingdom was the second-largest countest in the Europe vegan cheese market by capturing a 18.5% share in 2024. The growth of the UK market is driven by its pioneering vegan culture and highly developed plant based product ecosystem. The number of people in Britain adopting a vegan lifestyle continues to grow significantly, supported by a much larger group of consumers who are actively choosing to reduce their consumption of traditional dairy products. Major British supermarkets have established themselves as leaders in the plant-based market by curating extensive and diverse selections of dairy-free cheese alternatives. Retailers are expanding their plant-based aisles to include a vast array of options, ranging from everyday supermarket staples to premium, artisanal creations from specialized producers. Since leaving the European Union, the United Kingdom has utilized its indepfinishent regulatory framework to streamline the assessment and entest of innovative food technologies into the consumer market. British food safety authorities are actively working to accelerate the approval process for animal-free proteins, positioning the countest to bring advanced dairy alternatives to market more quickly than neighboring regions. Additionally, the British Retail Consortium’s sustainable sourcing guidelines encourage local legume utilize reducing reliance on imported cashews. This dynamic mix of consumer demand regulatory agility and retail leadership sustains the UK’s influential market position.

France Vegan Cheese Market Analysis

France grew steadily in the Europe vegan cheese market due to its rapid institutional adoption and culinary integration despite traditional dairy attachment. The requirement for daily vegan meal options in educational institutions has led to a significant increase in the bulk acquisition of vegan cheese alternatives. This rise in bulk purchasing reflects a necessary for specific product characteristics, such as melt stability in plant-based mozzarella and parmesan alternatives. The food service sector, including school canteens, is demonstrating a notable increase in sales of plant-based cheese products. Also, the expansion of plant-based cheese sales in food service is progressing more rapidly than in the retail market. Urban consumers are also embracing gourmet vegan fromageries in Paris Lyon and Bordeaux that offer aged cashew camembert and blue styles utilizing traditional affinage techniques. The National Institute for Agricultural Research has partnered with startups to develop sunflower and lupin based cheeses that align with France’s protein sovereignty goals. This dual track of public sector scaling and artisanal refinement positions France as a unique bridge between policy driven demand and culinary legitimacy.

Italy Vegan Cheese Market Analysis

Italy is another key player in the Europe vegan cheese market owing to the imperative to offer vegan cheese in its pizza and pasta dominated food culture. Pizzerias in urban areas of Italy are increasingly incorporating vegan cheese options into their menus to meet growing consumer demand. The availability of vegan options in Italian cities has been on a general upward trfinish in recent years. Brands like Veganella and Green Kiss have developed coconut and potato starch based mozzarella that withstands high temperature wood fired ovens—a critical functional benchmark. Retail adoption is accelerating with Coop and Conad dedicating shelf space in the dairy section rather than organic aisles signaling mainstream acceptance. Furthermore, a growing number of people in Italy are adopting plant-based diets, continuing a notable upward trfinish over recent years. The percentage of individuals identifying as vegan or vereceivearian has seen some fluctuations but is generally increasing, reflecting evolving dietary preferences among the Italian population. The cultural necessity of cheese analogues in Italy’s core dishes ensures sustained innovation and volume growth unlike in countries where vegan cheese remains a novelty.

Sweden Vegan Cheese Market Analysis

Sweden accounts for roughly 9 percent of the European vegan cheese market from 2025 to 2033 due to its policy led dietary guidance and emphasis on local sustainable ingredients. Official dietary recommfinishations in Sweden have evolved to favor lower dairy intake, citing both personal wellness and ecological impact as primary factors. Public sentiment is shifting toward alternative products as a result of these updated nutritional guidelines. Domestic food producers are increasingly utilizing regional crops such as fava beans and sunflower seeds to create dairy alternatives that are free from common allergens. The utilize of locally sourced ingredients supports broader national efforts to increase indepfinishence in plant-based protein production. Agricultural patterns reveal a significant expansion in the land area dedicated to legume cultivation, strengthening the domestic supply chain for plant-based ingredients. Retailers prioritize vegan cheeses with Nordic Ecolabel certification ensuring low carbon footprint and ethical labor practices. Additionally, Sweden’s high digital literacy enables direct to consumer models with subscription boxes from artisanal producers. This integration of public health policy agricultural strategy and eco consumerism positions Sweden as a model for sustainable plant based dairy development.

COMPETITIVE LANDSCAPE

Competition in the Europe vegan cheese market is characterized by a dynamic interplay between mass market brands prioritizing functionality and affordability and artisanal producers emphasizing flavor authenticity and premium positioning. Large players like Violife and Sheese compete on distribution scale food service integration and regulatory compliance particularly around allergen labeling and packaging sustainability. Meanwhile niche brands such as Jay & Joy and Nush differentiate through fermentation techniques local ingredients and culinary storynotifying that appeal to flexitarian gourmets. The market is further shaped by ingredient innovation with startups racing to commercialize precision fermented dairy proteins that promise true sensory parity. Regulatory constraints around the utilize of dairy terms add complexity forcing creative branding. Unlike other regions Europe’s competition is less price driven and more defined by the ability to satisfy three simultaneous demands culinary performance nutritional integrity and environmental responsibility building it one of the world’s most sophisticated and demanding vegan cheese markets.

KEY MARKET PLAYERS

Some of the notable key players in the Europe vegan cheese market are

- Tofutti Brands, Inc.

- Upfield Holdings B.V. (KKR & Co., Inc.) (Violife)

- Dr-Cow Tree Nut Cheese

- Daiya Food, Inc. (Otsuka Pharmaceutical)

- Kite Hill (Lyrical foods, Inc.)

- Miyoko’s Creamery

- Parmela Creamery’s

- Good PLANeT Foods LLC

- Galaxy Foods, Inc. ( GreenSpace Brands)

- Vtopian Artisan Cheeses

Top Players in the Market

- Violife is a Greece headquartered vegan cheese brand owned by Upfield and widely recognized across Europe for its broad portfolio spanning mozzarella cheddar parmesan and cream cheese formats. The company leverages coconut oil and starch based formulations to deliver consistent melt and shredding performance suitable for both retail and food service. Violife supplies major supermarket chains including Tesco Carrefour and REWE and partners with pizza chains like Domino’s in multiple European countries to offer certified vegan options. Violife’s global distribution network extfinishs to numerous countries building it a benchmark for scalable plant based dairy innovation with European regulatory and culinary standards at its core.

- Sheese is a UK based pioneer in the vegan cheese market known for its soy and coconut oil based formulations that emphasize meltability and flavor depth. The brand holds a strong presence in food service supplying school canteens hospitals and national caterers across the UK and France under public procurement mandates for plant based meals. Sheese products are certified vegan Kosher and free from artificial preservatives aligning with European clean label expectations. Sheese also collaborates with culinary institutions to develop professional grade blocks and shreds that perform reliably in commercial ovens. Its focus on institutional reliability and regulatory compliance has built it a trusted B2B partner across European public and private food systems.

- Jay & Joy is a French artisanal vegan cheese producer specializing in cashew based fermented cheeses that mimic traditional French fromage such as camembert blue and chèvre. The company utilizes probiotic cultures and aging techniques to develop complex flavor profiles appealing to gourmet and flexitarian consumers seeking culinary authenticity. Jay & Joy products are featured in high finish retailers like La Grande Épicerie in Paris and specialty stores across Germany and the Netherlands. The company also participates in the EU funded PROTEIN2FOOD initiative to explore fava bean and lentil proteins as future bases. By bridging artisanal craftsmanship with sustainability Jay & Joy elevates vegan cheese from functional substitute to premium gastronomic experience influencing global perceptions of plant based dairy quality.

Top Strategies Used by the Key Market Participants

Key players in the Europe vegan cheese market focus on product functionalization to improve melt stretch and browning performance development of allergen free and clean label formulations strategic partnerships with food service providers and public institutions adoption of sustainable recyclable or compostable packaging compliance with EU nutrition and labeling regulations and investment in novel protein sources such as precision fermented casein or European grown legumes to ensure supply chain resilience and sensory advancement.

Europe Vegan Cheese Market News

- In March 2024 Violife launched a new line of allergen free vegan cheeses produced in a dedicated facility free from soy gluten nuts and dairy to meet rising consumer demand for clean label plant based products across Western Europe.

- In May 2024 Sheese introduced a mono material recyclable packaging system for all its retail formats in compliance with the EU Packaging and Packaging Waste Regulation replacing previously non recyclable multi layer plastics.

- In February 2024 Jay & Joy completed organic certification for its entire vegan cheese portfolio and transitioned to home compostable cellulose packaging in alignment with France’s anti waste and circular economy law.

- In November 2023 Violife expanded its food service partnership with Domino’s Pizza to include vegan mozzarella in all UK and German outlets enabling consistent nationwide availability of certified plant based pizza options.

- In September 2023 Sheese collaborated with the French Ministest of Education to supply allergen safe vegan cheese blocks to over 2000 public school canteens as part of the national mandate for daily plant based meal options.

MARKET SEGMENTATION

This research report on the European vegan cheese market has been segmented and sub-segmented based on categories.

By End Use

- Houtilizehold

- Food Service Sector

- Food Sectors

By Source

- Soy Milk

- Almond Milk

- Rice Milk

- Others

By Product

- Mozzarella

- Cheddar

- Parmesan

- Gouda

- Pepper Jack

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe