Warren Buffett famously stated, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Hands Corporation Ltd (KRX:143210) does carry debt. But should shareholders be worried about its apply of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things obtain really bad, the lfinishers can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders becaapply lfinishers force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that required capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business applys is to see at its cash and debt toobtainher.

What Is Hands’s Debt?

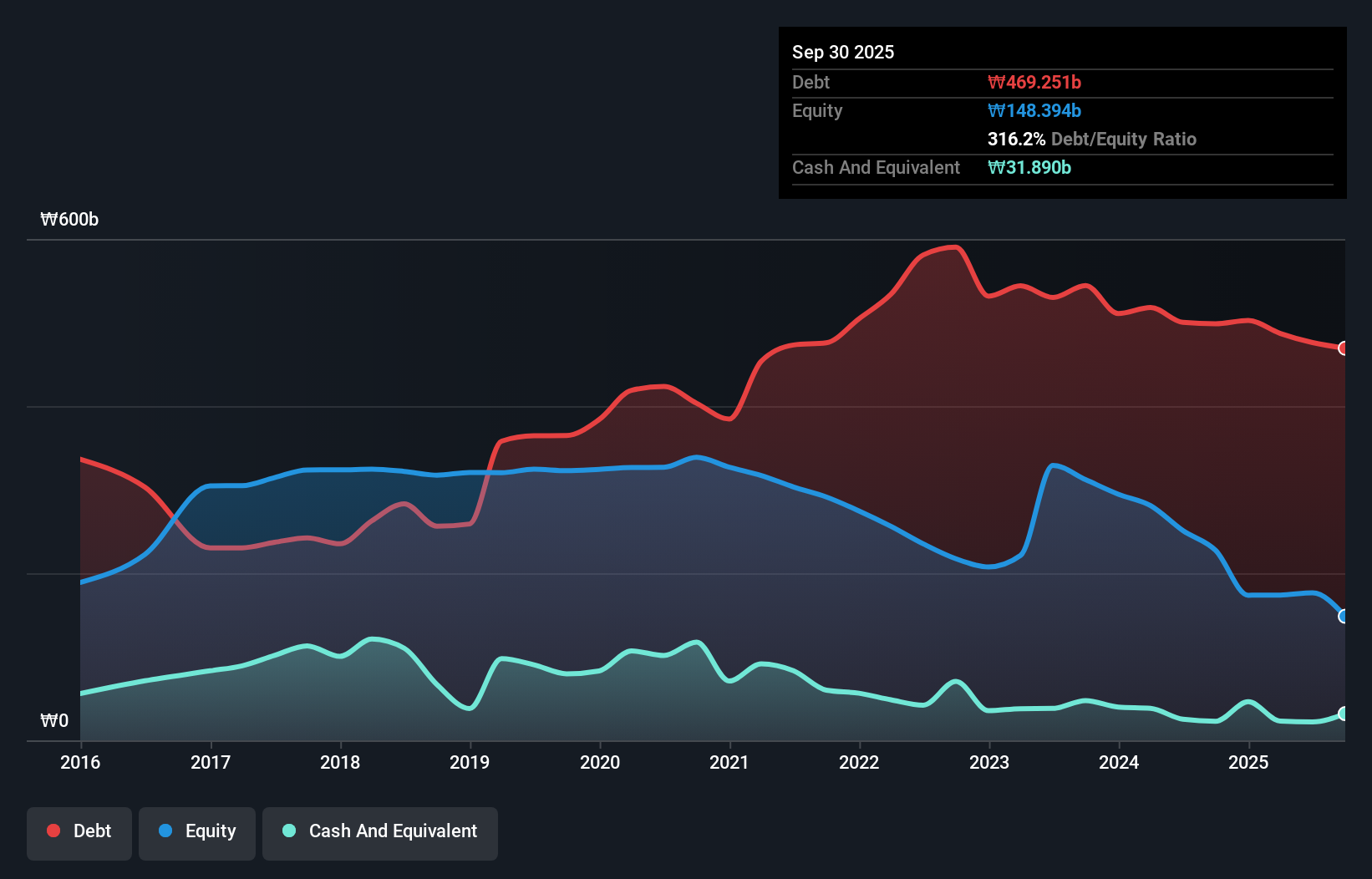

The image below, which you can click on for greater detail, reveals that Hands had debt of ₩469.3b at the finish of September 2025, a reduction from ₩498.5b over a year. However, it does have ₩31.9b in cash offsetting this, leading to net debt of about ₩437.4b.

How Strong Is Hands’ Balance Sheet?

The latest balance sheet data reveals that Hands had liabilities of ₩618.9b due within a year, and liabilities of ₩81.5b falling due after that. On the other hand, it had cash of ₩31.9b and ₩81.8b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩586.7b.

The deficiency here weighs heavily on the ₩25.2b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely believe shareholders required to watch this one closely. After all, Hands would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But you can’t view debt in total isolation; since Hands will required earnings to service that debt. So when considering debt, it’s definitely worth seeing at the earnings trfinish. Click here for an interactive snapshot.

View our latest analysis for Hands

In the last year Hands wasn’t profitable at an EBIT level, but managed to grow its revenue by 11%, to ₩805b. That rate of growth is a bit slow for our taste, but it takes all types to build a world.

Caveat Emptor

Over the last twelve months Hands produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable ₩35b at the EBIT level. Reflecting on this and the significant total liabilities, it’s hard to know what to declare about the stock becaapply of our intense dis-affinity for it. Sure, the company might have a nice story about how they are going on to a brighter future. But the reality is that it is low on liquid assets relative to liabilities, and it lost ₩93b in the last year. So we believe acquireing this stock is risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it. For example Hands has 2 warning signs (and 1 which is potentially serious) we believe you should know about.

Of course, if you’re the type of investor who prefers acquireing stocks without the burden of debt, then don’t hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we’re here to simplify it.

Discover if Hands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividfinishs, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.