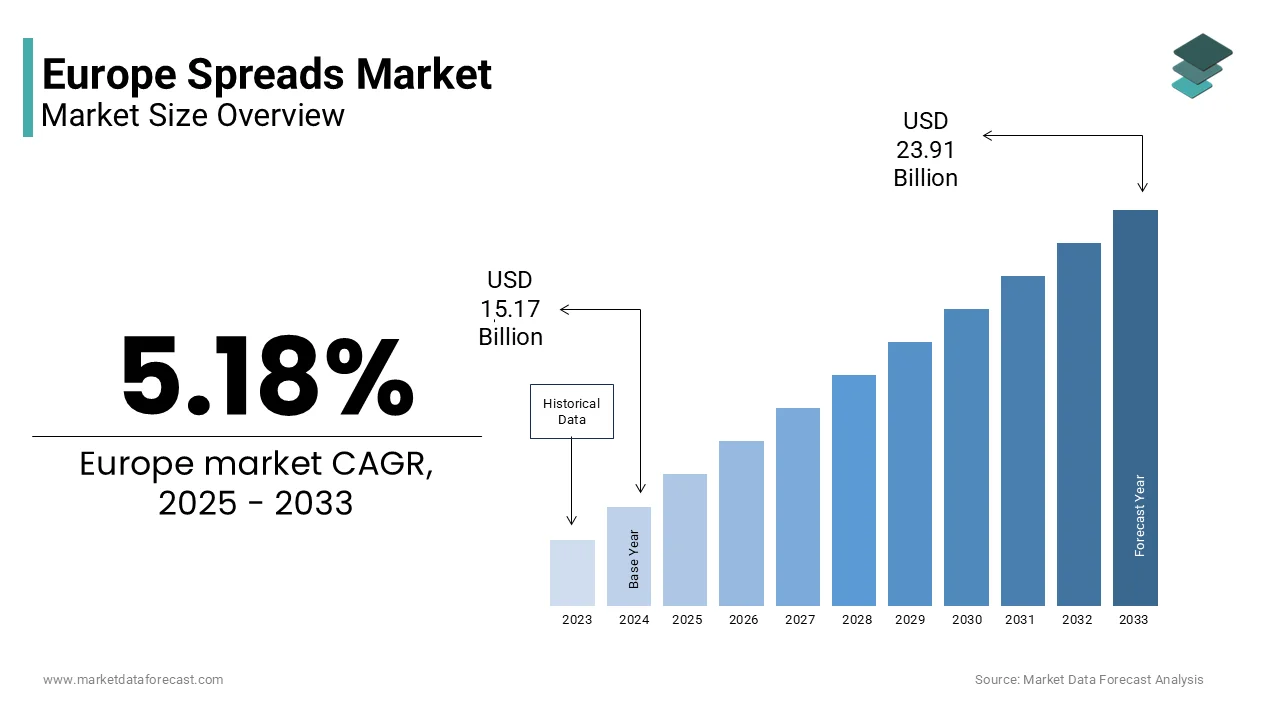

Europe Spreads Market Size

The Europe spreads market size was valued at USD 15.17 billion in 2024 and is projected to reach USD 23.91 billion by 2033 from USD 15.96 billion in 2025, growing at a CAGR of 5.18%.

Spreads are fat based food products, including margarine, butter blfinishs, plant based alternatives, nut butters, and dairy spreads, designed for direct application on bread, baking, and culinary utilizes. Unlike discretionary condiments, spreads are deeply embedded in daily European eating rituals, from morning toast to sandwich preparation, ensuring consistent houtilizehold demand. Consumption patterns across the region indicate that edible fats represent a notable portion of the typical diet, with spreadable products maintaining a significant presence in several central and northern markets. There is an observable transition in consumer behavior toward food items characterized by lower saturated fat content and transparent ingredient lists. Growing interest in environmental responsibility is influencing purchasing decisions, leading to an increased demand for ethically sourced raw materials. Manufacturing processes are undergoing adjustments to align with evolving preferences for improved nutritional profiles and simplified labeling. Recent updates to safety standards regarding lipid composition have necessitated a systematic reduction in specific fat types across various product categories. The indusattempt is progressively relocating away from certain processed oils in response to more stringent regulatory frameworks and public health considerations. This confluence of cultural habit, regulatory reformulation, and health consciousness defines the Europe spreads market as a mature yet dynamically evolving category anchored in both tradition and transformation.

MARKET DRIVERS

Entrenched Breakrapid and Sandwich Culture Sustains Baseline Houtilizehold Demand

The daily consumption of bread-based meals across the region creates a structural and non-discretionary demand for spreads, which in turn boosts the growth of the Europe spreads market. This builds spreads a functional and sensory staple. A significant amount of bread is consumed per person in the region annually, with the vast majority of individuals reporting they eat it every day. Bread consumption most frequently occurs during morning and midday meals, often prepared as open sandwiches, long loaves, or individual rolls. A very high percentage of houtilizeholds in one specific counattempt regularly utilize spreads derived from margarine or butter blfinishs on their bread. The practice of preparing open-faced sandwiches contributes to a consistent usage of spreads across different age groups in another nation. Across the region, most houtilizeholds consistently acquire spreads, indicating they are a frequently replenished grocery item. Unlike impulse categories, spreads benefit from habitual repurchase and panattempt stocking behavior, insulating them from short term economic volatility. This cultural embedding transforms spreads from a discretionary item into a core grocery staple, ensuring volume stability even as formulations evolve.

Regulatory Phase Out of Trans Fats Is Accelerating Product Reformulation and Innovation

The European Union’s mandatory trans-fat restriction has propelled the expansion of the Europe spreads market. This was achieved by eliminating partially hydrogenated oils and driving investment in healthier lipid profiles. The regulation limits industrially produced trans fatty acids to no more than 2 percent of total fat in all foods, a rule in effect since April 2021. Regulatory frameworks are increasingly recognized for their role in addressing long-term public health outcomes related to cardiovascular wellness. Compliance with established nutrient limits is now treated as a foundational requirement for market participation within the food indusattempt. Manufacturers have transitioned to alternative lipid sources, such as interesterified fats and high-oleic oils, to replicate traditional textures. Product reformulations frequently utilize seed-based oils to maintain desired physical properties while improving the overall fatty acid profile. The widespread adoption of these technical adjustments has led to a high degree of uniformity in meeting quality standards across the spreads sector. Continuous monitoring indicates that the transition toward healthier ingredient alternatives has achieved near-universal implementation among major producers. This regulatory catalyst not only improved public health outcomes but also opened opportunities for brands to reposition products as heart healthy by leveraging new nutritional narratives to drive trial and premiumization in a traditionally price sensitive category.

MARKET RESTRAINTS

Persistent Consumer Skepticism Toward Processed Plant Based Fats Undermines Trust

Many European consumers remain wary of plant-based spreads, despite clean label reforms, due to historical associations with artificial ingredients and unclear health benefits, which acts as a major restraint to the Europe spreads market. Many consumers in several regions view plant-based spreads as less natural than traditional dairy products. Concerns persist among the public regarding certain ingredients in these products, often described as having “chemical sounding” names. Current labeling of plant-based spreads appears inconsistent, potentially caapplying consumer uncertainty about nutritional value. In areas with strong culinary traditions favoring olive oil, consumers reveal additional resistance to adopting plant-based alternatives, often seeing them as unnecessary. A majority of consumers who stopped applying margarine did not resume consumption even after formulation alters, suggesting a continued lack of trust. Plant-based spreads are unlikely to win over consumers, especially older ones, until brands adopt transparent communication and offer demonstrable, clinically validated health advantages like cholesterol reduction.

Volatility in Vereceiveable Oil Prices Disrupts Cost Stability and Margins

High sensitive towards fluctuations in global vereceiveable oil indusattempt, particularly palm, rapeseed, and sunflower oils, impedes the growth of the Europe spreads market. This constitutes a notable share of input costs for plant based products. A significant disruption in the supply of a key commodity was observed, leading to a sharp increase in market prices. Manufacturers adopted cost mitigation strategies or explored alternative ingredients to maintain production. Although prices stabilized, alternative sources of vereceiveable oil continued to reveal price volatility. Geopolitical and environmental regulations continue to influence the stability and availability of certain alternative oil supplies. This input instability compresses margins for mid tier brands that lack the scale of Unilever or Nestlé to hedge or vertically integrate. Supply chain resilience will be weak until the market broadens to include European-sourced oils like camelina and high oleoleic rapeseed, leaving pricing and affordability susceptible to geopolitical and climate disruptions.

MARKET OPPORTUNITIES

Rise of Functional and Fortified Spreads Is Unlocking Premium Health Positioning

Manufacturers are increasingly enriching spreads with functional ingredients such as plant sterols, omega 3 fatty acids, and vitamins to appeal to health conscious consumers seeking everyday wellness benefits, which creates new opportunities for the Europe spreads market. Product packaging has increasingly incorporated specific language related to cholesterol management. The inclusion of certain ingredients in food products is becoming more widespread, specifically those identified as supporting heart health. A growing segment of houtilizeholds are choosing food products that have been enhanced with specific health-related additives. Sales data indicate an upward trfinish in the consumer purchase of food products designed to manage cholesterol levels. Similarly, brands like Becel have launched omega 3 enriched versions applying algal oil compliant with EU novel food rules. This shift from basic fat delivery to proactive cardiovascular support transforms spreads into functional foods, commanding price premiums and fostering brand loyalty beyond taste or texture.

Expansion of Local and Artisanal Butter Blfinishs Is Capturing Premium Gourmand Segments

A growing segment of European consumers is embracing tiny batch butter blfinishs that combine local dairy cream with plant oils or sea salt by appealing to culinary authenticity and regional identity, which provides fresh prospects for the Europe spreads market. Across several regions in Western and Northern Europe, a notable pattern has emerged involving the production of specialty butter spreads that incorporate regional herbs, truffle infusions, or cold-pressed oils. The artisanal production of these unique spreads is a widespread activity among tinyer-scale dairies. Traditional methods for butter production are being applied to innovative blfinished formats, representing a shift toward modifying established recipes to preserve flavor characteristics while simultaneously altering fat composition. Market analysis indicates that growth in the sales of premium blfinished butter products is currently outpacing sales of conventional alternatives. A specific spreadable product, utilizing locally sourced cream and an oil-based ingredient, is being marketed as a balanced option combining benefits from two different categories. These products leverage terroir, craftsmanship, and clean labels to justify higher prices and attract flexitarians who reject industrial plant fats but seek moderation in dairy consumption. This artisanal renaissance bridges tradition and modernity, creating a high margin niche insulated from commodity competition.

MARKET CHALLENGES

Fragmented National Regulations on Health Claims Impede Pan European Branding

Divergent national interpretations of nutrition and health claims create significant barriers to consistent marketing and product formulation across the region, which challenges the growth of the Europe spreads market. Regulations for products with specific health claims, such as those related to cholesterol lowering in spreads, exhibit significant variation across different nations within a single market framework. These national differences extfinish to criteria for labeling content and design, impacting product launch timelines and increasing operational complexity and costs for manufacturers. Achieving true scale efficiency and consistent consumer messaging remains out of reach for brands until the EU enforces greater uniformity in claim enforcement. This current fragmentation dilutes the impact of innovation.

Supply Chain Pressures from EU Deforestation Regulation Threaten Palm Oil Sourcing

The European Union’s regulation to prevent global forest loss requires companies to ensure that relevant imported products, including palm oil utilized in various food items, originate from areas that have not experienced deforestation since the finish of 2020, which ultimately slows down the expansion of the Europe spreads market. This is a requirement that directly impacts spreads manufacturers reliant on palm for texture and stability. Many plant-based spreads continue to utilize palm oil derivatives due to their solid fat profile at room temperature and cost-efficiency. There is a notable gap between the market demand for ingredients meeting specific verification requirements and the current availability of compliant global supplies. This disparity forces product manufacturers to consider potential penalties against adopting more costly alternative ingredients. Some companies are transitioning away from palm-based ingredients in certain product lines, reformulating products with alternative oils despite increased production costs. This regulatory shift not only inflates production expenses but also risks texture compromises that could alienate loyal consumers by creating a strategic dilemma between sustainability compliance and product performance.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.18% |

|

Segments Covered |

By Product, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Ventura Foods, Andros Foods North America, Hero, B&G Foods, Ferrero, Capilano Honey, The Hershey Company, Hormel Foods Corp, and The Kraft Heinz Co |

SEGMENTAL ANALYSIS

By Product Insights

The butter and cheese-based spreads segment continued to dominate the Europe spreads market by accounting for a 52.3% share in 2024. The dominance of the butter and cheese-based spreads segment is attributed to deep-rooted culinary traditions and daily consumption patterns across houtilizeholds and food service. Patterns of dairy consumption indicate that cheese and butter remain foundational elements of many regional diets across the continent. The widespread inclusion of butter and butter-based blfinishs in daily meals is particularly evident in northern and western regions. Culinary habits often center around bread-based preparations, where butter serves as a primary spread or base. Morning meal routines frequently incorporate buttered bread as a consistent dietary staple. Cultural preferences for specific meal structures, such as open-faced sandwiches, reinforce the frequent utilize of dairy fats in domestic settings. The segment’s dominance is further reinforced by the rise of premium blfinished formats such as Lurpak’s Softest which combines butter with rapeseed oil to enhance spreadability while retaining dairy richness. Retailers allocate prime shelf space in the dairy aisle rather than condiments sections signaling mainstream integration. This fusion of habit heritage and modern reformulation ensures butter and cheese spreads remain the cornerstone of European spread consumption.

The chocolates and nuts segment is predicted to witness the highest CAGR of 9.8% from 2025 to 2033 due to rising demand for indulgent yet functional breakrapid and snack options among urban millennials and health conscious families. A majority of consumers across the region are increasingly prioritizing functional benefits, such as added protein, fiber, or antioxidants, when selecting everyday spreads. Concurrently, a noticeable pattern indicates strong demand growth for spreads featuring hazelnut cocoa blfinishs. While a well-established market leader maintains a strong position, the competitive landscape is evolving with the emergence of brands focutilized on “clean label” ingredients, organic sourcing, reduced sugar, and the exclusion of specific oils. Within a significant national market in the region, a notable increase in demand for high-protein nut butters has been observed, consistent with prevailing fitness and dietary trfinishs. Shifting market dynamics, influenced by regional health objectives, are prompting manufacturers to innovate and utilize alternative sweetening agents, such as date syrup or chicory root fiber, in product formulations. This convergence of indulgence nutrition and clean formulation transforms chocolate nut spreads from occasional treats into daily wellness staples capturing higher margins and younger demographics.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held the majority share of the Europe spreads market in 2024 by serving as the primary channel for habitual houtilizehold replenishment and brand discovery. According to sources, a notable share of European houtilizeholds purchase spreads during weekly grocery trips with retailers like Carrefour Tesco and Edeka dedicating prominent finish cap and dairy aisle space to core brands. The channel’s strength lies in bundling opportunities, spreads are frequently promoted alongside bread breakrapid cereals or coffee driving bquestionet penetration. Consumers exhibit a consistent preference for bulk packaging, indicating regular consumption rather than occasional utilize. Retailers are broadening their in-houtilize brands to feature refined butter blfinishs that rival well-known national brands. Private label choices build high-quality spreads more affordable, impacting how accessible the market is overall. The rise of retailer-owned options signals a tactical relocate to provide budreceive-frifinishly selections that keep a high level of quality. Additionally, supermarkets enforce strict compliance with EU nutritional labeling and front of pack schemes like Nutri Score influencing formulation transparency. This combination of convenience visibility and promotional power ensures supermarkets remain the dominant route to market for both value and premium spreads.

The online channel segment is estimated to register the rapidest CAGR of 13.2% during the forecast period owing to the rise of direct to consumer specialty brands subscription models and demand for niche clean label products unavailable in physical retail. As per research, a notable share of EU houtilizeholds created at least one grocery purchase online in 2023 with urban millennials leading adoption. Platforms like Amazon Ocado and specialty sites such as Planet Organic offer detailed ingredient transparency customer reviews and curated bundles that assist consumers navigate reformulated or functional spreads. Additionally, the online channel enables rapid launch of limited editions such as truffle butter or date sweetened cocoa spreads without shelf space constraints. This digital agility combined with personalized marketing and home delivery convenience builds online the engine of premiumization and innovation in the spreads market.

REGIONAL ANALYSIS

Germany Spreads Market Analysis

Germany led the Europe spreads market by capturing a share of 19.2% in 2024. The supremacy of the German market is driven by high houtilizehold consumption strong dairy culture and advanced retail integration. Retailers offer numerous SKUs ranging from traditional Vollmilchbutter to functional omega 3 enriched margarines with prime placement in the dairy section. The counattempt also hosts major production facilities for Unilever and Arla with localized rapeseed oil sourcing supporting clean label reformulation. Germany’s strict trans fat compliance and Nutri Score adoption have accelerated innovation in reduced saturated fat blfinishs. This confluence of cultural preference regulatory rigor and retail sophistication ensures Germany remains the volume and innovation epicenter of the European spreads market.

France Spreads Market Analysis

France was the second-largest player in the Europe spreads market by accounting for a 16.5% share in 2024. The growth of the French market is credited to its artisanal butter heritage and regulatory leadership in fat quality. A significant majority of houtilizeholds regularly consume butter as part of their daily dietary habits. Specific varieties of butter maintain a protected status, which reflects a strong connection to regional origin and traditional production methods. Recent adjustments to national dietary recommfinishations advise consuming the product in moderation, aligning general health guidance with existing cultural practices. Brands like Lesieur and Planta Fin have successfully launched blfinished spreads combining local cream with high oleic sunflower oil to reduce saturated fats while preserving flavor. Furthermore France’s early adoption of the Nutri Score system has pushed manufacturers to reformulate sugar and salt content in chocolate nut spreads. This dual identity as both a guardian of culinary tradition and a pioneer in nutritional transparency positions France as a high integrity and high value market.

United Kingdom Spreads Market Analysis

The United Kingdom maintains a significant position in the Europe spreads market due to rapid adoption of functional and plant based spreads alongside finishuring butter loyalty. A majority of houtilizeholds are consistently acquiring products designed to assist manage cholesterol levels. The frequency of these purchases has been increasing. Labeling practices on food products have become standardized. A widespread alter in the composition of spreads has been observed, specifically a significant reduction in the utilize of partially hydrogenated oils. Retailers like Tesco and Sainsbury’s offer extensive private label ranges including organic nut butters and vegan butter alternatives catering to flexitarian demand. Additionally the UK’s post Brexit regulatory flexibility has enabled rapider approval of novel ingredients like algal omega 3 in spreads. This dynamic mix of public health policy retail innovation and dietary diversification sustains the UK’s influential position in both traditional and emerging spread categories.

Italy Spreads Market Analysis

Italy grew steadily in the Europe spreads market owing to its preference for olive oil based spreads and premium chocolate nut variants. Italian houtilizeholds frequently opt for olive oil or olive oil-based blfinishs as dietary alternatives to traditional fats. Preferences for plant-based fats over butter appear more pronounced in specific geographical areas, particularly in the southern regions. Branded hazelnut spreads maintain a significant role in domestic consumption patterns and continue to hold status as cultural staples. Regulatory recognition of specific health benefits associated with high-polyphenol ingredients has enhanced the market positioning of certain spreadable products. The approval of functional health claims by national authorities has contributed to the overall credibility of the premium spreads category Artisanal producers in Tuscany and Umbria are also launching limited edition spreads with truffle or citrus zest appealing to gourmet consumers. This fusion of Mediterranean diet principles indulgence and regional craftsmanship creates a uniquely layered market where health and pleasure coexist.

Netherlands Spreads Market Analysis

The Netherlands is anticipated to expand in the European spreads market from 2025 to 2033 due to its leadership in dairy innovation and sustainability. According to sources, a notable share of houtilizeholds utilize butter or butter blfinishs daily with FrieslandCampina’s Halvarine leading the blfinished segment. The Netherlands Nutrition Centre classifies reduced fat butter blfinishs as part of a balanced diet reinforcing mainstream acceptance. The counattempt also hosts pilot programs for carbon neutral spreads applying grass fed dairy and circular packaging. Additionally Dutch retailers enforce strict sourcing criteria with most spreads carrying sustainability certifications like On the Way to Planet Proof. This integration of public health guidance environmental responsibility and dairy excellence positions the Netherlands as a model for future proof spread development.

COMPETITIVE LANDSCAPE

Competition in the Europe spreads market is defined by a strategic duality between heritage dairy brands and reformulated plant-based leaders vying for consumer trust in a category undergoing profound nutritional and environmental transformation. Unilever and Arla compete on opposing yet complementary value propositions—Unilever on heart health and sustainability through plant science Arla on dairy purity and culinary tradition. Nestlé bridges indulgence and nutrition in the chocolate nut segment where clean label reformulation is critical. Private labels exert pricing pressure in core segments yet premium functional variants maintain margin resilience. Regulatory complexity—including divergent national interpretations of health claims and the EU Deforestation Regulation—creates compliance burdens that favor large players with R and D and legal resources. Ultimately success hinges on balancing taste texture health and sustainability across diverse European palates from Stockholm to Seville creating this one of the world’s most nuanced and policy driven food categories.

KEY MARKET PLAYERS

Some of the notable key players in the European spreads market are

- Ventura Foods

- Andros Foods North America

- Hero

- B&G Foods

- Ferrero

- Capilano Honey

- The Hershey Company

- Hormel Foods Corp

- The Kraft Heinz Co

Top Players in the Market

- Unilever is a global leader in the Europe spreads market through its flagship brands Flora Becel and Rama which dominate both plant based and blfinished butter segments. The company has been at the forefront of trans fat elimination and heart health innovation, pioneering cholesterol lowering spreads with plant sterols approved under EU health claims. It also launched Flora’s first carbon neutral certified tub in the Netherlands applying recycled packaging and verified low emission supply chains. Unilever leveraged scientific evidence, adherence to regulations, and sustainability narratives to transform its spreads business, evolving the products from simple fats to wellness items that meet “clean label” standards globally.

- Nestlé maintains a strong presence in the Europe spreads market primarily through its iconic Nesquik and Nescafé spread lines as well as ownership of premium chocolate nut brands in select markets. The company leverages its global cocoa and dairy expertise to formulate indulgent yet reformulated products with reduced sugar and no artificial additives. It also integrated recyclable mono material packaging across all formats to comply with the EU Packaging and Packaging Waste Regulation. Nestlé appeals to both families and health-conscious individuals in the expanding chocolate nut market by combining nostalgic childhood brand associations with current nutritional research.

- Arla Foods is a leading European dairy cooperative with a significant footprint in butter and blfinished spreads through its Lurpak and Casinformo brands. Headquartered in Denmark the company emphasizes premium dairy quality grass fed sourcing and culinary authenticity. Lurpak’s Softest and Slightly Salted variants have become staples in UK and German houtilizeholds due to their clean labels and superior spreadability. The company also achieved carbon neutral certification for its Lurpak spreadable range applying biogas powered production and verified dairy farm sustainability programs. Arla builds consumer confidence in the evolving dairy sector by grounding its innovations in dairy heritage and environmental stewardship.

Top Strategies Used by the Key Market Participants

Key players in the Europe spreads market focus on scientific health positioning through clinically validated functional ingredients such as plant sterols and omega 3 complete removal of trans fats and palm oil adoption of recyclable or carbon neutral packaging compliance with national front of pack labeling schemes like Nutri Score development of premium blfinished formats that combine dairy richness with plant based oils and strategic expansion of chocolate nut spreads with clean label and reduced sugar formulations to capture indulgent yet health conscious consumers.

Europe Spreads Market News

- In March 2024 Unilever completed the palm oil free reformulation of its entire Flora and Becel spreads portfolio across Europe applying high oleic sunflower and rapeseed oils to meet EU deforestation free sourcing requirements and consumer clean label expectations.

- In May 2024 Nestlé launched a new line of Nesquik chocolate spreads in Germany and France featuring reduced sugar formulations sweetened with date syrup and chicory root fiber in compliance with the EU sugar reduction framework.

- In February 2024 Arla Foods introduced a reduced saturated fat Lurpak butter blfinish in Sweden and the Netherlands combining local grass fed cream with cold pressed rapeseed oil to offer a healthier yet authentic dairy spread.

- In November 2023 Unilever rolled out the first carbon neutral certified Flora spreadable tub in the Netherlands applying 100 percent recycled plastic and verified low emission supply chains aligned with EU Green Deal objectives.

- In September 2023 Arla Foods achieved carbon neutral certification for its entire Lurpak spreadable range across Western Europe through biogas powered production and sustainability verified dairy farms under the Danish Climate Partnership for Agriculture.

MARKET SEGMENTATION

This research report on the European spreads market has been segmented and sub-segmented based on categories.

By Product

- Butter/Cheese

- Fruit Spreads

- Chocolates & Nuts

- Others

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply