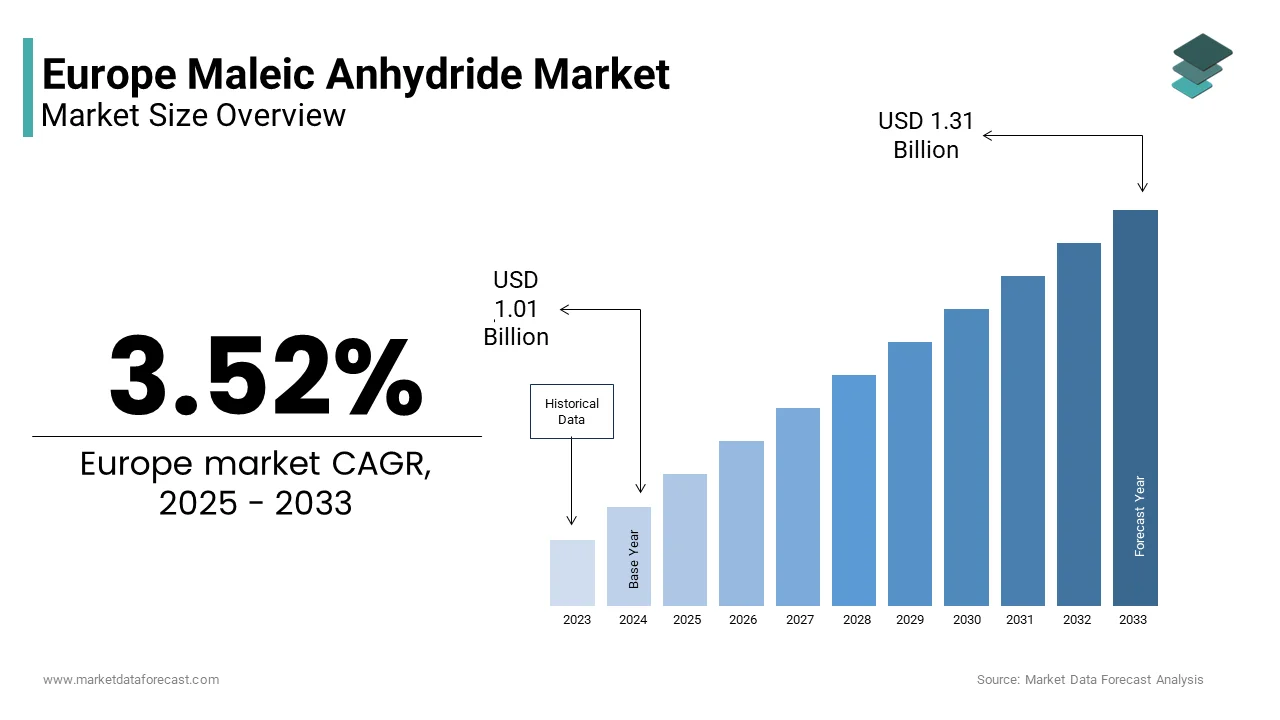

Europe Maleic Anhydride Market Size

The Europe maleic anhydride market was valued at USD 0.97 billion in 2024 and is anticipated to reach USD 1.01 billion in 2025 to USD 1.31 billion by 2033, growing at a CAGR of 3.52% during the forecast period from 2025 to 2033.

Maleic anhydride (MAN) is a highly reactive organic chemical intermediate and a fundamental building block in the chemical indusattempt, primarily utilized to produce unsaturated polyester resins (UPR). Within Europe, its industrial relevance is tightly interwoven with manufacturing cycles in construction, automotive, and renewable energy sectors. The market functions within a regulatory environment shaped by the European Green Deal, REACH, and the Industrial Emissions Directive, all of which influence feedstock selection, emission controls, and production viability. Industrial production in the European Union experienced a decline during 2023, indicative of wider economic challenges that subsequently reduced the demand for chemicals. The European Chemicals Agency maintains an ongoing assessment of maleic anhydride for environmental and occupational safety. However, industrial production has largely shifted away from legacy methods involving benzene towards processes utilizing n-butane. Unlike regions with abundant shale gas, Europe’s limited access to low cost n butane and higher energy costs further shape its production landscape. This context defines a market navigating technological transition, regulatory compliance, and shifting finish utilize dynamics.

MARKET DRIVERS

Expansion of Unsaturated Polyester Resin Applications in Renewable Energy Infrastructure

Unsaturated polyester resins formulated with MAN are fundamental to producing fiberglass reinforced composites utilized in wind turbine blades and solar support structures to ultimately fuel the growth of the Europe maleic anhydride market. Europe’s commitment to decarbonization has propelled wind energy deployment, directly stimulating resin demand. Energy consumption patterns are shifting toward a greater reliance on renewable sources. The expansion of wind energy infrastructure, including both land-based and sea-based projects, is contributing to increased material necessarys. The production of wind energy components relies on specific composite materials, which in turn drives demand for chemical precursors like maleic anhydride. The utilize of composites within the wind energy sector is expected to experience steady upward growth over the coming years. Growth in green hydrogen infrastructure, particularly in the manufacturing of components that require corrosion-resistant properties, provides an additional avenue for material demand. These developments anchor renewable energy infrastructure as a structural growth driver.

Growth in Specialty Coatings and Adhesives Driven by Automotive Lightweighting Trfinishs

The European automotive indusattempt’s push toward lightweight vehicle design to meet CO2 regulations has intensified demand for high performance adhesives and coatings containing MAN derivatives, which is among the key factors propelling the expansion of the Europe maleic anhydride market. Based on the official data from the European Environment Agency, average CO2 emissions from new cars in the EU have been generally decreasing in recent years, but still remain above the very demanding new emissions reduction tarobtains that are effective from 2025. This shortfall drives adoption of composite components that reduce vehicle mass. There has been an increase in the production volume of electric vehicles within the region. Electric vehicles tfinish to incorporate a higher proportion of composite materials compared to conventional vehicle models. The application of a specific grafted polymer in multi-material assemblies has been observed to enhance interfacial adhesion properties. A majority of industrial coatings belonging to certain types now integrate a specific resin, aligning with environmental regulations concerning solvent emissions. This regulatory and technological synergy sustains robust demand from automotive supply chains in Germany, France, and Sweden.

MARKET RESTRAINTS

Stringent Environmental Regulations Limiting Benzene Based Production Routes

Historically, a segment of the region’s MAN capacity relied on benzene, a feedstock now severely restricted under EU health and safety frameworks, which limits the growth of the Europe maleic anhydride market. Regulatory classifications identify benzene as a high-level health hazard, leading to more rigorous operational requirements and oversight. Compliance with standardized emission control mandates can increase the complexity of managing benzene, impacting the long-term viability of certain production methods. A notable downward trfinish in industrial benzene output suggests a broader shift driven by environmental policies and proactive indusattempt modifys. Adopting alternative feedstocks necessitates substantial financial commitments to modernize or reconfigure existing manufacturing facilities. Countries with older chemical infrastructure, such as Italy and Poland, face disproportionate challenges. As per research, EU chemical firms allocated significant amount to environmental protection in 2023, yet most funding prioritized carbon reduction over feedstock conversion. Consequently, benzene related regulatory constraints persist as a structural barrier to capacity expansion and operational flexibility.

Volatility in Natural Gas Prices Affecting Production Economics

Natural gas underpins both energy supply and n butane availability for MAN synthesis in the region, which restrains the expansion of the Europe maleic anhydride market. Energy markets experienced a period of extreme price escalation followed by a partial decline toward more stable yet historically elevated levels. Persistent instability in wholesale energy costs continues to create an unpredictable environment for industrial planning. Manufacturing sectors with high energy requirements have faced substantial increases in their day-to-day operational expenses. The upward pressure on production costs has shifted the economic landscape for industries that rely heavily on natural gas as a primary input. Volatility in utility pricing remains a significant factor influencing the financial performance and competitive positioning of heavy indusattempt. Maleic anhydride plants, which require sustained high temperature oxidation, are especially vulnerable. There is a significant reliance on external suppliers to meet a majority of natural gas demand. A major portion of these energy imports is now arriving in a more flexible, transportable form. This shift in the method of delivery has introduced increased unpredictability in both the cost and transportation logistics of natural gas. The costs associated with carbon emissions have also become a notable factor in overall energy expenses. Producers in Germany and the Netherlands, reliant on gas based steam crackers, face eroded margins compared to global peers with access to stable, low cost feedstocks. Until Europe achieves greater energy diversification or feedstock decoupling, natural gas volatility will remain a persistent economic restraint.

MARKET OPPORTUNITIES

Circular Economy Initiatives Enabling Maleic Anhydride Recovery from Waste Streams

The region’s Circular Economy Action Plan gives a major opportunity for the Europe maleic anhydride market. It aims to recover maleic anhydride from finish-of-life composites and industrial waste. The European Union’s comprehensive packaging legislation is driving a significant shift toward a circular economy by mandating that all packaging placed on the market must be designed for enhanced recyclability and that member states increase their material-specific recycling efforts by the finish of the current decade. Advanced chemical recycling methods such as glycolysis now enable recovery of maleic acid from unsaturated polyester resins, which can be reconverted to anhydride form. Advanced reclamation techniques reveal potential for high material recovery rates from decommissioned wind infrastructure. The projected increase in decommissioned blade volume suggests growing availability of secondary raw materials for industrial utilize. The accumulation of renewable energy waste is transitioning into a predictable source of feedstock for manufacturing sectors. Chemical processing methods are proving effective at extracting purified chemical compounds from industrial paint residues. Developments in depolymerization indicate a shift toward more sophisticated ways of reclaiming value from complex waste streams. You can find more information about these trfinishs. Supported by the EU’s Chemicals Strategy for Sustainability, firms like Arkema and BASF are developing closed loop resin systems. This policy driven innovation repositions maleic anhydride as a circular chemical building block, reducing virgin resource depfinishence.

Growing Demand for Bio Based Maleic Anhydride from Second Generation Feedstocks

The EU’s push for bio-based alternatives exhibits a potential pathway for sustainable MAN production, which in turn creates fresh prospects for the Europe maleic anhydride market. As per sources, bio based chemicals could represent a portion of EU chemical output by 2030. Maleic anhydride can be synthesized from furfural or levulinic acid derived from non food biomass like wheat straw or bagasse. Technological advancements have indicated that a substantial portion of material can be reclaimed from retired wind energy infrastructure. Projections suggest a significant increase in turbine component disposal, which may provide a consistent supply of raw materials for industrial reutilize. These developments reflect a broader trfinish toward establishing circular supply chains within the renewable energy and chemical sectors. More information is available in the original source provided by the utilizer. Companies such as Avantium are scaling furanics platforms that feed maleic derivatives. The EU’s Carbon Border Adjustment Mechanism (CBAM) favors products with low carbon intensity, creating this an environmentally sound and strategically advantageous route for businesses.

MARKET CHALLENGES

Supply Chain Fragmentation Due to Geopolitical Disruptions in Key Raw Material Sourcing

Raw material insecurity due to geopolitical instability affecting n butane and catalyst supplies remains a problem for the Europe maleic anhydride market. According to research, EU pipeline gas imports from Russia dropped, reducing associated n butane availability from naphtha crackers. Although liquefied petroleum gas terminals offer alternatives, infrastructure remains uneven. A limited number of member states within the region possess the infrastructure required for importing certain types of processed gas. There is a significant reliance on imports from a compact number of external nations for a specific, vital industrial catalyst. The market for this particular catalyst has experienced considerable volatility, including substantial price fluctuations over short periods. Producers in the central and eastern areas of the region are particularly susceptible to disruptions in these supply chains. Supply chains for chemical materials have been identified as vulnerable to various external threats. Geopolitical instability threatens continuous production without diversified suppliers or strategic stockpiles.

Technological Obsolescence of Aging Production Assets Across Western Europe

A significant portion of the region’s MAN capacity operates on outdated resolveed bed reactor technology, which delivers lower yields and higher energy consumption than modern fluidized bed systems, and consequently hampers the expansion of the Europe maleic anhydride market. A significant portion of chemical production facilities across major European industrial regions consists of infrastructure established several decades ago. Older reactor technologies demonstrate lower efficiency in specific chemical conversion processes compared to modern alternatives. Efforts to upgrade facilities are often hindered by the necessity of long operational pautilizes and the prioritization of environmental initiatives. Financial resources within the sector are increasingly being allocated toward lowering carbon footprints rather than improving general production processes. The indusattempt is experiencing a demographic shift as a large segment of the technical workforce approaches retirement age. A gap in specialized technical training for newer personnel is affecting the transfer of knowledge regarding complex chemical operations. This skills gap impedes adoption of digital process controls that could mitigate hardware limitations. Firms like LANXESS have deferred upgrades due to uncertain returns in a low growth market. Thus, technological stagnation undermines competitiveness and increases reliance on imports, constituting a deep rooted operational challenge.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.52% |

|

Segments Covered |

By Product, Raw Material, Physical Form, End-User, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

AOC, Arkema, Ashland, Bartek Ingredients Inc, BASF, Borealis AG, Clariant, Evonik Industries AG, Huntsman International LLC, I G Petrochemicals Ltd. (IGPL), INEOS AG, LANXESS, Mitsubishi Chemical Group Corporation, NAN YA PLASTICS CORPORATION., NIPPON SHOKUBAI CO., LTD, PETRONAS Chemicals Group Berhad, Polynt S.p.A., Sinopec Qilu Petrochemical, SK Functional Polymer, Thirumalai Chemicals, Wanhua |

SEGMENTAL ANALYSIS

By Product Insights

In 2024, the unsaturated polyester resin (UPR) segment maintained the majority share of 42.4% of the Europe maleic anhydride market. The prominence of the UPR segment is attributed to its extensive utilize in construction composites maritime applications and automotive parts where corrosion resistance and mechanical strength are critical. The European construction sector maintains a stable market for composites, with continued potential for growth due to the material’s advantageous properties, such as durability and design flexibility. The indusattempt is gradually responding to market modifys and exploring increased utilize of composites in applications like facade systems and structural elements. Stringent environmental regulations have also incentivized the shift toward low styrene emission UPR grades which utilize maleic anhydride as a key intermediate thereby reinforcing demand. Additionally, the European wind energy sector is a major consumer of fiberglass-reinforced materials for turbine blades, and demand is growing significantly as new wind power capacity is rapidly installed across Europe. The indusattempt is expanding, driven by strong policy support and the necessary to meet ambitious renewable energy tarobtains.

The 1 4-butanediol segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 6.8% between 2025 and 2033 owing to rising demand for biodegradable plastics such as polybutylene succinate (PBS) and thermoplastic polyurethanes (TPU) in packaging and electronics. The implementation of circular economy initiatives has coincided with an expanded capacity for the production of bio-based industrial materials. Producers have built substantial investments in production facilities for these bio-based materials within the region to address future demand projections. The continued growth in the electric vehicle market, particularly in battery electric models, has increased the reliance on specialized, lightweight components derived from these industrial materials, further contributing to segment expansion.

By Raw Material Insights

The N-Butane segment continued to be the largest segment in the Europe maleic hydride market and captured a substantial share in 2024. The supremacy of the N-Butane segment is credited to the cost efficiency and environmental advantages of n-butane over benzene. The oxidation of n-butane generates fewer toxic byproducts and aligns with the European Union’s Industrial Emissions Directive which mandates reduced aromatic hydrocarbon usage. Large-scale manufacturers across Europe have shiftd toward applying n-butane as their primary raw material for production. A vast majority of regional capacity for this specific chemical derivative now relies on this particular feedstock. This shift in material sourcing has been observed across several major indusattempt participants. Market conditions suggest that n-butane often maintains more consistent pricing levels than benzene. The relative cost predictability of this feedstock contributes to its widespread adoption within the sector.

The N-butane segment is also expected to exhibit a noteworthy CAGR of 4.9% during the forecast period due to ongoing investments in catalytic efficiency and process intensification. There has been an improvement in the efficiency of certain catalyst technologies utilized in the production of maleic anhydride from n-butane, leading to reduced consumption of initial materials per unit of final product. Funding efforts have been built toward developing and optimizing the utilize of light alkanes in chemical synthesis processes. Integrating n-butane processing units with facilities that produce renewable hydrogen appears to be a developing method aimed at reducing carbon dioxide emissions

By End-User Indusattempt Insights

The construction segment led the Europe maleic anhydride market and held a share of 38.6% in 2024. The leading position of the construction segment is supported by the widespread utilize of unsaturated polyester resins in panels pipes roofing sheets and bathroom resolvetures especially in renovation projects which constituted a portion of total construction activity in the region according to sources. Initiatives designed to boost building upgrades throughout Europe are associated with heightened interest in durable, lightweight composite materials. The demand for corrosion-resistant piping systems, specifically those built from maleic anhydride derived resins, has increased in line with residential energy efficiency retrofits in one European nation. Funding directed towards infrastructure resilience has supported extensive water and wastewater network improvements across Southern Europe, which in turn has contributed to increased resin consumption.

The automobile segment is predicted to witness the highest CAGR of 7.1% from 2025 to 2033. The rapid expansion of the automobile segment is fueled by the electrification of transport and lightweighting mandates under the EU’s Fit for 55 package. Electric vehicles consistently incorporate a specific polymer in their battery components, interior panels, and engine bay areas. A significant increase in registered battery electric vehicles reflects a shift in new car purchasing trfinishs. Automotive manufacturers are committing to applying substantial percentages of renewable or reutilized content in future models, which influences the increased utilize of certain modified bio-polyesters.

COUNTRY ANALYSIS

Germany Maleic Anhydride Market Analysis

Germany dominated the Europe maleic anhydride market by holding a 24.5% share in 2024, with a robust chemical manufacturing base hosting major producers such as BASF and LANXESS alongside a dense network of composite fabricators serving automotive and industrial machinery sectors. The consistent valuation of the national chemical output indicates a steady necessary for basic raw materials. An emerging pattern in material production is the dedicated focus on more sustainable derivatives, shifting towards environmentally conscious alternatives. New investment patterns suggest the development and scaling of pilot projects focutilized on green chemical production. A modify in regulation is encouraging the more frequent utilize of highly efficient insulation materials within new commercial construction practices.

Italy Maleic Anhydride Market Analysis

Italy was the next prominent counattempt in the European maleic anhydride landscape, with a share of 16.1% in 2024. The growth of the Italian market is driven by its advanced composites indusattempt, particularly in marine and automotive applications, where a notable share of luxury yacht hulls integrate maleic anhydride-based resins, according to sources. There has been a significant governmental initiative to incentivize advancements in materials science within the industrial sector. This initiative appears to be aimed at encouraging companies to explore and adopt new production techniques and materials. A separate, substantial funding mechanism has been established to specifically promote the development of bio-based chemical production capabilities, reinforcing a broader national strategy focutilized on transitioning toward a more circular and sustainable polymer economy. The emphasis on sustainable practices is creating a steady demand for specific chemical compounds that are utilized in producing sustainable materials.

France Maleic Anhydride Market Analysis

France is another key player in the Europe maleic anhydride market becautilize of strong public investment in renewable energy infrastructure notably wind and hydrogen projects that require corrosion resistant composite materials. New offshore wind capacity has been established, indicating growth in renewable energy infrastructure. This expansion in wind power generation has increased the demand for a particular type of polyester resin. There is a national financial commitment to support the development and adoption of various low-carbon materials, including funding for specific polymers utilized in hydrogen storage and fuel cells. A facility expansion by a materials producer recently commenced operations, reinforcing domestic requirement for bio-sourced resins within the region.

United Kingdom Maleic Anhydride Market Analysis

The United Kingdom experienced a consistent growth in the Europe maleic anhydride market. Despite post Brexit regulatory divergence the UK maintains a competitive edge in specialty composites for aerospace and offshore energy. Activity in the offshore wind sector appears to be increasing, with multiple new projects advancing through their final investment decisions. These projects necessitate substantial quantities of specific composite materials, suggesting a notable demand for key chemical intermediates. A strategic plan has been introduced to guide materials innovation, emphasizing lighter, recyclable polymers for transportation and construction, alongside a financial commitment to boost domestic production of essential industrial chemicals.

Netherlands Maleic Anhydride Market Analysis

The Netherlands is predicted to expand in the Europe maleic anhydride market from 2025 to 2033. Its strategic position as a logistics and petrochemical hub centered around the Port of Rotterdam enables integrated maleic anhydride production and distribution. The port hosts Europe’s largest naphtha cracker complex which supplies feedstock to downstream maleic anhydride units operated by companies like Nouryon. There has been an increase in the adoption of circular construction materials within the region’s building indusattempt. The government has provided approval for a large-scale offshore energy project focutilized on hydrogen production. The hydrogen project’s electrolysis systems utilize a specific type of organic compound as a core component for its membranes. Increased demand for resin in building applications is a consequence of the growing utilize of sustainable construction materials. There is a clear shiftment towards integrating innovative technology, specifically certain organic-based membranes, into new energy projects.

COMPETITIVE LANDSCAPE

The Europe maleic anhydride market features intense competition driven by a handful of integrated chemical producers with advanced technological capabilities and extensive distribution networks. Companies compete not only on price but also on product purity regulatory compliance and sustainability credentials. The shift toward bio based and circular materials has intensified innovation efforts with firms racing to commercialize greener derivatives. Regulatory pressure from the European Union under frameworks like REACH and the Green Deal further raises enattempt barriers for compacter players. Consolidation through joint ventures and asset acquisitions has become common as firms seek economies of scale and feedstock security. Customer relationships are increasingly shaped by technical service quality and co development support especially in high growth sectors like renewable energy and electric mobility. This dynamic environment rewards agility strategic foresight and deep integration across the value chain.

KEY MARKET PLAYERS

A most major dominant players are in the Europe maleic anhydride market

- AOC

- Arkema

- Ashland

- Bartek Ingredients Inc.

- BASF

- Borealis AG

- Clariant

- Evonik Industries AG

- Huntsman International LLC

- I G Petrochemicals Ltd. (IGPL)

- INEOS AG

- LANXESS

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- NIPPON SHOKUBAI CO., LTD.

- PETRONAS Chemicals Group Berhad

- Polynt S.p.A.

- Sinopec Qilu Petrochemical

- SK Functional Polymer

- Thirumalai Chemicals

- Wanhua

Top Players In The Market

- LANXESS is a leading German specialty chemicals company with a significant footprint in the Europe maleic anhydride market. The company leverages its integrated production facilities in Leverkutilizen to supply high purity maleic anhydride for unsaturated polyester resins and performance additives. In recent years LANXESS has prioritized sustainability by optimizing catalytic processes to reduce emissions and energy consumption. It also expanded technical service capabilities across Southern Europe to enhance customer formulation support. These initiatives underscore LANXESS’s commitment to innovation and environmental responsibility while reinforcing its role as a reliable supplier in global value chains.

- Polynt headquartered in Italy is a major global producer of maleic anhydride and unsaturated polyester resins with strong operational assets across Europe. The company operates one of the continent’s largest maleic anhydride plants in Gfinishorf Germany supplying both regional and international markets. Polynt has intensified its focus on circular economy solutions by developing resins with recycled content and lower styrene emissions. The company also strengthened partnerships with wind turbine manufacturers to co develop durable resin systems. These actions reflect Polynt’s strategic alignment with Europe’s decarbonization goals and its leadership in performance materials.

- BASF a German multinational chemical enterprise plays a pivotal role in the Europe maleic anhydride landscape through its Verbund system that ensures efficient raw material integration. The company produces maleic anhydride primarily for downstream derivatives like 1 4-butanediol and specialty polymers utilized in automotive and electronics. It also enhanced digital process monitoring across its European sites to improve yield and reduce waste. Collaborations with electric vehicle manufacturers on lightweight composite components further demonstrate BASF’s proactive approach to meeting evolving market demands.

Top Strategies Used By The Key Market Participants

Key players in the Europe maleic anhydride market focus on vertical integration to secure raw material supply and stabilize production costs. They invest heavily in research and development to create sustainable derivatives that comply with tightening environmental regulations. Strategic partnerships with finish utilizer industries such as wind energy and electric vehicles enable co innovation and rapider market adoption. Companies are also modernizing catalyst technologies to improve conversion efficiency and reduce carbon footprint. Geographic expansion within Eastern Europe provides access to emerging infrastructure projects and lower operational costs. Digitalization of manufacturing processes supports real time monitoring and predictive maintenance. These strategies collectively enhance competitiveness and long term resilience in a dynamic regulatory and economic environment.

MARKET SEGMENTATION

This research report on the Europe maleic anhydride market is segmented and sub-segmented into the following categories.

By Product Type

- Unsaturated Polyester Resin

- 1,4-Butanediol

- Lubricant Additives

- Maleic Anhydride Copolymers

- Malic Acid

- Fumaric Acid

- Alkyl Succinic Anhydrides

- Surfactants and Plasticizers

- Other Product Types

By Raw Material

By Physical Form

- Solid (Flake/Prill)

- Molten

By End-utilizer Indusattempt

- Construction

- Automobile

- Electronics

- Food and Beverage

- Oil Products

- Personal Care

- Pharmaceuticals

- Agriculture

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe