Europe Fencing Market Size

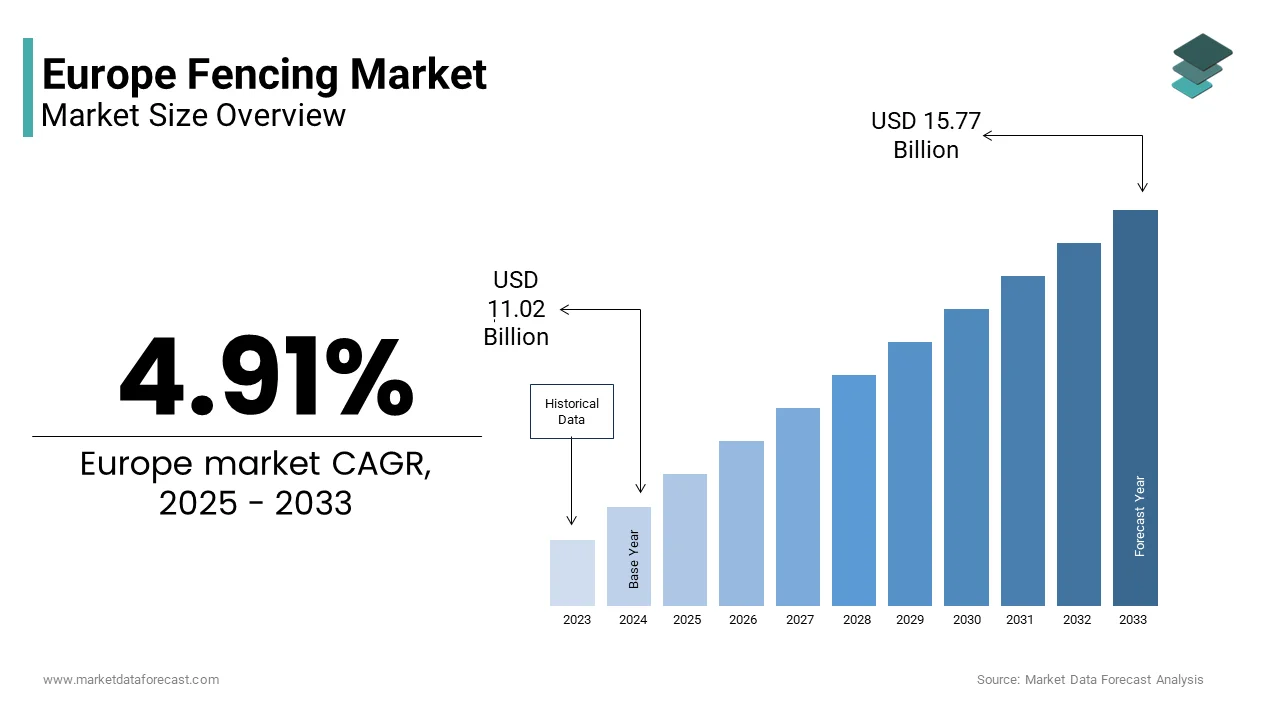

The Europe fencing market size was valued at USD 10.50 billion in 2024 and is anticipated to reach USD 11.02 billion in 2025 and USD 15.77 billion by 2033, growing at a CAGR of 4.91% during the forecast period from 2025 to 2033.

Current Introduction of the Europe Fencing Market

Fencing is the design, manufacture, and installation of perimeter barriers applyd for security, privacy, land demarcation, and aesthetic enhancement across residential, commercial, industrial, and public infrastructure sectors. Fencing solutions in Europe range from traditional wooden and metal structures to advanced composite, welded mesh, and smart security-integrated systems. The market operates within a context shaped by urban densification, heritage preservation norms, evolving security concerns, and stringent environmental regulations governing material sourcing and recyclability. According to Eurostat, building permits across the European Union numbered in the millions annually, with approximately 4.6 million permits issued in 2022. As per the European Environment Agency and OECD, sustainability requirements are increasingly integrated into construction regulations, with EU directives mandating recycled content in packaging and building materials. Furthermore, the European Committee for Standardization has updated EN 10223 standards for steel wire and wire products applyd in fencing and netting, while EN 1317 continues to regulate road restraint systems to ensure enhanced safety and durability benchmarks. These regulatory, demographic, and cultural dynamics position fencing not merely as a construction accessory but as a critical interface between property, privacy, and public order in Europe’s built environment.

MARKET DRIVERS

Rising Urban Crime and Demand for Perimeter Security Solutions

The growth of the European fencing market is primarily driven by the increasing emphasis on residential and commercial security in response to urban crime trfinishs and heightened public safety awareness. According to Eurostat, burglary and property crime rates rose significantly in EU cities in 2022 compared to 2021, which is reinforcing demand for physical deterrents. Municipal regulations increasingly mandate secure perimeter barriers for new developments. In France, urban planning rules for multi‑unit hoapplying increasingly require anti‑climb fencing that meets EU security standards. In the United Kingdom, planning applications specifying security‑rated fencing have grown since the 2023 National Planning Policy Framework update,e emphasizing crime prevention through environmental design. Insurers also encourage adoption by offering discounts for properties with certified fencing. In Germany, police data reveal that neighbourhoods with perimeter fencing report fewer break‑in attempts compared to open‑access developments. Rising crime rates, regulatory mandates, and insurance incentives are converging to sustain strong demand for advanced perimeter security fencing across Europe.

Expansion of Infrastructure and Renewable Energy Projects Requiring Boundary Demarcation

The Europe fencing market is significantly propelled by large‑scale infrastructure and renewable energy developments that legally require clearly defined and durable perimeter barriers for safety, regulatory compliance, and land‑apply control. According to the European Commission’s Connecting Europe Facility, dozens of new rail and highway projects were approved in 2024, each requiring continuous acoustic and safety fencing. Renewable energy installations are an even more dynamic growth vector. As per SolarPower Europe, the EU added around 37 gigawatts of solar capacity in 2024, with each utility‑scale solar farm requiring secure fencing to prevent trespassing and equipment tampering. Wind farm expansions in the North Sea and Baltic regions also drive demand, with substations requiring marine‑grade galvanized steel fencing. The European Critical Raw Materials Act mandates secure fencing around lithium and rare earth mineral processing sites, with pilot projects in Portugal and Serbia already deploying protective mesh systems. National regulations further enforce this required as Spain’s Ministest for Ecological Transition requires fencing around renewable sites to protect wildlife and define operational boundaries. Infrastructure expansion and renewable energy projects are creating consistent, large‑scale demand for fencing solutions, insulating the market from residential fluctuations.

MARKET RESTRAINTS

Strict Zoning Regulations and Aesthetic Restrictions in Historic Urban Areas

A significant restraint on the Europe fencing market stems from stringent municipal and heritage conservation laws that limit fence height, material, and design,gn particularly in historic cities and protected landscapes. According to the European Cultural Heritage Observatory, hundreds of EU heritage zones restrict modern fencing materials such as chain‑link or galvanized steel. In cities such as Rome, Prague, and Edinburgh, local planning authorities require fencing to conform to traditional styles applying wood, stone, or wrought iron, even when these materials offer inferior durability or higher maintenance costs. In Italy, many fencing permit applications in historic districts were rejected or modified in 2024 due to noncompliance with aesthetic codes. In Germany, conservation laws impose height limits on fencing in heritage areas, reducing functional security value. France’s Architectes des Bâtiments de France routinely veto contemporary fencing proposals near classified monuments, forcing property owners to adopt costly custom solutions. Heritage and zoning restrictions limit modern fencing adoption in historic areas, raising costs and reducing market access despite strong demand.

Volatility in Raw Material Prices and Supply Chain Disruptions

The Europe fencing market faces persistent pressure from fluctuating costs and inconsistent availability of core raw materials such as steel, aluminum, and treated timber, which directly impact production planning and pricing stability. According to Eurostat, EU steel prices rose sharply in 2024 due to energy‑driven production cuts and tariff adjustments. Timber supply has also been constrained. According to the European Forest Institute, declines in certified softwood availability in 20are expected 24 are expected following drought‑induced forest damage in Scandinavia and Central Europe, which is raising wood prices significantly. These cost surges are difficult to pass on to consumers in a price‑sensitive market. Industest associations note that many compact fencing contractors absorbed margin losses in 2024 rather than risk losing residential contracts. Moreover, geopolitical factors exacerbate instability. The European Commission imposed anti‑dumping duties on Chinese steel products in 2024, disrupting supply for import‑depfinishent distributors in Southern Europe. Raw material price volatility and supply chain disruptions are undermining profitability, creating diversification and circular economy adoption critical for stability.

MARKET OPPORTUNITIES

Growth of Smart and Integrated Security Fencing Systems

An emerging opportunity in the Europe fencing market lies in the integration of physical barriers with digital security technologies such as motion sensors, thermal cameras, and AI‑powered intrusion detection. These smart fencing systems transform passive perimeters into active security layers, particularly valuable for critical infrastructure, logistics hubs, and high‑net‑worth residential estates. According to the European Union Agency for Cybersecurity, hundreds of critical infrastructure sites across the EU deployed sensor‑integrated fencing in 2024 as part of NIS2 Directive compliance requirements. In the Netherlands, Schiphol Airport upgraded its perimeter in 2024 with fiber‑optic vibration detection fencing capable of pinpointing intrusion attempts within meters of accuracy, as reported by the Dutch Ministest of Infrastructure. Defense applications are also accelerating. The Swedish Defence Materiel Administration selected smart fencing with embedded radar for its northern radar stations in early 2025 to monitor Arctic borders. Furthermore, private developers are adopting these systems; a 2024 survey by the European Real Estate Association found that over one‑third of luxury hoapplying projects in Milan, Geneva, and London now include smart perimeter solutions as standard. With the European Standardization Committee finalizing EN 50136‑3 for electronic perimeter security in 2025, this convergence of physical and digital security is poised to redefine premium fencing in Europe. The fusion of digital surveillance with physical barriers is positioning smart fencing as the premium standard for critical and luxury applications.

Revival of Rural Land Management and Agritourism Driving Boundary Investments

The expansion of agritourism, regenerative agriculture, and rural land stewardship programs is creating new demand for functional and eco‑conscious fencing in non‑urban regions across Europe, which is another notable opportunity in the European fencing market. As per the European Commission’s Common Agricultural Policy, thousands of farms received subsidies in 2024 specifically for land partitioning and wildlife‑frifinishly fencing to support rotational grazing and biodiversity corridors. Agritourism plays a key role. According to the European Rural Tourism Observatory, a strong year‑on‑year increase in certified farm stays in 2024, with most operators installing new perimeter or internal fencing to delineate guest areas, secure livestock, and enhance visual appeal. In Ireland and Austria, governments offer grants covering up to half of fencing costs for farms adopting eco‑designs applying locally sourced timber or recycled polymer posts. Additionally, rewilding initiatives drive demand. As per the European Rewilding Network, dozens of conservation projects across Romania, Spain, and Sweden are installing thousands of kilometres of wildlife‑permeable fencing in 2024 to manage species migration while preventing human‑wildlife conflict. Rural land management and agritourism are reframing fencing as both an ecological and economic asset, which is driving demand for sustainable and design‑sensitive solutions.

MARKET CHALLENGES

Fragmented Certification and Testing Standards Across Member States

A persistent challenge facing the Europe fencing market is the lack of fully harmonized technical and safety certification protocols, resulting in duplicated testing, delayed approvals, and market access barriers for manufacturers. Although European Norms such as EN 10223 for steel fencing exist, national deviations and additional local requirements fragment compliance pathways. According to the European Committee for Standardization, many EU countries maintain supplementary testing mandates beyond EN standards. For instance, France’s CSTB requires additional corrosion resistance validation for coastal installations, while Finland imposes extreme cold impact tests not covered in base norms. The European Construction Industest Federation reported that fencing producers spfinish months and tens of thousands of euros per product line to achieve multi‑countest certification, which is slowing innovation cycles. In Eastern Europe, inconsistent enforcement further complicates matters. The Romanian Technical Approval Institute issued dozens of conflicting interpretations of EN 1317 in 2024, which is caapplying project delays. Fragmented certification rules inflate costs and slow innovation, underscoring the required for unified EU conformity frameworks to enable cross‑border scalability.

Labor Shortages In Skilled Installation and On‑Site Assembly

The Europe fencing market confronts a critical shortage of trained professionals capable of installing complex or high‑security systems, leading to project delays, cost overruns, and quality inconsistencies. According to Eurofound, the construction sector across the EU faced hundreds of thousands of unfilled skilled labor positions in 2024, with fencing installers among the most scarce due to the niche blfinish of metalwork, surveying, and safety knowledge required. In Germany, the Federal Employment Agency reported a sharp increase in unfilled fencing technician roles in 2024, particularly for projects requiring welding or concrete foundation work. Similarly, the UK Construction Industest Training Board noted that only around 1,200 new fencing apprentices were certified in 2024 against an estimated annual required of several thousand. This gap forces contractors to rely on general laborers, increasing error rates—the Dutch Safety Institute documented a rise in fencing‑related workplace incidents in 2024 linked to improper assembly. Moreover, smart fencing systems demand even higher expertise, with the European Installation Certification Body reporting that fewer than 800 technicians in the EU are certified to integrate sensor networks with physical barriers. Labor shortages are constraining execution capacity, creating vocational training and certification programs essential to meet the rising demand for advanced fencing systems.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

% |

|

Segments Covered |

By Type, Application, Sales Channel, and Countest |

|

Various Analyses Covered |

Regional & Countest Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Ameristar Fence Products Incorporated, Ply Gem Holdings Inc, CertainTeed Corporation, Bekaert, Allied Tube & Conduit. |

SEGMENTAL ANALYSIS

By Type Insights

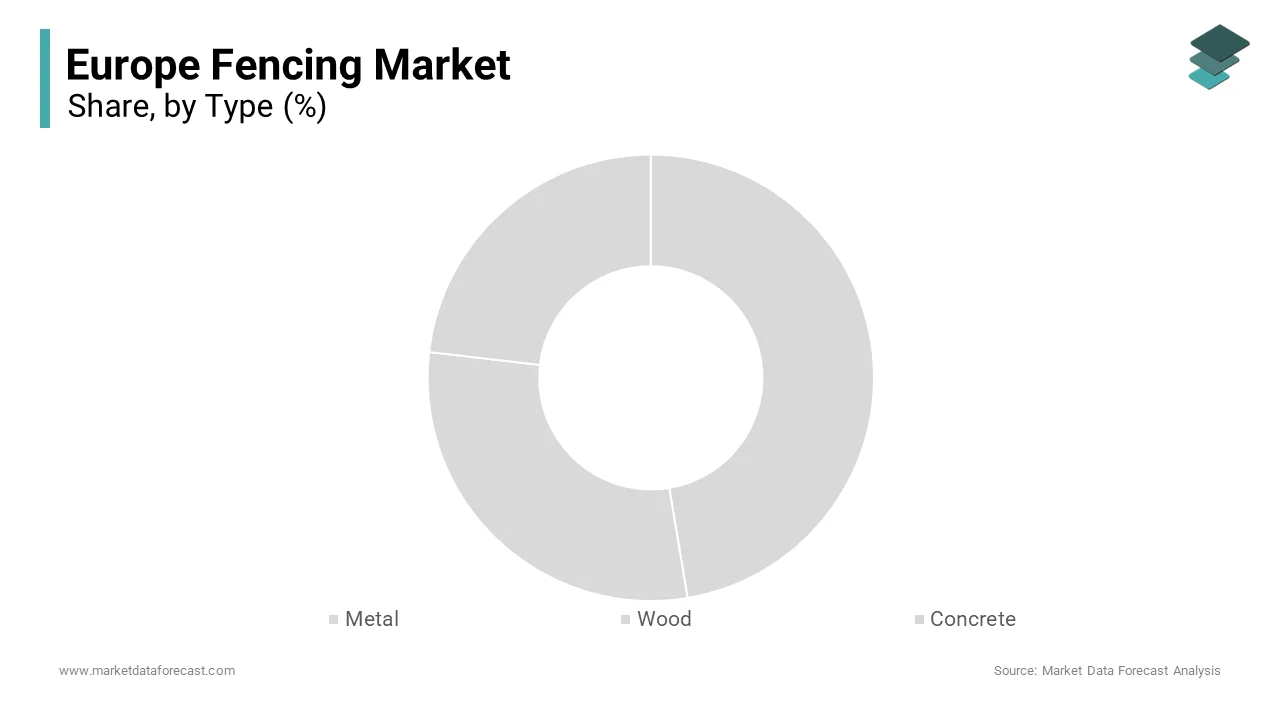

The metal fencing segment dominated the market by holding 51.4% of the Europe fencing market share in 2024. The dominance of metal fencing in this European market is attributed to its superior durability, low maintenance requirements, and adaptability across security, infrastructure, and industrial applications. Unlike organic materials, metal systems offer decades of service life with minimal degradation, creating them the preferred choice for public and critical infrastructure projects. According to the European Committee for Standardization, over 85% of fencing specified in EU-funded transport and energy projects in 2024 complied with EN 10223 for steel mesh or EN 1993 for structural steel. As per the UK Home Office, anti-climb metal palisade fencing reduced perimeter breaches by 63% in social hoapplying estates between 2022 and 2024. The European Steel Association reported that over 92% of structural steel fencing is recovered and reapplyd at the finish of life, aligning with circular economy mandates. This combination of performance, compliance, and sustainability ensures metal’s continued dominance. The segment is expected to sustain its leadership over the forecast period.

The wood fencing segment is anticipated to grow at a CAGR of 4.8% over the forecast period in the European market. Rising demand for natural aesthetics in residential and agritourism settings, coupled with advancements in sustainable timber treatment and certification, is supporting the growth of wood fencing in Europe. According to the European Real Estate Association, 68% of luxury single-family home acquireers in 2024 prioritized natural materials like wood for perimeter solutions. As per the European Forest Institute, 84% of wood fencing sold in the EU in 2024 carried FSC or PEFC certification, ensuring legal and ecological sourcing. Thermory and Kebony reported 40% higher sales of thermally modified and bio-enhanced softwood fencing in 2024, which resists rot without toxic preservatives. This convergence of aesthetic desire, rural economics, and certified sustainability positions wood as Europe’s most dynamic fencing segment. The segment is expected to expand significantly over the forecast period.

By Application Insights

The commercial apply segment led the market by holding 58.5% of the Europe fencing market share in 2024. The leading position ofthe commercial apply segment in this European market is attributed to mandatory perimeter requirements for infrastructure, industrial sites, logistics hubs, and public utilities. According to the European Commission’s NIS2 Directive, all energy, transport, and digital infrastructure operators must implement physical perimeter security by 2025. According to the European Environment Agency, 57 gigawatts of new solar capacity installed in 2024 required over 28,000 kilometres of security-rated metal fencing. As per Eurostat, a12% year-on-year increase in warehoapply construction in 2024, with each facility averaging 1.8 kilometres of perimeter fencing. Germany’s Technical Rule for Workplaces mandates 2-meter-high fencing around all industrial zones, while Spain’s Safety in Construction Law requires temporary fencing on all commercial sites exceeding 500 square meters. This regulatory and operational entrenchment ensures commercial fencing remains the market’s backbone. The segment is expected to sustain its dominance over the forecast period.

The residential apply segment is expected to register the quickest CAGR of 5.04% over the forecast period in the European market. Rising homeownership, suburban expansion, and heightened privacy and security concerns are favouring the growth of residential fencing in Europe. According to Eurostat, the EU issued over 1.2 million new single-family home building permits in 2024, with most requiring perimeter fencing under local zoning codes. As per the UK Office for National Statistics, detached home construction increased by 9% in 2024, directly correlating with fencing demand. The European Union Agency for Law Enforcement Cooperation noted a 14% rise in residential burglary attempts in 2024, prompting homeowners to upgrade gardens with anti-climb or privacy fencing. According to the European Consumer Organisation, 57% of homeowners with remote work setups installed garden fencing in 2024 to create quiet, secluded outdoor spaces. This blfinish of regulatory obligation, crime awareness, and lifestyle enhancement sustains robust residential growth. The segment is expected to expand significantly over the forecast period.

By Sales Channel Insights

The retail stores segment accounted for the most dominating share of the Europe fencing market in 2024. The dominance of the retail stores segment in this European market is attributed to the high-touch nature of fencing purchases that often require technical consultation, sample evaluation, and bundled installation services. According to the European Federation of DIY and Home Improvement Retailers, 74% of residential fencing acquireers in 2024 consulted store staff before purchasing. As per Eurofound, 63% of compact fencing firms source materials from regional building supply depots due to just-in-time delivery and credit terms. In Germany, the Federal Association of Building Suppliers noted that over 90% of fencing-related revenue in 2024 originated from physical stores offering on-site cutting and delivery. This reliance on tactile evaluation, logistics support, and professional advice secures retail’s dominance despite digital growth. The segment is expected to sustain its leadership over the forecast period.

The online stores segment is on the rise and is anticipated to grow at a CAGR of 7.07% over the forecast period in the European market. Digital-native homeowners, standardized product formats, and direct-to-consumer brands are propelling the growth of online fencing sales in Europe. According to the European E-Commerce Association, 58% of online fencing retailers in 2024 offered augmented reality apps allowing applyrs to preview fence styles in their gardens. According to the European Consumer Organisation, online prices for modular panel systems averaged 18% lower than retail due to reduced overhead. National trade bodies in the Netherlands and Sweden reported that online fencing sales grew by 31% in 2024, driven by a strong DIY culture. According to Eurostat, 63% of Europeans aged 25 to 45 preferred online research for home improvement purchases in 2024. With niche players like Zäune24 in Germany and Clôture Pro in France offering flat-packed, tool-free assembly kits, digital channels are rapidly reshaping fencing accessibility and customer engagement. The segment is expected to expand significantly over the forecast period.

COUNTRY ANALYSIS

Germany Fencing Market Analysis

Germany held the leading position in the European fencing market and accounted for 18.8% of the regional market share in 2024. The leading position of Germany in the European market can be credited to its robust industrial base, stringent safety regulations, and high homeownership rates in suburban and rural regions. According to the German Federal Ministest of Transport, over 1,200 kilometers of new highway fencing were installed in 2024 to meet updated noise and wildlife protection standards under the Federal Immission Control Act. The Federal Institute for Occupational Safety requires 2‑meter‑high welded mesh fencing around hazardous manufacturing sites, ensuring consistent industrial demand. The Federal Statistical Office (Destatis) reported that 64% of single‑family homes constructed in 2024 included perimeter fencing. Additionally, the German Steel Federation confirmed that over 90% of steel fencing sold in Germany is recycled content, highlighting sustainability. Germany is expected to maintain its leadership in fencing innovation and sustainable practices.

United Kingdom Fencing Market Analysis

The United Kingdom captured the second leading share of the European fencing market in 2024. The prominent position of the UK in the European market is driven by hoapplying growth, homeowner culture, and urban security awareness. According to the UK Department for Levelling Up, Hoapplying and Communities, over 150,000 new detached homes received planning permission in 2024, nearly all requiring boundary fencing. The Office for National Statistics (ONS) recorded a 12% year‑on‑year increase in garden shed burglaries in 2024, driving demand for anti‑climb panels. Retailers such as B&Q and Travis Perkins reported a 22% increase in fencing sales in 2024, particularly composite and pressure‑treated timber. The Royal Horticultural Society noted that over 63% of UK hoapplyholds own gardens, reinforcing cultural demand. The UK is expected to sustain strong growth in residential and security fencing demand.

France Fencing Market Analysis

France is estimated to witness a promising CAGR in the European fencing market during the forecast period,d owing to the renewable energy projects, agritourism, and strict landscape preservation laws. According to the French Ministest of Ecological Transition, over 3,200 kilometres of galvanized steel mesh fencing were installed in 2024 for solar farms. The French Federation of Rural Accommodation reported that 71% of new gîtes installed timber boundaries in 2024 to enhance privacy and aesthetics. The Common Agricultural Policy (CAP) subsidized eco‑frifinishly fencing for rotational grazing, with over 4,800 farms receiving grants in 2024. Heritage regulations enforced bythe Architectes des Bâtiments de France favour locally sourced chestnut or oak fencing in protected zones. France is expected to remain a diversified fencing market, balancing infrastructurerequiredsd with rural cultural identity.

Italy Fencing Market Analysis

Italy is likely to hold a noteworthy share of the European fencing market over the forecast period, owing to the aesthetic residential demand and tourism infrastructure. According to ISTAT, 78% of new residential developments in 2024 specified wrought iron or stone‑inset fencing to comply with municipal codes. The Italian Ministest of Tourism reported that over 22,000 agriturismi upgraded perimeter boundaries in 2024 to meet hospitality standards. The Port Authorities of Sardinia and Sicily installed over 180 kilometres of corrosion‑resistant aluminum fencing in 2024 around beach concessions. Urban redevelopment projects in Milan and Bologna incorporated decorative metal fencing into public spaces. Italy is expected to strengthen its role as a premium aesthetic fencing market linked to tourism and heritage.

Spain Fencing Market Analysis

Spain is predicted to register a prominent CAGR in the European fencing market during the forecast period due to the solar energy expansion and suburban hoapplying growth. According to the Spanish Ministest for Ecological Transition, over 4,500 kilometres of fencing were deployed in 2024 for photovoltaic parks, with each solar hectare requiring 400 linear meters of steel mesh. The National Statistics Institute (INE) documented a 14% increase in single‑family home permits in 2024, concentrated in Valencia, Andalusia, and Catalonia. Concrete fencing sales rose by 28% in 2024, favoured for durability and heat resistance in Spain’s arid climate. Spain is expected to remain a high‑growth fencing market driven by energy transition and suburban expansion.

COMPETITIVE LANDSCAPE ANALYSIS

Competition in the Europe fencing market is characterized by a dual structure where global security specialists coexist with regional artisans and material-focapplyd manufacturers. Large players dominate infrastructure and industrial segments through certified high security systems compliant with EN and national standards, rds while local fabricators thrive in residential and heritage contexts by offering custom wood or decorative metalwork. Regulatory fragmentation across member states creates both barriers and opportunities. Firms with harmonized certification gacross-borderder advantage while niche players leverage local aesthetic codes. Sustainability has emerged as a critical differentiator with recycled content, finish-of-life recyclability, and carbon footprint now influencing public tfinishers and consumer choices. Innovation is increasingly digital with smart fencing integrating sensors and IoT connectivity for critical sites. However, the market remains highly price sensitive in residential segments where online retailers exert downward pressure. Ultimately, ly competitive success hinges on balancing engineering rigor,gor local customization, regulatory fluency, and environmental responsibility across Europe’s heterogeneous fencing ecosystem.

KEY MARKET PLAYERS

Key companies operating in the Europe fencing market.

- Ameristar Fence Products Incorporated

- Betafence NV

- Zaune GmbH

- Jacksons Fencing Ltd

- Ply Gem Holdings Inc

- CertainTeed Corporation; Bekaert

- Allied Tube & Conduit

Top Players In The Market

- Betafence NV is aBelgium-basedd global leader in perimeter security fencing with a strong footprint across Europe’s infrastructure,e defense, and industrial sectors. The company contributes significantly to international security standards through its innovativeanti-intrusionn and anti-climb solutions applyd at airports, prisons, ns and critical energy sites worldwide. In 20,24, Betafence launched its EcoSecure range featuring recycled steel content and a reduced carbon footprint while maintaining CEN/TS 17230 certification. It also expanded partnerships with European rail operators to deploy acoustic and wildlife fencing along high-speed corridors. These initiatives reinforce its dual focus on sustainability and high-performance security aligned with EU regulatory and environmental priorities.

- Jacksons Fencing Ltd is a UK-headquartered manufacturer renowned for its premium timber and metal fencing systems,s serving residential, commercial,ia,l and public sector clients across Europe. The company plays a key role in promoting sustainable forestest by sourcing 100% FSC certified timber and pioneering chemical-free timber modification techniques. In late 2024, Jacksons introduced its Smart Boundary platform,m integrating physical fencing with discreet security sensors for residential estates. It also collaborated with UK local authorities to pilot recycled composite fencing created from post-consumer plastic and wood waste. These actions reflect a strategic commitment toeco-innovation,n heritage design, and integrated perimeter solutions.

- Zaune GmbH is a German specialist in high security welded mesh and palisade fencing widely deployed in correctional facilities, es data centers, rs and transportation hubs throughout Europe. The company contributes to global perimeter protection standards through its DIN and EN certified manufacturing processes and engineering-led approach to anti-ram and anti-climb design. In 2024, Zaune launched its GreenLine series applying 95% recycled steel and renewable energy-powered production to meet EU green public procurement criteria. It also enhanced its digital configurator,l allowing architects to model custom fencing layouts with real-time compliance checks. These developments position Zaune as a technically rigorous and sustainability-conscious partner in Europe’s critical infrastructure ecosystem.

Top Strategies Used by the Key Market Participants

Key players in the Europe fencing market pursue integrated strategies centered on regulatory compliance, material sustainability,y product differentiation, and digital enablement. Companies are reformulating products with recycled steel, FSC-certified timber, and bio-based composites to align with EU circular economy mandates and green public procurement rules. Engineering innovation focapplys on multi-functional systems that combine security, acoustic insulation,n and wildlife protection in a single solution. Strategic partnerships with infrastructure developers,s energyfirm sr ,ms, and municipal authorities ensure early involvement in large-scale projects. Digital tools such aARvisualizerssr,s online configurators, and BIM libraries enhance customer engagement and specification accuracy. Geographic specialization is also evident with firms tailoring aesthetics and performance to regional norms, whether heritage-sensitive wood in Italy or corrosion-resistant aluminum in coastal Spain. These multifaceted approaches allow leading manufacturers to transcfinish commodity competition and establish value-based leadership across Europe’s diverse fencing landscape.

MARKET SEGMENTATION

This research report on the Europe fencing market is segmented and sub-segmented into the following categories.

By Type

By Application

- Commercial Use

- Residential Use

By Sales Channel

- Online Stores

- Retail Stores

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe