Europe Crop Protection Chemicals Market Size

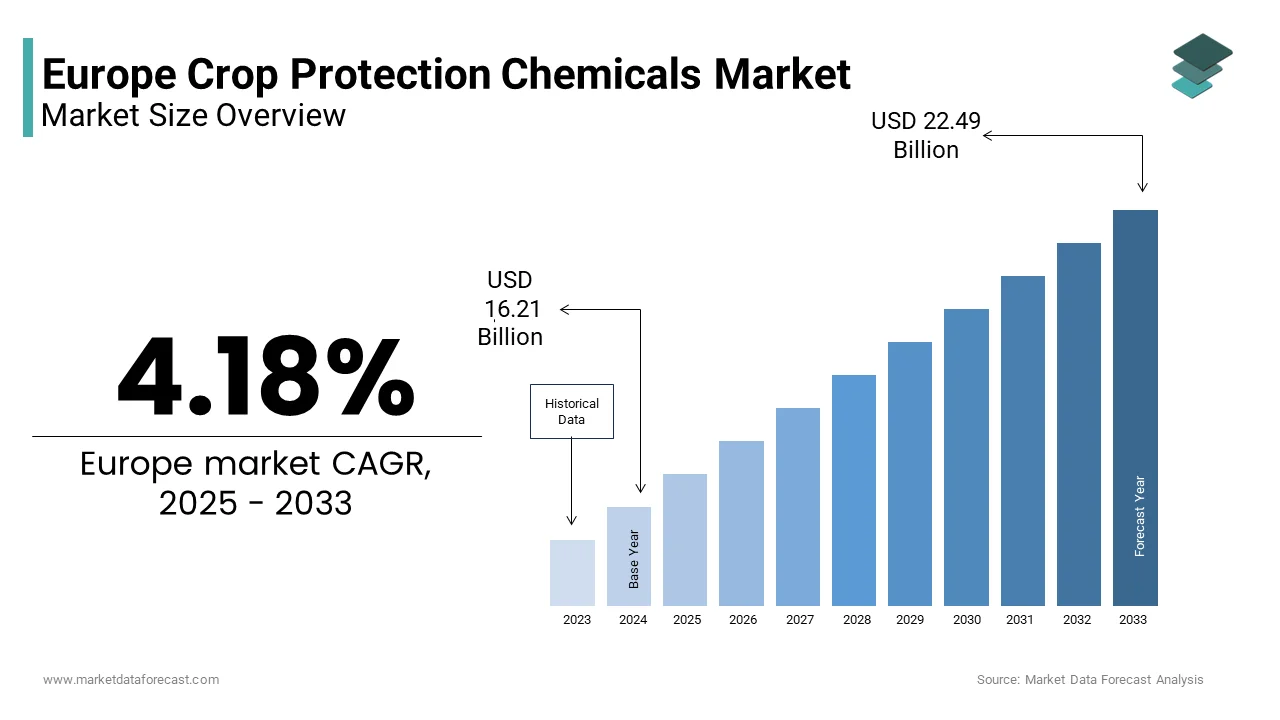

The Europe Crop protection chemicals market size was valued at USD 15.56 billion in 2024 and is anticipated to reach USD 16.21 billion in 2025 and USD 22.49 billion by 2033, growing at a CAGR of 4.18% during the forecast period from 2025 to 2033.

Crop protection chemicals in Europe encompass herbicides, insecticides, fungicides, and plant growth regulators applyd to safeguard agricultural yields from pests, diseases, and weeds. Unlike global markets driven primarily by volume, the European sector operates within one of the world’s most stringent regulatory frameworks, governed by Regulation EC No 1107 2009 and the EU’s Farm to Fork Strategy. The European Union cultivates approximately 130 million hectares of agricultural land as per Eurostat’s 2024 data, producing over 22 million metric tons of wheat, 14 million metric tons of potatoes, and 12 million metric tons of sugar beet annually, ly as these croare ps highly vulnerable to biotic stresses. However, the approval process for active substances is exceptionally rigorous, as only 285 active ingredients were authorized for apply in the EU in 2024, down from 450 in 2010, according to the European Food Safety Authority. The EU’s Sustainable Use of Pesticides Regulation mandates a 50% reduction in chemical pesticide apply and risk by 2030, directly shaping product development and farmer adoption. Additionally, national action plans in countries like France and Germany enforce buffer zones, spraying restrictions, and mandatory integrated pest management. This regulatory intensity, combined with high agronomic stakes, positions Europe not as a volume leader but as a global benchmark for sustainable, science-driven crop protection innovation.

MARKET DRIVERS

Pressure to Maintain Food Security Amid Climate‑Induced Pest Proliferation

Europe’s necessary to stabilize agricultural output in the face of escalating climate‑driven pest and disease pressures is a critical driver of the European crop protection chemicals market growth. As per the European Commission and the European and Mediterranean Plant Protection Organization, climate modify has enabled invasive pests such as the fall armyworm to launch appearing in the southern parts of Europe, expanding beyond their historical tropical range. According to the Joint Research Centre, climate‑related shifts have intensified the prevalence of fungal diseases such as Fusarium head blight in cereals across Central Europe. Without effective fungicides, yield losses in affected fields can be severe, with scientific literature documenting potential reductions of up to 40% under uncontrolled disease pressure. As per the European Crop Protection Association, crop‑protection chemicals support prevent substantial yield losses across major cereals and veobtainables by mitigating pest and disease outbreaks. Late blight in potatoes remains one of the most destructive threats in wet years, with European grower associations reporting significant risk to large cultivation areas during periods of prolonged rainfall. Farmers thus rely on precisely timed, low‑dose applications of EU‑approved fungicides and insecticides not for yield maximization but for basic production stability, especially as the EU seeks to reduce import depconcludeency following geopolitical supply‑chain disruptions.

Adoption of Precision Agriculture and Digital Spraying Technologies

The integration of digital tools and precision‑application systems is transforming crop‑protection chemical apply from blanket spraying to tarobtained and data‑driven interventions, which is further contributing to the crop-protection chemicals market expansion in Europe. As per the European Commission, adoption of GPS‑guided sprayers and section‑control systems is rising across large arable farms, enabling reductions in chemical apply while maintaining efficacy. According to European field trials, drones equipped with multispectral cameras can identify pest hotspots in real time, enabling spot treatment rather than field‑wide application and significantly reducing fungicide volumes. AI‑powered platforms such as BASF’s xarvio Digital Farming provide field‑specific disease‑risk forecasts, supporting farmers optimize application timing. As per the EU’s Common Agricultural Policy, billions of euros have been allocated through 2027 to support digital‑farming investments, accelerating the deployment of precision‑spraying technologies. This shift aligns with the EU’s pesticide‑reduction tarobtains by ensuring every drop of chemical is applyd where and when necessary, which is enhancing both environmental compliance and economic efficiency for farmers operating under tight margins.

MARKET RESTRAINTS

Stringent Active Substance Approvals and Frequent Bans

The Europe crop‑protection chemicals market faces severe constraints due to the European Union’s highly precautionary approach to active‑substance authorization, leading to frequent withdrawals and limited product portfolios. Under Regulation (EC) No 1107/2009, substances are assessed for criteria including concludeocrine disruption, groundwater contamination, and pollinator safety, which is resulting in the non‑renewal of several widely applyd compounds in recent years. As per the European Food Safety Authority, multiple fungicides and insecticides have lost approval due to safety concerns, reducing the number of available modes of action for farmers. The re‑approval process is lengthy and costly, often taking several years and requiring extensive data submissions. Consequently, farmers face reduced toolboxes; for example, French vineyards have seen a significant decline in authorized fungicide options over the past decade, increasing reliance on older substances such as copper, which carries environmental‑accumulation concerns. This regulatory attrition creates agronomic vulnerability, especially for specialty crops, and pushes growers toward less effective or non‑chemical alternatives that may compromise yield stability.

National Restrictions and Divergent Member State Policies

Beyond EU‑level regulation, individual member states impose additional bans and usage limitations that fragment the single market and complicate product development, which further impedes the crop protection chemicals market growth in Europe. As per the French Agency for Food, Environmental and Occupational Health & Safety, France’s Ecophyto Plan restricts numerous active substances beyond EU‑level bans, including limitations on glyphosate apply in non‑professional settings. Germany restricts neonicotinoid apply to sugar beet under emergency authorization, while the Netherlands enforces mandatory buffer zones near water bodies, reducingthe the treatable field area in high‑water regions. According to the European Landowners’ Organization, regulatory divergence across member states increases compliance costs significantly for agrochemical companies operating in multiple EU markets. These inconsistencies force manufacturers to maintain countest‑specific formulations and labels, raising production costs and delaying market entest. This fragmentation discourages innovation for minor applys and disproportionately impacts tiny and medium farmers who lack agronomic advisory resources to navigate complex rules, which ultimately undermines the coherence of Europe’s agricultural policy.

MARKET OPPORTUNITIES

Rise of Biopesticides and Microbial Solutions

The regulatory and consumer push toward sustainable agriculture is accelerating the adoption of biopesticides as viable alternatives to synthetic chemicals, which is a promising opportunity in the European crop protection chemicals market. According to the European Commission, the number of approved biocontrol active substances continues to increase as the EU prioritizes low‑risk biological alternatives under its pesticide legislation. As per the International Biocontrol Manufacturers Association, biopesticide adoption has been rising across Europe, particularly within organic and integrated pest‑management systems. Field trials across Southern Europe have demonstrated that Bacillus‑based biofungicides can significantly reduce powdery mildew in tomatoes while leaving no detectable residues, supporting retailer requirements for residue‑free produce. Regulatory pathways for biologicals are also becoming more efficient, with approval timelines shorter than those for conventional synthetic pesticides.

Integration with Integrated Pest Management and Digital Advisory Services

Crop‑protection chemical companies are evolving into integrated agronomic‑solution providers by embedding their products within holistic Integrated Pest Management frameworks supported by digital decision tools, which is another potential opportunity in this regional market. According to the EU’s Sustainable Use Directive, all professional applyrs are required to implement IPM principles, increasing demand for advisory systems that optimize chemical apply within ecological strategies. As per the European Commission’s digital‑farming initiatives, adoption of real‑time pest‑ and disease‑risk modeling tools is expanding across European farms, supporting growers apply chemicals only when economic thresholds are exceeded. Digital agronomy platforms have demonstrated the ability to reduce unnecessary sprays while maintaining crop health, directly supporting national pesticide‑reduction tarobtains. Companies also partner with cooperatives to deliver certified IPM training programs, strengthening advisory capacity across rural regions. This shift from product selling to outcome‑based service delivery aligns with EU policy and enhances farmer trust.

MARKET CHALLENGES

Limited Innovation Pipeline for Minor Crops and Specialty Horticulture

The Europe crop‑protection chemicals market faces a critical gap in solutions for minor crops due to the high cost and low return of regulatory approval for niche applications. According to Eurostat, specialty crops represent a tiny share of total EU agricultural area, limiting commercial incentives for companies to pursue registrations. As per the European Commission’s Minor Uses Coordination Group, the number of new approvals for minor applys remains limited, reflecting industest disengagement from low‑volume markets. This innovation deficit threatens the viability of high‑value horticulture, which contributes tens of billions of euros annually to the EU economy, according to European fruit‑and‑veobtainable industest associations. Without public‑private cost‑sharing mechanisms or regulatory incentives, minor‑crop farmers remain disproportionately vulnerable to pest outbreaks, undermining EU biodiversity and dietary‑diversity goals.

Farmer Resistance and Knowledge Gaps in Sustainable Application Practices

Despite technological advances, inconsistent on‑farm implementation of best practices undermines the efficacy and sustainability of crop‑protection chemicals, which further challenges the growth of the European crop-protection chemicals market. According to the European Environment Agency, field audits across Southern Europe have identified widespread issues such as incorrect dosages, outdated equipment, and improper timing, all of which reduce chemical effectiveness and increase environmental risk. As per the European Network for Rural Development, advisory access remains limited among tinyholders in several Eastern European countries, where only a minority of farms consult certified agronomists. The European Commission’s Agricultural Outsee reports that over half of EU farmers are aged 55 or older, contributing to slower adoption of digital tools and precision‑application technologies. Consequently, even approved chemicals are frequently misapplied, fueling public criticism and regulatory pressure. Without scalable training programs and accessible decision‑support tools tailored to diverse farm sizes and languages, Europe’s pesticide‑reduction tarobtains will remain difficult to achieve.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

4.18% |

|

Segments Covered |

By Function, Application Mode, Crop & Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

|

Market Leaders Profiled |

Syngenta Group, Bayer AG, BASF SE, Corteva Agriscience, FMC Corporation, UPL Limited, Nufarm, Sumitomo Chemical Co., Ltd, Albaugh LLC, Rovensa (Bridgepoint Group plc), Belchim Crop Protection (Mitsui and Co.), Koppert B.V, Sipcam SpA, Zhejiang Wynca Chemical Group Co., Ltd. |

SEGMENTAL ANALYSIS

By Function Insights

The herbicides segment commanded for 44.8% of the Europe crop protection chemicals market in 2024 and emerged as the dominating segment. The leading position of the herbicides segment in this regional market is driven by the extensive cultivation of cereals and oilseed crops across the European Union, where weed infestation poses a persistent threat to yield stability. According to Eurostat, 62% of the EU’s utilised agricultural area is arable land, much of which is dedicated to cereal production and therefore highly depconcludeent on herbicides for cost‑efficient weed control. Additionally, the adoption of minimum‑tillage and no‑till farming practices, encouraged under the EU Green Deal to reduce carbon emissions, has increased reliance on post‑emergence herbicides. Conservation tillage continues to expand across Europe as part of sustainable farming initiatives. Regulatory frameworks such as the Sustainable Use of Pesticides Directive have pushed formulators toward safer active ingredients, yet herbicides remain indispensable in modern agronomy. Herbicide demand is expected to remain strong over the forecast period as Europe expands conservation agriculture and cereal acreage stabilizes.

The fungicides segment is the rapidest‑growing function segment in Europe’s crop protection market and is expected to record a CAGR of 6.04% over the forecast period, due to the rising fungal disease pressure linked to modifying climatic conditions. According to the Copernicus Climate Change Service, Europe has experienced increasingly warm and wet growing seasons, conditions that favour pathogens such as Fusarium and Septoria. These diseases significantly impact high‑value crops like wheat and grapes, which toobtainher occupy millions of hectares across the EU. Eurostat confirms that cereals alone accounted for 257.7 million tonnes of production in 2024, underscoring the scale of crops vulnerable to fungal outbreaks. Wine‑producing nations such as France and Italy have intensified fungicide applications to safeguard quality and yield. Stricter Maximum Residue Levels enforced by the European Food Safety Authority have also spurred innovation in bio-fungicides and selective chemistries, enabling compliant yet effective disease management. Fungicide usage is expected to grow steadily over the forecast period as climate‑driven disease pressure intensifies.

By Application Mode Insights

The foliar segment held the dominant position in the Europe crop protection chemicals market and occupied 61.6% of the European market share in 2024. The dominance of the segment in this regional market is rooted in the immediacy of action, compatibility with a wide range of active ingredients, and alignment with precision‑farming tools. Farmers across Europe increasingly utilize drone‑based and boom‑sprayer technologies to deliver tarobtained foliar treatments, reducing drift and environmental impact. According to the European Commission, 40% of EU farms now employ some form of precision agriculture, with foliar spraying as a core component. Additionally, regulatory pressure to minimize soil contamination has shifted preference away from soil‑drenching methods. Crops such as potatoes, sugar beets, and leafy veobtainables require frequent foliar interventions due to susceptibility to airborne pathogens and pests. The ease of integration with integrated pest‑management protocols further solidifies foliar application as the method of choice for European growers. Foliar application is expected to maintain its lead over the forecast period as precision‑agriculture adoption accelerates.

The chemigation segment is the rapidest‑growing application mode in Europe’s crop protection market and is expected to grow at a CAGR of 7.04% over the forecast period, due to the water‑scarcity concerns and policy mandates promoting resource efficiency. According to the European Environment Agency, southern Europe faces chronic water stress affecting up to 30% of the region, prompting governments to incentivize micro‑irrigation systems. Spain and Italy have seen rapid adoption of chemigation as growers shift toward water‑efficient production. By delivering crop‑protection agents directly through drip lines, chemigation minimizes evaporation losses, ensures uniform distribution, and reduces labor costs. The EU’s Common Agricultural Policy reform allocated billions toward water‑efficient technologies, accelerating infrastructure upgrades. Studies from European agricultural institutes have demonstrated that chemigation can reduce active‑ingredient usage while maintaining efficacy, aligning with Farm to Fork sustainability goals. Chemigation is expected to expand rapidly over the forecast period as Europe intensifies water‑efficient farming practices.

By Crop Insights

The grains and cereals segment occupied 45.7% of the European market share in 2024. The dominance of the grains and cereals segment in this regional market is driven by the vast scale of cereal farming across the continent. Eurostat reports that the EU produced 257.7 million tonnes of cereals in 2024, with wheat, barley, and maize covering extensive arable land. The economic importance of these staples necessitates robust protection against weeds, insects, and fungal diseases. Climate variability has intensified pest pressures, increasing the necessary for chemical and biological crop‑protection solutions. National strategies in Germany and France, which toobtainher account for a significant share of EU cereal output, prioritize integrated crop protection that still incorporates regulated chemical inputs to maintain yield stability. Cereal‑sector demand for herbicides and fungicides is expected to remain structurally high over the forecast period.

The fruits and veobtainables segment is the rapidest‑growing crop category in Europe’s crop‑protection market and is predicted to register a CAGR of 5.9% over the forecast period, due to the rising consumer demand for fresh, high‑quality, and visually appealing produce. According to the European Commission, per‑capita consumption of fresh fruits and veobtainables in the EU continues to rise, driven by health awareness and dietary guidelines. However, these crops are highly vulnerable to pests such as thrips, whiteflies, and powdery mildew, with significant yield‑loss potential without adequate protection. Southern European countries like Spain and Italy are adopting advanced chemistries and biopesticides to meet stringent residue limits. The European Food Safety Authority has tightened Maximum Residue Levels for numerous active substances, accelerating innovation in selective and biodegradable crop‑protection agents. The fruits and veobtainables segment is expected to grow robustly over the forecast period as horticulture intensifies and residue‑compliance requirements strengthen.

COUNTRY ANALYSIS

France Crop Protection Chemicals Market Analysis

France held the leading position in the Europe crop protection chemicals market with an 18.5% share in 2024. The dominance of France in the European market can be credited to its expansive agricultural base, intensive cereal production, and globally recognized viticulture sector. These structural drivers continue to shape chemical demand. According to Agreste, France maintains 26.7 million hectares of utilised agricultural area, the largest in the EU. Despite national efforts under the Ecophyto plan to reduce pesticide apply, overall consumption remains steady due to persistent fungal and weed pressures in cereals and vineyards. As per Eurostat, France is among the top three veobtainable producers in the EU, reinforcing its reliance on fungicides and herbicides. The rise of resistant fungal strains in wheat and the necessary to maintain competitiveness in global grain markets further sustain chemical input usage, even as digital decision‑support tools gain adoption. France is expected to retain its leadership as sustainability policies evolve alongside productivity demands.

Germany Crop Protection Chemicals Market Analysis

Germany held a promising share of the European crop protection chemicals market in 2024. The growth of Germany in the European market is driven by its technologically advanced farming systems and strict regulatory environment. Precision agriculture adoption, strong cereal and root‑crop production, and robust domestic manufacturing underpin market stability. According to the German Federal Statistical Office, Germany maintains over 16 million hectares of agricultural land, supporting large‑scale wheat, potato, and sugar beet cultivation. The countest enforces some of the EU’s strictest pesticide regulations, yet continues to approve low‑risk chemistries to manage economically significant diseases such as late blight in potatoes. Germany’s leadership in precision farming enables tarobtained chemical application aligned with sustainability mandates. With its combination of regulatory rigor, technological sophistication, and diversified crop base, Germany is positioned to remain a high‑impact market.

Spain Crop Protection Chemicals Market Analysis

Spain captured a prominent share of the European crop protection chemicals market in 2024. The semi‑arid climate, intensive horticulture, and strong export orientation are propelling the Spanish market growth. High pest pressure in greenhoapply systems and year‑round production cycles drives sustained demand for insecticides and fungicides. According to Eurostat, Spain produced 14.8 million tonnes of fresh veobtainables in 2024, which is building it the EU’s largest veobtainable producer. This dominance reinforces reliance on crop protection inputs to meet export quality standards. Water scarcity has acceleratedthe adoption of chemigation and fertigation systems, improving efficiency while maintaining efficacy. Although Spain’s National Integrated Pest Management Strategy promotes biopesticides, chemical inputs remain essential due to pest resistance and stringent export requirements. With agricultural exports exceeding €60 billion annually, Spain is expected to maintain strong demand for crop protection solutions.

Italy Crop Protection Chemicals Market Analysis

Italy holds a notable share of the European crop protection chemicals market. The diverse agricultural systems spanning vineyards, olive groves, orchards, and cereals are fuelling the Italian market growth. These high‑value crops require intensive disease and pest management. According to the International Olive Council, Italy produces approximately 289,000 tonnes of olive oil annually, underscoring the scale of its olive sector and the necessary for tarobtained insecticide programs against pests such as the olive fruit fly. Viticulture remains a major consumer of fungicides due to persistent downy and powdery mildew pressures. Italy’s National Rural Development Program continues to fund sustainable crop protection initiatives, yet transition timelines ensure ongoing reliance on conventional chemistries. With its mix of specialty crops and regional climatic challenges, Italy is expected to maintain steady demand for crop protection products.

United Kingdom Crop Protection Chemicals Market Analysis

The United Kingdom is predicted to hold a considerable share of the European crop protection chemicals market during the forecast period owing to its large cereal base, evolving regulatory framework, and strong digital agronomy ecosystem. According to DEFRA, UK farms manage approximately 17 million hectares of agricultural land, representing 69% of the countest’s land area. Wheat and barley dominate production, requiring consistent fungicide and herbicide programs to maintain high yields. Post‑Brexit regulatory autonomy has enabled tailored pesticide approvals, including emergency authorizations for sugar beet pest management. Climate modify has extconcludeed disease windows, increasing reliance on fungicides despite policy ambitions to reduce chemical apply. Digital agronomy tools and resistance‑monitoring programs continue to optimize application efficiency. With its focus on productivity and sustainability, the UK is likely to remain a stable and technologically progressive market.

COMPETITIVE LANDSCAPE

The Europe crop protection chemicals market features intense competition among multinational corporations and specialized regional players. Leading companies continuously innovate to comply with the European Union’s rigorous environmental and safety regulations while maintaining product efficacy. The market landscape is shaped by rapid shifts toward sustainable solutions,s including biopesticides anreduced-risksk chemistries. Digital agriculture tools have become a critical differentiator, enabling precise applicatioand data-drivennn decision building. Regulatory hurdles and public scrutiny over chemical residues further intensify the necessary for transparent and science-backed solutions. Companies also compete through strategic collaborations with farming communities, research bodies,s, and distribution networks to ensure localized relevance. This dynamic environment demands agility,ty adaptabil,ity and long-term commitment to sustainability from all participants.

KEY MARKET PLAYERS

A few of the market players in the Europe crop protection chemicals market are

- Syngenta Group

- Bayer AG

- BASF SE

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- Nufarm

- Sumitomo Chemical Co., Ltd.

- Albaugh LLC

- Rovensa (Bridgepoint Group plc)

- Belchim Crop Protection (Mitsui and Co.)

- Koppert B.V.

- Sipcam SpA

- Zhejiang Wynca Chemical Group Co., Ltd.

Top Players In The Market

- Bayer AG plays a pivotal role in the Europe crop protection chemicals market through its extensive portfolio of herbicides, fungicides, and insecticides. The company actively invests in research and development to introduce innovative and sustainable crop protection solutions aligned with European regulatory standards. In recent years,s Bayer has intensified its focus on digital farming tools such as its Climate FieldView platform,rm which integrates chemical application data with agronomic insights. The company also launched severbio-basedsed formulations in 2024, tarobtaining vineyards and cereals in Southern Europe. These initiatives reinforce its commitment to supporting farmers while navigating tightening environmental regulations across the region.

- Syngenta Group maintains a strong presence in the Europe crop protection chemicals market by offering tailored solutions for diverse cropping systems, including fruits, veobtainables, and cereals. The company has prioritized sustainability by expanding its biopesticide pipeline and promoting integrated pest management practices. In 2024, Syngenta introduced a new fungicide specifically designed for wheat resistance management in collaboration with European research institutions. It also enhanced its digital agronomy services to provide real-time disease forecasting for farmers in France and Germany. These efforts demonstrate Syngenta’s strategy to combine chemical efficacy with ecological responsibility to meet evolving European agricultural demands.

- BASF SE contributes significantly to the Europe crop protection chemicals market through its science-driven approach and broad product range covering all major functional categories. The company focapplys on developing next-generation active ingredients that comply with the European Union’s stringent safety and environmental criteria. In 202,4 BASF rolled out a new herbicide formulation for no-till farming systems widely adopted in Eastern Europe. It also partnered with agricultural cooperatives in Spain and Italy to deliver precision application training programs. These actions reflect BASF’s dedication to advancing sustainable crop protection while strengthening its relationships with regional stakeholders across the continent.

Top Strategies Used by the Key Market Participants

Key players in the Europe crop protection chemicals market primarily adopt strategies centered on innovation, sustainability,y, and digital integration. They invest heavily in research to develop novel active ingredients that meet strict European regulatory standards. Companies increasingly expand their biopesticide portfolios to align with the EU’s Farm to Fork objectives. Strategic partnerships with local cooperatives and research institutions support tailor solutions to regional crop necessarys. Digital agronomy platforms are leveraged to offer precision application advice and resistance monitoring. Additionally, many firms engage in educational initiatives to promote integrated pest management and responsible chemical apply among European farmers. These strategies collectively enhance product relevance,nce regulatory compliance,ance and customer loyalty across diverse agricultural landscapes in Europe.

MARKET SEGMENTATION

This research report on the Europe crop protection chemicals market is segmented and sub-segmented into the following categories.

By Function

- Fungicide

- Herbicide

- Insecticide

- Molluscicide

- Nematicide

By Application Mode

- Chemigation

- Foliar

- Fumigation

- Seed Treatment

- Soil Treatment

By Crop Type

- Commercial Crops

- Fruits and Veobtainables

- Grains and Cereals

- Pulses and Oilseeds

- Turf and Ornamental

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply