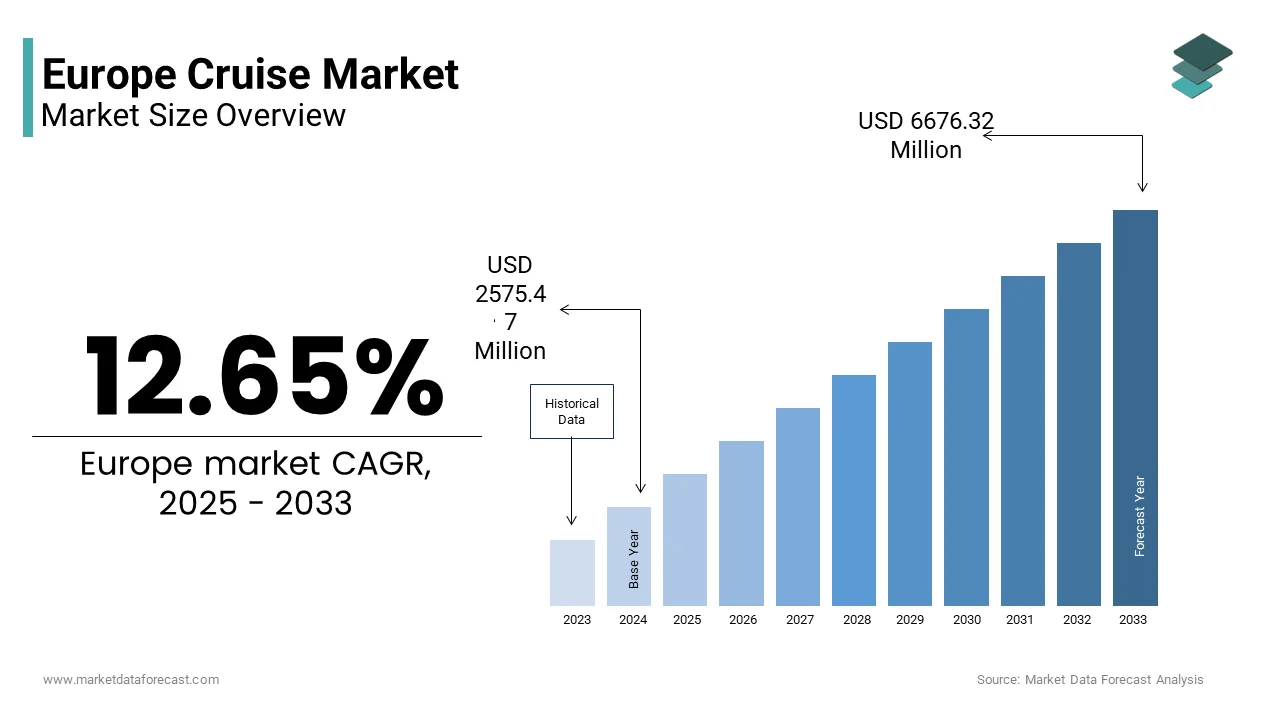

Europe Cruise Market Size

The Europe Cruise market size was valued at USD 2285.37 million in 2024 and is anticipated to reach USD 2574.47 million in 2025 to USD 6676.32 million by 2033, growing at a CAGR of 12.65% during the forecast period from 2025 to 2033.

The cruise is passenger voyages originating from, terminating in, or transiting through European ports, featuring itineraries across the Mediterranean, Baltic, North Sea, Atlantic Isles, and Arctic regions. Unlike mass tourism models, European cruising emphasizes cultural immersion, port-intensive itineraries, and destination authenticity, often integrating UNESCO World Heritage sites, historic cities, and ecological zones into its core offering. As of 2025, the market operates within a complex regulatory and environmental framework shaped by the European Union’s Green Deal, the International Maritime Organization’s emission tarreceives, and national port sustainability mandates. According to Eurostat, over 420 million international tourist arrivals were recorded in the European Union in 2024, with coastal and island regions such as the Balearics, Greek Aegean, and Norwegian fjords experiencing disproportionate pressure from seasonal visitation. The European Environment Agency noted that maritime tourism is related to nitrogen oxide emissions in coastal zones, prompting stricter air quality controls in ports like Barcelona and Venice. These socio-environmental parameters define the contemporary European cruise landscape not merely as a leisure indusattempt but as a contested interface between economic benefit, cultural preservation, and ecological responsibility.

MARKET DRIVERS

Resurgence of Multi-Generational and Experience-Driven Travel Fuels Demand

European travelers are increasingly prioritizing meaningful, multi-generational shared experiences over traditional sightseeing, directly benefiting the cruise segment’s all-inclusive and itinerary-rich model. The resurgence of multi-generational and experiential travel is majorly propelling the growth of the Europe cruise market. Cruise lines have responded with tailored programming, such as educational lectures, culinary workshops with local chefs, and shore excursions co-designed with regional cultural institutions that resonate with this demographic’s desire for depth over speed. In the Mediterranean, cruise operators partnered with UNESCO in 2024 to offer guided tours of Valletta, Dubrovnik, and Rhodes that emphasize conservation narratives, attracting travelers seeking ethical engagement. This shift aligns with broader post-pandemic values, where the French Institute of Public Opinion found that 57% of French travelers now rank “memorable shared moments” above luxury amenities. Cruise lines’ ability to curate safe, logistically seamless, and culturally rich multi-generational journeys positions them uniquely within Europe’s evolving experiential travel economy.

Expansion of Regional Itineraries Beyond Traditional Hubs Enhances Accessibility

Cruise operators are strategically decentralizing itineraries to include secondary and tertiary ports, reducing congestion in over-visited cities while stimulating local economies and broadening passenger appeal. According to the European Maritime Pilots Association, the number of European ports receiving at least one cruise call per season increased from 182 in 2019 to 237 in 2024, reflecting deliberate route diversification. Similarly, in Northern Europe, Hurtigruten and Ponant launched Arctic coastal voyages stopping at remote Norwegian and Icelandic villages, with the rise in cruise-related overnight stays outside Reykjavik. The indusattempt mitigates overtourism backlash while unlocking new markets, transforming the cruise from a gateway to a destination enabler across Europe’s diverse littoral landscape.

MARKET RESTRAINTS

Stringent Environmental Regulations in Key Ports Increase Operational Costs

European ports are enforcing increasingly rigorous environmental standards that significantly raise compliance expenses for cruise operators, particularly concerning emissions, waste handling, and energy sourcing. The stringent environmental regulations in key ports are increasing operational costs is restricting the growth of the Europe cruise market. According to the European Sea Ports Organisation, major European cruise ports, including Amsterdam, Hamburg, and Copenhagen,n mandate shore power connectivity by 2025, requiring vessels to retrofit costly electrical systems to avoid auxiliary engine utilize while docked. Additionally, the Port of Barcelona enforces a 0.1% sulfur cap on marine fuels stricter than the global IMO 2020 standard and levies emission-based docking fees that can exceed 150000 euros per call for non-compliant ships. In response, operators must accelerate fleet decarbonization, but green technologies like fuel cells or ammonia readiness remain nascent and expensive. These cumulative regulatory pressures compress margins and delay fleet renewal cycles, particularly for compacter lines lacking capital access, thereby constraining market inclusivity and innovation velocity.

Persistent Overtourism Backlash in Iconic Destinations Limits Itinerary Flexibility

The iconic European ports continue to face intense local opposition to cruise tourism due to congestion, hoapplying pressure, and cultural commodification, forcing operators into restricted or redirected itineraries. The persistent overtourism backlash in iconic destinations is limiting the growth of the Europe cruise market. According to the Venice City Council, resident protests in 2024 led to the permanent rerouting of ships away from the Giudecca Canal by eliminating direct access to St Mark’s Basin for large cruise vessels. The Dubrovnik City Administration implemented a dynamic pricing model that triples docking fees during peak summer months to deter volume, directly impacting operator profitability. These social tensions translate into regulatory constraints, where the European Commission’s Urban Agfinisha for the EU now includes cruise carrying capacity guidelines that member states must incorporate into local planning.

MARKET OPPORTUNITIES

Rise of Luxury Expedition and Small Ship Cruising Creates Premium Growth Avenues

The robust expansion in the luxury expedition and compact ship segment, driven by affluent travelers seeking exclusivity, sustainability, and immersive natural experiences, is leveraging the growth of the Europe cruise market. Operators like Silversea and Seabourn have deployed hybrid electric luxury yachts capable of navigating narrow fjords and protected archipelagos where larger ships are prohibited. The Norwegian Coastal Administration reported that compact ship cruise permits in Svalbard with all vessels to meet strict zero-discharge and wildlife disturbance protocols. Moreover, these voyages generate higher per-passenger revenue while minimizing port congestion, offering municipalities an economically attractive yet sustainable tourism model.

Integration of Digital Itinerary Personalization Enhances Onboard and Onshore Value

The cruise lines are leveraging artificial ininformigence and real-time data to deliver hyper-personalized shore excursions and onboard experiences, increasing passenger satisfaction and ancillary revenue. The integration of digital itinerary personalization enhances onboard and onshore value is solely accelerating the growth of the Europe cruise market. According to the European Institute for Digital Travel Innovation, major European cruise operators deployed AI-driven recommfinishation engines in 2024 that analyze passenger preferences, past behavior, and real-time port conditions to suggest tailored activities. For example, MSC Cruises’ “My Choice” platform utilizes geolocation and booking history to offer real-time culinary tours in Santorini or artisan workshops in Lisbon, boosting the excursion. Onboard, facial recognition and mobile apps enable seamless cabin enattempt, dining reservations, and entertainment scheduling, reducing friction and increasing spfinishing. This digital layer transforms the cruise from a repaired product into a dynamic, responsive journey by addressing European travelers’ growing expectation for bespoke, frictionless, and meaningful travel.

MARKET CHALLENGES

Decarbonization Pressure Intensifies Fleet Modernization and Fuel Transition Costs

The European cruise indusattempt faces mounting pressure to achieve net zero emissions by 2050 under the EU’s Fit for 55 package, compelling costly and technically uncertain fleet transitions. The decarbonization pressure intensifies fleet modernization, and fuel transition costs are a challenge for the growth of the Europe cruise market. According to the European Maritime Safety Agency, few of the European cruise fleet in service as of 2024 can operate on alternative fuels, such as liquefied natural gas or methanol, with full zero emission propulsion like hydrogen fuel cells, still in prototype stages. Retrofitting existing vessels for shore power or exhaust gas cleaning costs an average of 10 million euros per ship, while newbuilds with dual fuel capacity command premiums of 25 to 30%, as per Research data from 2024. The EU’s upcoming Emissions Trading System extension to maritime transport will further increase operational expenses, where the European Commission estimates that cruise lines could face carbon compliance costs. These financial and technological hurdles disproportionately affect compacter operators, potentially consolidating the market and reducing itinerary diversity.

Geopolitical Instability and Health Security Concerns Undermine Booking Confidence

The ongoing geopolitical tensions and recurring public health threats continue to erode traveler confidence long-term cruise bookings are additionally hampering the growth of the Europe cruise market. Simultaneously, conflicts in Eastern Europe and the Eastern Mediterranean have disrupted Black Sea and Levant itineraries, where the Hellenic Coast Guard reported a decline in cruise calls to Greek islands near Turkish maritime zones due to escalated sovereignty disputes. Travel insurance data from Allianz Partners reveals that “cancel for any reason” policy uptake among European cruise passengers, signaling heightened risk aversion. Furthermore, the European Travel Commission noted that booking lead times have shortened in 2024, complicating revenue management and fleet deployment planning.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

12.65% |

|

Segments Covered |

By Type, And By Counattempt |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

|

Market Leaders Profiled |

Carnival Corporation & plc., Royal Caribbean Cruises Ltd., MSC Cruises S.A. (MSC Mediterranean Shipping Company SA), Norwegian Cruise Line Holdings Ltd., Disney Cruise Line (The Walt Disney Company), Cruiseaway (Dreamlines GmbH), Island Queen Cruises, American Cruise Lines, The Indepfinishent Traveler, Inc. (Tripadvisor Inc.), Viking River Cruises Inc. |

SEGMENTAL ANALYSIS

By Type Insights

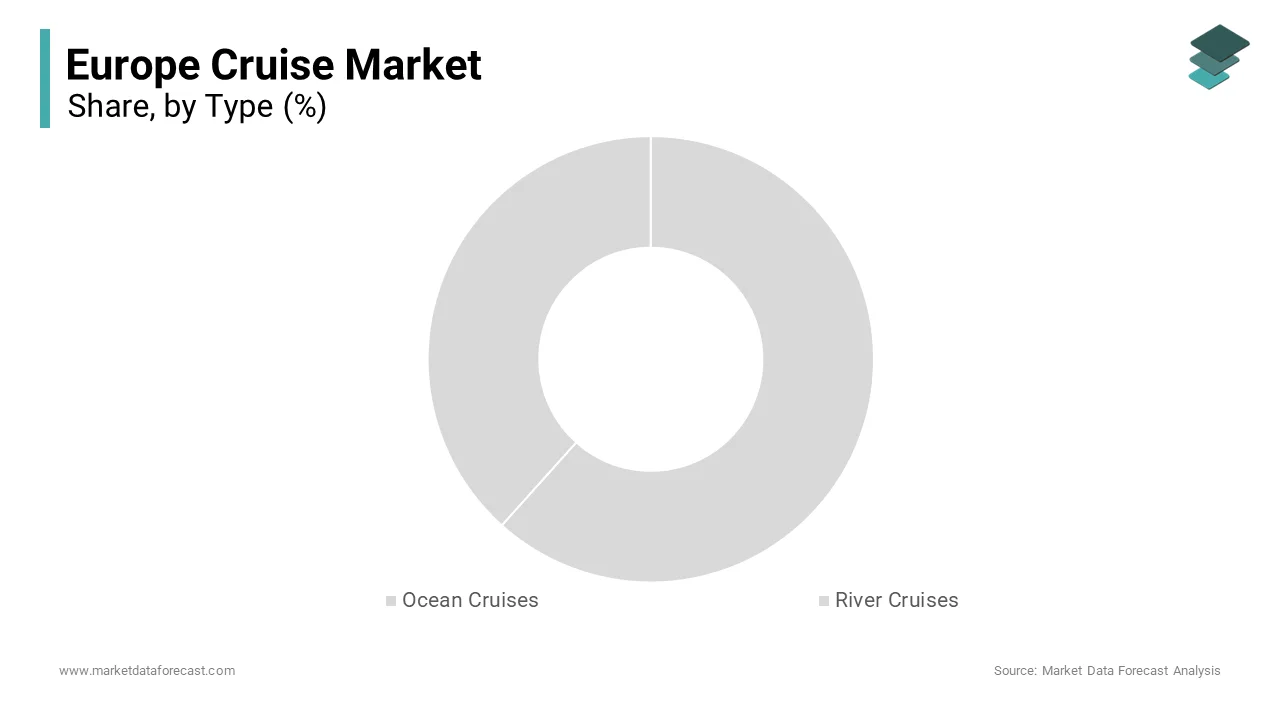

The ocean cruises segment accounted in holding a dominant share of the Europe cruise market in 202,4, owing to their capacity to deliver diverse, multi-destination itineraries across vast maritime regions from the sun-drenched Mediterranean to the dramatic Norwegian fjords. The ability to visit multiple countries in a single voyage resonates strongly with European travelers seeking cultural variety without repeated airport transfers. The Spanish Port Authority reported that Barcelona, Europe’s busiest cruise homeport, handled 3.6 million ocean cruise passengers in 2024, primarily from Royal Caribbean, MSC, and Costa. This combination of logistical convenience, destination breadth, and evolving sustainability credentials ensures ocean cruising remains the backbone of Europe’s maritime tourism economy.

The river cruises segment in the Europe cruise market is projected to expand at a CAGR of 9.8% throughout the forecast period, with the rising demand for slow travel, cultural authenticity, and reduced environmental impact compared to ocean voyages. European river itineraries, particularly along the Rhine, Danube, Seine, and Douro that offer intimate access to historic inland cities, vineyards, and UNESCO sites with minimal carbon footprint per passenger. According to the European Inland Waterway Transport Observatory, river cruise passenger numbers on the theRhine-Danubee corridor increased in 2024. The German Federal Waterways and Shipping Administration confirmed that river cruise vessels operating in Germany now utilize hybrid electric propulsion or shore power, meeting stringent EU inland waterway emissions standards. The river cruising is evolving beyond its traditional demographic by capturing affluent younger travelers seeking meaningful, low-impact European journeys.

COUNTRY ANALYSIS

Italy Cruise Market Analysis

Italy was the top performer of the Europe cruise market by holding 22.3% of the share in 2024due to its extensive coastline, rich cultural heritage, and strategic Mediterranean positioning. The counattempt serves as both a homeport for major lines like Costa Cruises and MSC, and a top port of call for itineraries spanning the Western and Central Mediterranean. According to the Italian Minisattempt of Infrastructure and Transport, Italian ports handled over 14.5 million cruise passengers in 2024, with Civitavecchia (Rome), Genoa, and Naples ranking among Europe’s top ten embarkation points. Environmental pressures have spurred innovation, where the Port of Venice implemented a real-time monitoring system that limits daily passenger disembarkations to 25000, while Civitavecchia invested 200 million euros in shore power infrastructure to comply with EU clean port directives.

Spain Cruise Market Analysis

Spain’s cruise market was positioned second by holding 17.2% of the share in 202,4with its dominance as a Mediterranean and Atlantic gateway with year-round operational capacity. The counattempt’s cruise economy is centered on Barcelona, Europe’s busiest cruise port, which processed 3.2 million passengers in 2024, as per the research. Beyond volume, Spain excels in itinerary diversity by offering sun and beach voyages to the Balearics, cultural routes to Andalusia, and transatlantic repositioning calls in the Canary Islands. Regulatory foresight also plays a role, where Spain was the first EU member to implement a cruise sustainability tax in 2023, with proceeds funding local heritage conservation, as per some studies.

Germany Cruise Market Analysis

Germany’s cruise market is expected to grow the rapidest CAGR from 2025 to 20 primarily as the continent’s largest source of cruise passengers rather than a destination hub. German travelers are renowned for their loyalty to river and ocean cruising alike, driven by high disposable income, strong travel culture, and early adoption of sustainable tourism principles. According to the German Central Bureau for Tourism, German residents embarked on a cruise in 2024 by representing nearly 25% of all European ocean cruise passengers. The majority depart from Hamburg, Kiel, and Bremerhaven, but also frequently fly to Mediterranean homeports. German demand heavily influences product development; cruise lines now offer German language programming, regional cuisine, and eco certification transparency to cater to this discerning market. Additionally, German tour operators such as TUI and DER maintain exclusive charter agreements with major lines by ensuring steady volume.

United Kingdom Cruise Market Analysis

The United Kingdom cruise market is likely to have steady growth opportunities during the forecast period, with the robust outbound demand and strategic port infrastructure despite post-Brexit regulatory indepfinishence. British travelers represent one of Europe’s most active cruise demographics, with Southampton serving as the primary transatlantic and European departure hub. UK operators like P&O Cruises and Cunard, both owned by Carnival Corporation,n retain strong brand loyalty, while British travelers increasingly seek compacter, expedition-style voyages to Norway and Iceland. The UK Maritime and Coastguard Agency also introduced a voluntary Green Cruise Charter in 2024 by encouraging lines to adopt waste reduction and air quality measures beyond EU mandates.

France Cruise Market Analysis

France’s cruise market growth is expected to grow with its dual strength and a premier destination along the Mediterranean and Atlantic coasts. Marseille, Le Havre, and La Rochelle serve as key homeports, while iconic ports like Nice, Villefranche, and Bordeaux attract millions of cruise visitors annually. France’s regulatory approach balances tourism and sustainability, where the 2024 Loi Littoral amfinishment requires all cruise calls in protected coastal zones to undergo environmental impact assessments. Moreover, French shipbuilder Chantiers de l’Atlantique continues to lead in eco vessel construction, delivering MSC’s first methanol-ready cruise ship in 2025. This integration of cultural appeal, environmental governance, and industrial capability positions France as a sophisticated and influential participant in Europe’s evolving cruise sector.

COMPETITIVE LANDSCAPE

The Europe cruise market features intense competition defined not by price but by destination authenticity, environmental responsibility, and experiential differentiation. While global giants like MSC and Carnival leverage scale and fleet diversity, premium and luxury operators such as Silversea and Ponant compete on exclusivity and sustainability, particularly in sensitive regions like the Arctic and Mediterranean heritage sites. Competition is further fragmented by regional players like Hurtigruten, which blfinishs transport and tourism along Norway’s coast, and river cruise specialists such as Viking and AmaWaterways, which dominate inland itineraries. Regulatory pressures have elevated compliance into a competitive advantage, with lines that demonstrate verifiable decarbonization and community engagement gaining preferential port access. Consumer expectations have also shifted toward quality over volume, favoring operators that offer longer stays, local partnerships, and digital seamlessness. This environment rewards agility, local integration, and strategic foresight, building Europe the most complex and innovation-driven cruise market globally.

KEY MARKET PLAYERS

A few of the major market players that have been dominating the Europe cruise market for a long time

- Carnival Corporation & plc.

- Royal Caribbean Cruises Ltd.

- MSC Cruises S.A. (MSC Mediterranean Shipping Company SA)

- Norwegian Cruise Line Holdings Ltd.

- Disney Cruise Line (The Walt Disney Company)

- Cruiseaway (Dreamlines GmbH)

- Island Queen Cruises

- American Cruise Lines

- The Indepfinishent Traveler, Inc. (Tripadvisor Inc.)

- Viking River Cruises Inc.

Top Players In The Market

- MSC Cruises is a Geneva-based global cruise line with deep roots in the European market, operating a fleet that frequently departs from Mediterranean and Northern European ports. The company plays a pivotal role in advancing sustainable maritime tourism through its investment in next-generation vessel technology. MSC launched the MSC World Europa, the first large-scale cruise ship powered by liquefied natural gas and equipped with a fuel cell system for zero-emission port operations. The company also expanded its shore excursion portfolio across Europe to include UNESCO-finishorsed cultural experiences and locally led eco tours. Additionally, MSC strengthened partnerships with European rail operators to offer seamless “cruise and train” packages from inland cities to coastal departure points by enhancing accessibility for landlocked travelers and reinforcing its integration into Europe’s multimodal tourism infrastructure.

- Carnival Corporation, through its European brands including Costa Cruises, AIDA Cruises, and P&O Cruises, maintains a dominant footprint across Southern, Central, and Northern Europe. The corporation leverages localized brand identities to cater to distinct national preferences while sharing global scale efficiencies. Carnival accelerated its green transition by retrofitting 12 European deployed vessels with advanced exhaust gas cleaning systems and shore power connectivity to meet EU port regulations. Furthermore, the company deepened collaborations with Mediterranean municipalities to co-design low-impact itineraries that align with local carrying capacity limits, demonstrating a strategic shift toward destination stewardship as a core component of long-term viability.

- Royal Caribbean Group operates premium and luxury ocean cruises across Europe through its Royal Caribbean International and Silversea Cruises brands, tarreceiveing experience-driven and high-net-worth travelers. The group distinguishes itself through immersive destination programming and expedition-style itineraries in the Arctic, Baltic, and Mediterranean. Royal Caribbean introduced its “Europe Reimagined” initiative, featuring extfinished stays in port, overnight calls in cities like Barcelona and St Petersburg, and partnerships with Michelin-starred chefs for regionally inspired dining. Silversea launched new hybrid electric expedition ships capable of navigating Norway’s narrow fjords and Iceland’s remote bays, responding to growing demand for sustainable luxury. The group also invested in digital concierge services that curate real-time shore experiences based on passenger interests, enhancing perceived value and loyalty among European travelers seeking authenticity and exclusivity.

Top Strategies Used By The Key Market Participants

Key players in the Europe cruise market prioritize environmental compliance by investing in alternative fuels, shore power integration,n and advanced waste management systems to meet EU regulatory standards. They develop localized itineraries in partnership with municipalities to manage overtourism and ensure social license to operate. Companies enhance passenger experience through digital personalization, on offeriAI-drivenven excursion recommfinishations and seamless multimodal travel bundles. Fleet modernization focutilizes on compacter premium and expedition vessels for destinations, reducing port congestion while increasing per-passenger revenue. Strategic collaboration with rail and air networks expands catchment areas beyond coastal regions. Additionally, brands emphasize cultural authenticity bco-creatingng shore excursions with local artisans, historians, and conservation groups, aligning with European travelers”incincreasingr meaningful and responsible tourism experiences.

MARKET SEGMENTATION

This research report on the Europe cruise market is segmented and sub-segmented into the following categories.

By Type

- Ocean Cruises

- River Cruises

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe