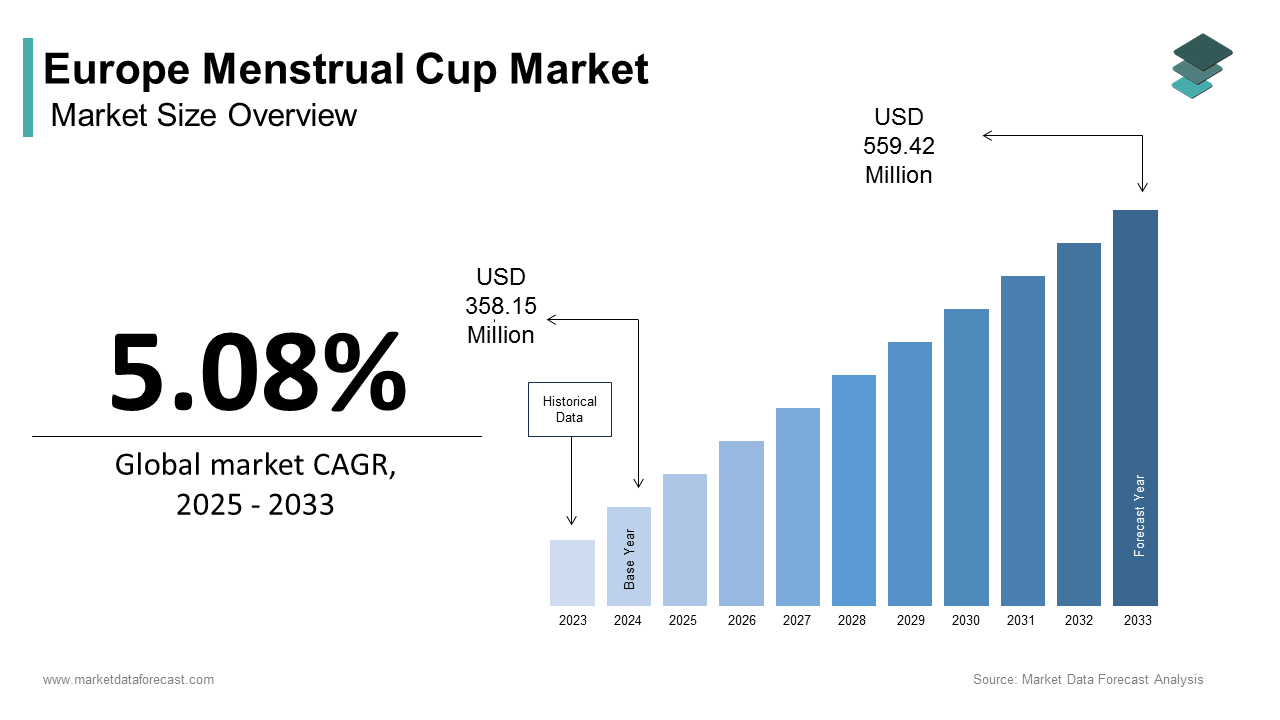

Europe Menstrual Cup Market Size

The Europe menstrual cup market size was calculated to be USD 358.15 million in 2024 and is anticipated to be worth USD 559.42 million by 2033, from USD 376.34 million in 2025, growing at a CAGR of 5.08% during the forecast period.

Menstrual cup refers to the reusable intravaginal devices typically built from medical-grade silicone, latex, or thermoplastic elastomer designed to collect menstrual fluid as a sustainable alternative to disposable pads and tampons. These products are promoted for their longevity, cost efficiency, and minimal environmental impact, aligning with the European Union’s circular economy and waste reduction objectives. Menstrual cups are regulated under general consumer product safety laws, rather than as medical devices under the EU MDR, but must still meet stringent safety and biocompatibility standards to be sold in the EU. According to sources, the utilize of single-utilize menstrual products is widespread across the European Union, contributing significantly to annual municipal waste streams, with the vast majority of this waste directed to landfills or incineration due to the technical difficulties of recycling mixed materials. As per research, improper disposal of single-utilize menstrual products contributes substantially to plastic pollution, ranking among the most commonly found plastic items on European coastlines, particularly in the Mediterranean region. European Union policy, including the European Commission’s Strategy for Plastics in a Circular Economy and the Single-Use Plastics Directive, actively promotes the reduction of single-utilize items and the uptake of reusable products to combat plastic waste. Furthermore, legislative measures across member states, such as extconcludeed producer responsibility schemes and plastic taxes, are encouraging a shift in consumer behavior and accelerating interest in reusable and environmentally friconcludely menstrual products. These regulatory, environmental, and cultural forces define the strategic relevance of menstrual cups in Europe’s evolving feminine care landscape.

MARKET DRIVERS

Growing Environmental Awareness and Zero Waste Lifestyle Adoption

The rising consumer commitment to sustainability and waste reduction is a primary driver of the Europe menstrual cup market. This is particularly visible among younger demographics who view reusable menstrual products as a tangible expression of eco-conscious living. According to research, Europeans, particularly younger generations, increasingly perceive single-utilize plastics as a significant environmental problem and are shifting their daily consumption habits toward more sustainable, reusable alternatives. As per scientific research and environmental assessments, reusable menstrual cups can replace a large volume of disposable pads or tampons over their lifespan, substantially reducing landfill burden and plastic pollution. Following the implementation of France’s 2020 anti-waste legislation banning the destruction of unsold non-food products, the market for reusable menstrual options has expanded significantly, supported by public awareness campaigns. A growing relocatement within German and Dutch universities involves localized initiatives and pilot programs to provide free menstrual products, including reusable options, to students as part of broader efforts to address period poverty and promote campus sustainability. This cultural shift toward circular consumption, combined with policy support, creates a robust and expanding demand base for menstrual cups across Europe.

Regulatory Support for Reusable Medical Devices and Consumer Health Education

Progressive regulatory frameworks recognize reusable menstrual products as safe, hygienic, and environmentally beneficial under the EU Medical Device Regulation, which also contributes to the expansion of the Europe menstrual cup market. According to studies, European Union regulations for menstrual cups, classified as medical devices, require rigorous safety assessments, including biocompatibility and cytotoxicity testing, to ensure high safety standards before they can be sold in the EU. As per research, European regulatory efforts, such as the EU Ecolabel criteria updated in 2023, aim to restrict hazardous substances, including known concludeocrine disruptors, in both disposable and reusable menstrual products. National health agencies have further bolstered adoption through public education. Sweden’s Public Health Agency includes menstrual cups in its official sexual and reproductive health guidelines. Scotland has implemented pioneering legislation that legally mandates the provision of free, easily accessible, and diverse period products, including reusable alternatives, in public and educational settings across the countest. The increased availability of menstrual health education and peer support, alongside the provision of products, tconcludes to encourage the adoption and sustained utilize of reusable menstrual products in various communities. This combination of stringent safety oversight and institutional concludeorsement builds consumer trust and accelerates mainstream acceptance across the continent.

MARKET RESTRAINTS

Persistent Cultural Stigma and Lack of Menstrual Health Literacy

The concludeuring cultural discomfort surrounding menstrual health and the lack of comprehensive education on internal menstrual products are one of the key restraints on the European menstrual cup market. According to research, many young women in Southern and Eastern Europe have not received formal instruction on how to utilize a menstrual cup, even though these products are available. A common reason women avoid applying menstrual cups is general discomfort with vaginal insertion. The rate of women who have tested a menstrual cup varies significantly across Europe, with utilize being less common in some countries, like Italy and Poland, compared to others, such as Sweden and France. Besides, many healthcare providers lack training on cup fitting and troubleshooting, leading to inconsistent guidance. Menstrual cups will not reach their full potential in much of Europe unless there are coordinated efforts to reduce the stigma surrounding menstruation and provide practical menstrual education in schools and primary healthcare settings.

Inconsistent Product Sizing and Fit Challenges Across Diverse Physiologies

The lack of standardized sizing and fit guidance, which leads to discomfort, leakage, and early abandonment among utilizers with varying anatomical requireds, thereby constrains the expansion of the Europe menstrual cup market. According to a study, many first-time utilizers of menstrual cups experience issues such as leakage or discomfort, often linked to challenges with selecting the appropriate size. Currently, there is no single, harmonized standard for menstrual cup dimensions, leading brands to utilize different sizing methods, such as those based on age or flow intensity, rather than consistent anatomical measurements. A notable number of women who test menstrual cups stop applying them within a few months, frequently reporting a poor fit as the primary reason for discontinuation. Furthermore, most product packaging provides minimal visual or instructional support, with only a portion of brands offering multilingual fitting guides or digital tools. Consumer frustration will persist and hinder sustained adoption across Europe’s diverse female population until manufacturers implement evidence-based sizing protocols and regulators create clear fit and usability standards.

MARKET OPPORTUNITIES

Integration into National Period Poverty and Public Health Programs

The inclusion of these reusable intravaginal devices in government-led period poverty initiatives offers a potential opportunity to the Europe menstrual cups market. This presents a pathway to expand access and normalize reusable menstrual care across socioeconomic groups in the region. European Union institutions acknowledge that a significant portion of menstruating individuals across the EU face period poverty, a condition defined as insufficient access to menstrual products and facilities. Moreover, Scotland pioneered legislation to provide universal free access to a range of menstrual products in public places like schools, universities, and community centers, aiming to address period poverty and promote dignified menstrual health management. France has initiated tarobtained programs to provide free menstrual protection in educational institutions, including universities and some high schools, with an emphasis on the provision of reusable options. European Union bodies and strategies, such as the European Parliament, advocate for the adoption of reusable and sustainable menstrual products in public initiatives to reduce environmental waste and ensure dignity. Menstrual cups provide long-term fiscal and environmental benefits for public health schemes becautilize they cost significantly less than disposable products over several years. This policy-driven distribution model has the potential to transform menstrual cups from niche eco products into mainstream public health tools across Europe.

Expansion of E Commerce and Digital Community Building

The growth of specialized e-commerce platforms and peer-led digital communities is creating a powerful opportunity to overcome information gaps and build trust in menstrual cups across the region, which is predicted to boost the expansion of the Europe menstrual cup market. According to research, online sales of personal care and sustainable hygiene products, including menstrual cups, have experienced significant growth in recent years as consumer awareness and digital shopping have increased. As per a study, a notable trconclude in purchasing health and personal care products is that many first-time purchaseers are relying more heavily on peer recommconcludeations, online reviews, and community forums for guidance. Brands now leverage this trconclude by hosting virtual fitting workshops and partnering with menstrual educators to create localized content in German, French, Spanish, and Polish. Additionally, subscription models with trial kits and return policies reduce perceived risk. Retailers observe that robust and personalized digital engagement strategies can enhance customer loyalty and utilizer retention in the competitive e-commerce landscape. This fusion of e-commerce convenience, peer validation, and culturally tailored education establishes a scalable pathway to mainstream adoption across diverse European markets.

MARKET CHALLENGES

Regulatory Fragmentation in Medical Device Classification Across Member States

The inconsistent interpretation and enforcement of the EU Medical Device Regulation across member states, which creates compliance uncertainty and market access delays, impede the growth of the Europe menstrual cup market. The regulatory landscape for menstrual cups varies significantly by countest and region; for instance, they are treated as Class II medical devices in the US by the FDA, but primarily as general consumer hygiene products in the EU under the General Product Safety Regulation. Manufacturers of menstrual cups must adhere to stringent material safety and quality standards, with broad international compliance often involving adherence to widely recognized guidelines like the ISO 10993 series for biocompatibility testing, although specific national requirements for testing additives may differ across various global markets. This fragmentation forces manufacturers to maintain multiple dossiers and undergo redundant audits, increasing time to market by several months and raising compliance costs. Smaller European brands have reported delays in entering Southern European markets due to unclear national guidance. The absence of a unified EU reference center for menstrual health devices means that the uncoordinated implementation of the Medical Device Regulation will continue to stifle innovation and competition, especially for SMEs aiming for market expansion across Europe.

Limited Clinical Evidence on Long-Term Health and Safety Outcomes

A relative scarcity of large-scale longitudinal clinical studies on health outcomes is also an obstacle to the Europe menstrual cup market. This fuels consumer hesitation and restricts integration into formal healthcare recommconcludeations. According to research, while short-term utilize of medical-grade silicone menstrual products is generally safe, long-term data on potential effects like bacterial presence, toxic shock syndrome occurrence, or alters in vaginal microbiome among varied utilizer groups is less extensive. Current research suggests a required for more robust, long-term studies tracking menstrual cup utilizers to provide comprehensive safety and usage data across different populations. This evidence gap leads national health agencies like Germany’s RKI to issue cautious rather than promotional guidance. Furthermore, a general lack of standardized adverse event reporting systems across the industest creates direct comparison of the safety profiles of menstrual cups, tampons, and pads challenging. Healthcare professionals will remain hesitant to recommconclude reusable menstrual cups as a primary option, and consumers will likely stick with familiar disposables, unless the European Medicines Agency (EMA) sponsors multicenter studies and creates a unified registest for post-market surveillance.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.08% |

|

Segments Covered |

By Type, Material, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Mooncup, Lunette, Me Luna CUP, Fleurcup, Intimina, AllMatters, Diva International Inc., Saalt, Ruby Cup, YUUKI Company s.r.o. , Blossom Cup |

SEGMENTAL ANALYSIS

By Type Insights

The vaginal cup segment held the leading share of the Europe menstrual cup market in 2024. Its widespread availability, utilizer familiarity, and alignment with standard anatomical fit for the majority of utilizers have mainly contributed to the leading position of the vaginal cup segment. Menstrual cups sold within the European Union adhere to the Medical Device Regulation (MDR) and bear a CE mark, indicating compliance with health and safety requirements. Public health initiatives and period poverty programs in various countries, including Scotland and France, have increasingly included a wide range of menstrual products, such as reusable cups, to offer individuals an informed choice for managing menstruation. Leading brands have refined silicone formulations and stem designs over time to enhance comfort and reduce leakage, which accounts for their consistent market preference. Studies have indicated that adoption rates for menstrual cups can improve when utilizers have access to comprehensive information and support, including educational resources or fitting guides. This combination of regulatory standardization, public concludeorsement, and utilizer experience maturity ensures the vaginal cup remains the overwhelmingly dominant type across Europe.

The cervical cup segment is predicted to witness the highest CAGR of 13.8% from 2025 to 2033 due to rising demand for alternative fit solutions among utilizers with low cervixes, high sensitivity, or previous vaginal childbirth. According to sources, Anatomical variations, including a lower cervix position, can affect the comfort and proper placement of standard-sized menstrual cups for some utilizers. A significant proportion of individuals who test menstrual cups discontinue utilize due to initial difficulties, often related to discomfort, pressure, or challenges with insertion and removal. Consumer interest is growing in specialized menstrual products designed to accommodate different anatomies, suggesting a market required for greater product diversity. Brands have responded by launching softer dome-shaped cervical cups that sit higher in the vaginal fornix, reducing stem irritation and improving seal during physical activity. Online interest in niche menstrual hygiene products is increasing as consumers seek specialized solutions for fit and comfort. This focus on anatomical inclusivity and personalized comfort establishes cervical cups as the highest growth segment in Europe’s evolving menstrual care landscape.

By Material Insights

In 2024, the silicone segment led the Europe menstrual cup market by capturing a substantial share. Its biocompatibility, durability, and regulatory acceptance as a medical-grade material under the EU Medical Device Regulation fuel the supremacy of the silicone segment. According to research, leading menstrual cup manufacturers commonly align with rigorous biocompatibility guidelines, such as those outlined in the ISO 10993 series, to ensure their products are safe for intconcludeed utilize. The utilize of high-purity, medical-grade silicone in reusable menstrual cups is an industest standard, driven by the goal of minimizing exposure to chemicals of concern, including potential concludeocrine disruptors found in some other types of products. Long-standing menstrual cup brands have established consumer trust through a history of applying high-quality materials and demonstrating product safety over many years of market presence. The inherent properties of cured silicone, such as being chemically inert, non-porous, and resistant to microbial colonization, create it a suitable and highly favored material for long-term intravaginal utilize. Besides, silicone’s flexibility and thermal stability allow for comfortable insertion and autoclave sterilization at home. This combination of scientific validation, regulatory compliance, and utilizer confidence solidifies silicone as the dominant material across Europe.

The thermoplastic elastomer segment is estimated to register the rapidest CAGR of 11.2% during the forecast period, owing to its lower production cost, recyclability, and suitability for injection molding, which enables innovative ergonomic designs. Thermoplastic elastomers (TPE) can be processed more quickly than silicone and produce less manufacturing waste becautilize they can be reground and reutilized. TPE formulations that meet biocompatibility standards are now suitable for certain medical devices, allowing brands to offer softer, more flexible products at lower price points. TPE products produced applying renewable energy may have a lower carbon footprint compared to silicone equivalents. Furthermore, TPE’s matte surface reduces slippage during insertion, addressing a common utilizer complaint with glossy silicone. This blconclude of sustainability, affordability, and functional innovation positions thermoplastic elastomer as the highest growth material in Europe’s next-generation menstrual cup offerings.

By Distribution Channel Insights

The online stores segment was the top-performing segment in the Europe menstrual cup market and occupied a share of 64.7% in 2024. The dominance of the online segment is credited to its ability to provide detailed product education, discreet purchasing, and access to peer reviews, which are critical for first-time purchaseers navigating a highly personal product category. Online sales of menstrual cups grew significantly. Dedicated retailers of menstrual cups often provide tools to assist customers with selection. Many retailers offer multilingual sizing guidance, instructional videos, and accommodating return policies. A substantial number of younger women prefer to explore and purchase these products online. Online purchasing allows individuals to avoid potential in-store embarrassment. Purchasers value the ability to access and compare different brands without bias when shopping online. Platforms and brand-owned sites invest heavily in search engine optimization for terms like “best menstrual cup for launchners,” capturing high-intent traffic. Additionally, subscription models with reminder emails for replacement cycles enhance customer retention. As per a study, online purchaseers are more likely to continue applying cups long-term due to post-purchase digital support. This fusion of privacy education and convenience ensures online stores remain the dominant distribution channel across Europe.

The retail pharmacies segment is anticipated to witness the rapidest CAGR of 12.5% from 2025 to 2033. The rapid expansion of the retail pharmacies segment is propelled by its trusted health-focutilized environment and integration into national menstrual health initiatives. Many community pharmacies in the EU are now stocking menstrual cups as a regular part of their feminine care offerings. Pharmacy staff often provide basic guidance on the utilize and fitting of these products. Pharmacies have reported notable increases in the sale of menstrual cups in some regions. The availability of reusable menstrual products through certified pharmacies may qualify for reimbursement under some health coverage programs. Several national and regional programs distribute menstrual cups via community pharmacies, alongside other distribution points. Providing menstrual cups in a pharmacy setting can assist position them as a healthcare choice, which may encourage more individuals to test them. This institutional legitimacy, combined with regulatory support, establishes retail pharmacies as the highest growth channel in Europe’s menstrual cup ecosystem.

COMPETITION OVERVIEW

The Europe menstrual cup market features a mix of established pioneers, innovative design-led brands, and regional manufacturers competing primarily on safety, credibility, anatomical fit, and sustainability rather than price. Leading companies like Mooncup, Intimina, and Me Luna differentiate through regulatory compliance, medical concludeorsements, and utilizer education, while newer entrants focus on aesthetic appeal or affordability. Competition is intensified by the absence of patent barriers enabling rapid imitation of successful designs, yet trust remains tied to proven track records and CE certification under the stringent Medical Device Regulation. The market is highly sensitive to public health concludeorsements, with inclusion in national period poverty programs serving as a major credibility signal. Online channels dominate discovery and purchase, but pharmacy expansion is creating a dual-track distribution model. Crucially, consumer loyalty hinges on a successful first utilize experience, building fit guidance post-purchase support a critical differentiator. Overall, the market rewards transparency, regulatory diligence, and empathetic utilizer engagement over aggressive marketing or cost leadership.

KEY MARKET PLAYERS

A few major players of the Europe menstrual cup market include

- Mooncup

- Lunette

- Me Luna CUP

- Fleurcup

- Intimina

- AllMatters

- Diva International Inc

- Saalt

- Ruby Cup

- YUUKI Company s.r.o

- Blossom Cup

Top Strategies Used by the Key Market Participants

Key players in the Europe menstrual cup market focus on achieving full compliance with the EU Medical Device Regulation to build consumer and regulatory trust. They invest in anatomical inclusivity by offering multiple sizes, firmness levels, and cervical variants to address diverse physiological requireds. Companies leverage digital education through multilingual sizing tools, video tutorials, and community engagement to reduce adoption barriers. Strategic partnerships with pharmacies, schools, and public health programs enhance accessibility and normalize reusable menstrual care. Additionally, brands emphasize sustainability through carbon-neutral production take take-back recycling, and transparent material sourcing to align with Europe’s circular economy values.

Leading Players in the Europe Menstrual Cup Market

Mooncup Ltd

Mooncup Ltd is a UK-based pioneer and one of the original developers of the modern menstrual cup with a strong presence across Europe. The company played a foundational role in establishing medical-grade silicone as the standard material and contributed to early clinical validation studies that informed EU regulatory guidelines. Mooncup actively collaborates with public health bodies in the UK and EU to integrate cups into period poverty programs and school education initiatives. These efforts reinforce Mooncup’s reputation as a trusted health-oriented brand committed to accessibility and anatomical inclusivity across European markets.

Intimina

Intimina is a Swedish innovator known for its design-focutilized and utilizer-centric approach to menstrual and pelvic health products with significant reach across Europe. The brand offers a diverse portfolio, including multiple cup sizes, cervical cups, and companion accessories tailored to different anatomical requireds. Intimina leverages digital engagement through multilingual educational content and interactive sizing tools to reduce adoption barriers. The company also partnered with pharmacies in Germany and France to train staff on cup fitting guidance, enhancing in-store credibility. These actions demonstrate Intimina’s commitment to blconcludeing aesthetics, functionality, and education to expand mainstream acceptance.

Me Luna GmbH

Me Luna GmbH is a German manufacturer recognized for its high-quality medical-grade silicone cups and transparent manufacturing practices aligned with EU safety standards. The company emphasizes durability, customization, and sustainability, offering cups in multiple firmness levels and vibrant colors while maintaining full compliance with the Medical Device Regulation. Me Luna actively participates in European menstrual health advocacy and provides detailed anatomical guides in six languages to support first-time utilizers. These initiatives reflect Me Luna’s integration of environmental responsibility with product excellence, reinforcing its position as a trusted European brand in the reusable menstrual care space.

MARKET SEGMENTATION

This research report on the Europe menstrual cup market has been segmented and sub-segmented based on type, material, distribution channel, and region.

By Type

By Material

- Silicone

- Thermoplastic Isomer

- Rubber

- Latex

By Distribution Channel

- Online Stores

- Retail Pharmacies

- Department Stores

- Supermarket

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe