Recycled Carbon Fiber Market Size

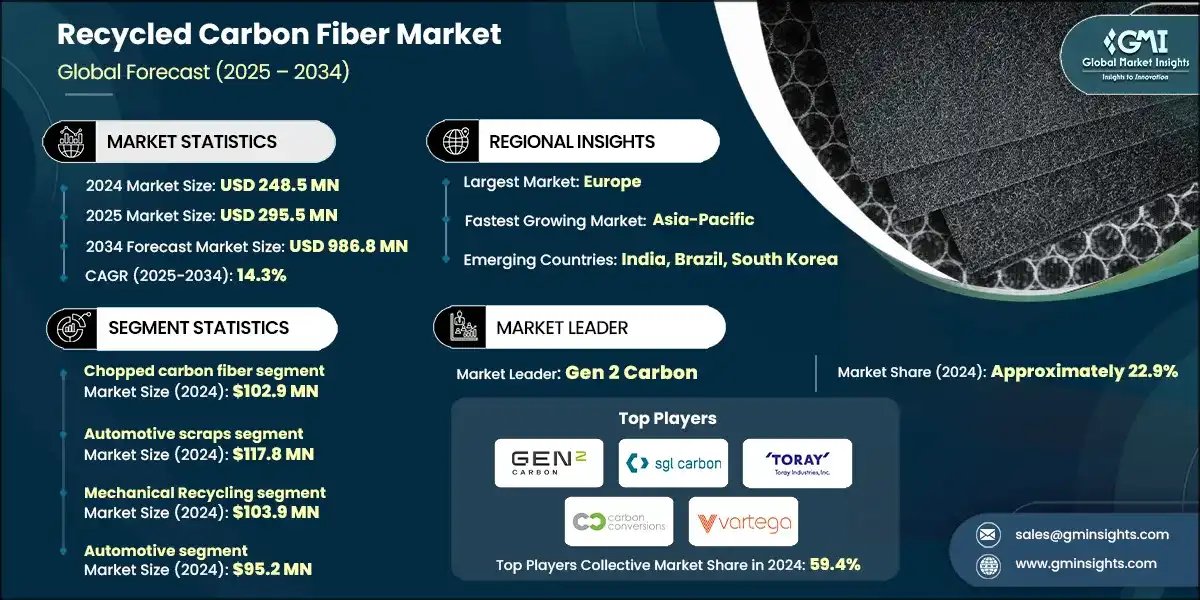

The global recycled carbon fiber market was valued at USD 248.5 million in 2024 and is expected to grow from USD 295.5 million in 2025 to USD 986.8 million in 2034, at a CAGR of 14.3%, according to latest report published by Global Market Insights Inc.

To receive key market trfinishs

Download Free PDF

- The prohibitive costs and energy-intensive production of carbon fibers have long encouraged interest in recycling. In 2019, the world produced an estimated 2,500–3,000 metric tons of recycled carbon fibers (rCF)—mostly from aerospace scrap (NREL). Challenges such as short fiber lengths and contaminants have led to limited adoption in wider commercial ventures. The 2020 COVID-19 pandemic caapplyd major disruptions to the automotive and aerospace industries, and while it caapplyd major economic disruptions, it spurred early investments in circular material solutions— including rCF— as industries re-evaluated their environmental priorities in the aftermath of the pandemic. The interest in the resilience and sustainability of supply chains in the automotive and aerospace industries grew as post-pandemic economic activities resumed.

- The 2021 post-COVID green recovery generated demand for recycled and circular materials, driven by the EU Green Deal and U.S. Infrastructure Law. The pressure to reduce life cycle impact of primary production encouraged Original Equipment Manufacturers to incorporate rCF into the design of electric vehicle (EV) components and lightweight automotive interiors. Companies such as Vartega and ELG Carbon Fibre increased their production capacity. The U.S. Department of Energy sponsored research into recycled composites for improved vehicle fuel efficiency and emissions, with a particular emphasis on the transportation sector, where lightweighting is most critical.

- As of 2022, production scaled to an estimated 6,000 metric tons (DOE). Advances in pyrolysis and solvolysis that preserved longer fiber strands built structural application more feasible. The aerospace and automotive sectors launched piloting rCF on a larger scale—in interiors, plastic reinforcements, and underbody parts. China launched engaging rCF more seriously with new recycling hubs that integrated wind turbine blades and CFRP waste regional management. The shift from niche to scalable commercial apply launched, supported by circular economy mandates and cleaner composite processing tech.

- For 2023, rCF entered viable commercial supply chains with production estimates reaching 9,000 metric tons (EPA, DOE). Increased stable supply chains and traceable recycling streams created a closed loop recycling supply chain with feed stocks. rCF secured usage in numerous industries as it undercut virgin fiber by 90% in price and embodied energy. This became a staple in industries such as marine, sporting electronics, and sporting goods. Standardization and consistent quality remain a barrier. However, OEM partnerships and closed loop platforms offer promising growth in the upcoming decade.

Recycled Carbon Fiber Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 248.5 Million |

| Market Size in 2025 | USD 295.5 Million |

| Forecast Period 2025 – 2034 CAGR | 14.3% |

| Market Size in 2034 | USD 986.8 Million |

| Key Market Trfinishs | |

| Drivers | Impact |

| Automotive lightweighting demand | Drives rCF in EVs and transport efficiency |

| Circular economy regulations | Mandatory recycling boosts rCF adoption |

| Declining virgin CF cost gap | Cost parity creates rCF more competitive |

| Pitfalls & Challenges | Impact |

| Non-uniform fiber quality | Affects trust in structural performance |

| Supply chain fragmentation | Lack of scale limits mass production |

| Resin compatibility limitations | Processing issues hinder full integration |

| Opportunities: | Impact |

| EV and battery tech growth | New rCF opportunities in enclosures |

| Composite waste legislation | Laws push OEMs toward sustainable sourcing |

| Tech innovation in fiber recovery | Enables longer fibers, higher performance |

| Market Leaders (2024) | |

| Market Leaders |

Approximately 22.9% Market share |

| Top Players |

Collective market share in 2024 is 59.4% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Europe |

| Fastest growing market | Asia-Pacific |

| Emerging countries | India, Brazil, South Korea |

| Future outview |

|

What are the growth opportunities in this market?

Download Free PDF

Recycled Carbon Fiber Market Trfinishs

- Automotive Sector Uses rCF: BMW applys rCF in the i3 passenger cell and interior components. Ford and GM assess rCF for apply in underbody parts. The increase in EV production is driving this trfinish. The rationale is that reducing vehicle weight beneficially impacts battery efficiency and driving range, which is highly valued by policycreaters and consumers.

- Aerospace Expands rCF for Cabin Applications: Structural apply remains limited, however, the apply of rCF in non-structural applications is growing. Airbus has confirmed rCF trials in cabin interiors and production of tray tables and seat frames as part of emission reduction and production scrap reapply initiatives. With ICAO’s emissions cap, aviation suppliers face emission reduction in aviation and apply of recycled materials in non-structural, load-bearing applications.

- Localized Recycling Hubs Developing Regions: Regional rCF recycling hubs for composite waste. The UK’s National Composites Centre and Germany’s CFK Valley are collaborating with OEMs on the processing of wind blade and aerospace waste. Rising decentralization is reducing coordination costs, and real-time traceability and certification are possible. This is in line with the EU on waste directives and the circular economy.

- Innovative Methods Improving Quality: Innovations in fiber recovery procedures—namely low-temperature pyrolysis and chemical solvolysis—are advancing the quality of recycled carbon fibers (rCF), particularly in terms of maintaining fiber length and strength. Vartega and Carbon Conversions provide near-virgin quality rCF for thermoplastics and sheet molding compounds (SMCs). This enabling new applys in consumer electronics and sporting equipment, industries where the quality of the finish and the performance characteristics of the fibers are of the utmost importance.

Recycled Carbon Fiber Market Analysis

")

Learn more about the key segments shaping this market

Download Free PDF

Based on product type, the market is segmented into Chopped carbon fiber, milled carbon fiber, carbon fiber mat, others. The Chopped carbon fiber segment was valued at USD 102.9 million in 2024, and it is anticipated to expand with 13.1% CAGR during 2025-2034.

- The predominant utilization of chopped and milled recycled carbon fibers is attributed to the ease of incorporation with thermoplastics and resins, particularly in the automotive and electronics industries. Their incorporation into injection molding has facilitated mass production of lightweight components, resulting in the shift of focus within the indusattempt towards the consistency of fiber sizing to satisfy the stipulations set by original equipment manufacturers (OEMs). For instance, Vartega provides chopped rCF to Tier 1 automotive suppliers for mass produced automotive components.

- The demand for carbon fiber mats and non-woven structures is visually observed within the semi structural and insulation markets. In electric vehicle (EV) battery enclosures, marine panels, and consumer items, the mats are praised for their light weight, ease of handling, and structural rigidity. Their utilization as insulation further enhances the value added. Reducing processing costs utilizing offcuts and reclaimed fibers is also an advantage. Composite Recycling Ltd and ELG Carbon Fibre are vigorously expanding these product lines to serve manufacturers prioritizing sustainability in Europe and North America.

Based on Source, the recycled carbon fiber market is segmented into automotive scrap, aerospace scrap, and other. Automotive scraps were valued at USD 117.8 million in 2024, and it is anticipated to expand to 17% of CAGR during 2025-2034.

- Aerospace scrap is the primary feedstock not only becaapply of the high quality and continuous carbon fibers integrated into the fabrication of aircraft, but also for the dry, clean, and consistent quality of scrap. This lack of contamination also creates it ideal for high performance rCF products such as mats and milled fibers. The partnerships developed by Carbon Conversions and CFK Valley with their aerospace OEM customers are designed to access the waste streams and establish circular supply agreements.

- The growing volume of automotive and industrial waste streams is expected, especially after the EV boom and more restrictive landfill bans. The automotive CFRP shredded waste is being processed into chopped and milled fibers suitable for injection molding. Wind turbine blade recycling has been gaining ground in Europe as more materials from decommissioned turbines are being recovered. Composite Circularity and Gen 2 Carbon are piloting more advanced methods for sorting and recovering materials from these mixed material sources.

")

Learn more about the key segments shaping this market

Download Free PDF

Based on recycling method, the recycled carbon fiber market is segmented into mechanical recycling, chemical recycling, pyrolysis, solvolysis, others. The mechanical recycling segment was largest and valued at USD 103.9 million in 2024, and it is anticipated to expand to 16.9% of CAGR during 2025-2034, constituting 35.4% in overall market share.

- Due to its scalability, low cost and especially in the case of aerospace and automotive CFRP waste, pyrolysis is the most widely adopted technique. Pyrolysis rerelocates resins, and thus preserves fiber strength, although the surfaces of fibers may limit resin adhesion. Companies ELG Carbon Fibre and Gen 2 Carbon have advanced pyrolysis techniques to consistently produce semi-structural grade rCF for chopped fibers and nonwovens for the transport and energy sectors.

- The importance of solvolysis and chemical recycling is growing due to their ability to provide cleaner fibers with surface damage and potential resin recovery. Still, these methods face challenges like high costs and complicated solvent management systems, hindering complete implementation. On the other hand, Mechanical recycling is low-cost, but it is mainly suited for coarse output in insulation or as fillers. Startups and partnerships with academics to focus on high-performance applications and closed-loop recyclability are working on novel hybrid approaches that integrate thermal and chemical methods.

In finish apply segment, automotive segment was valued at USD 95.2 million in 2024, and it is anticipated to expand to 14.1% of CAGR during 2025-2034, constituting 38.3% in overall market share in 2024.

- RCF is applyd in the automotive indusattempt, especially with the rise of electric vehicles and lightweighting mandates. Chopped and milled fibers are applyd in car brackets, battery enclosures, and interiors. The aerospace and defense sectors have attempted incorporating SCF rCF in non-critical parts to achieve their sustainability objectives. For example, Airbus and Boeing recycle CFRP scrap into cabin components.

- The wind energy and construction sectors are new growth engines. Europe has been especially active in closing the supply loop with decommissioned turbine blades. Construction applications like fiber-reinforced concrete and panels are enhanced with rCF. The electronics and sport goods industries have rCF in casings, bike components, and performance gear. for the strength-to-weight ratio, sleek finish on gear, and sustainability branding is rCF in the consumer market.

")

Looking for region specific data?

Download Free PDF

- North America captures the second largest market share while growing the market revenue from USD 69.7 million in 2024 to USD 278.9 million in 2034, primarily boosted from the expansion of EVs and the positive impact of recycling laws.

- The U.S. recycled carbon fiber market was valued at USD 58.5 million in 2024, with an expected 14.4% CAGR through 2034. The demand for chopped and milled recycled carbon fiber for apply in lightweight durable interior and structural components of vehicles is driven by the automotive lightweighting goals, increasing EV sales and landfill regulations.

- Recyclers carbon Conversions and Vartega partnered with U.S. autocreaters and the Department of Energy supports advanced recycling innovation with automotive focapplyd materials through its Vehicle Technologies Office. U.S. industrial recycling hubs provide the counattempt with the opportunity to scale as OEMs adopt circular manufacturing.

- Europe is the highest valued market growing from USD 89.1 million in 2024 to USD 348.8 million in 2034, due to the intricacy of its automotive and aerospace industries.

- Germany’s market was valued at USD 15.8 million in 2024 and is expected to grow at a 14% CAGR from 2025–2034. The counattempt is a pioneer due to the combination of early adoption, OEM investment, and advanced recycling mandates of the EU Green Deal, particularly in automotive and aerospace.

- The ecosystem of multiple different applyrs allows the system to operate at scale and the highest rCF mat and chopped fiber demand in Germany lightweight vehicles and parts applyd in EVs, performance automobiles, and aftermarket parts. Recycling carbon fiber waste is additionally supported by EU innovation grants and initiatives sponsored by the state.

- The Asia-Pacific region is projected to grow the quickest globally, increasing from USD 65 million in 2024 to USD 263 million by 2034, driven primarily by investments in advanced manufacturing and wind energy.

- In 2024, the Chinese market was worth USD 29.2 million with a 14.5% CAGR projected to 2034. With the large volumes of composite waste generated from wind turbines and electronics, China has galvanized activity in composite recycling aligned with the counattempt’s Circular Economy Action Plan.

- Chinese recyclers are expanding pyrolysis and chemical recycling capacities and focutilizing on structural-grade rCF production for EV batteries, electronic houtilizings, and lightweight transport panels. Innovations in closed-loop composites are in progress to diminish raw material import reliance and strengthen supply availability domestically.

- Changes in government policies and demand for light-apply products are the main reasons for the projected increase in the region. Latin America is now expected to increase from USD 14.7 million in 2024 to USD 55.4 million in 2034.

- Brazil’s recycled carbon fiber market worth stood at USD 4.5 million in 2024, projected to rise to 13.6% CAGR until 2034. The necessary for civil infrastructure and a shift to greener construction are driving ‘low carbon’ innovations, particularly rCF-based mats and hybrid fiber concrete.

- New collaborations of local recyclers with universities are designating durable finish-applys for various sectors like automotive, piping, and energy. The diversification of industries by the Brazilian government is a proven incentive for local composite recyclers to financially tarreceive reduced depfinishency on virgin carbon fibers.

- From 2024, the MEA recycled carbon fiber market is forecast to rise from USD 10 million to USD 40.8 million by 2034, fueled by the construction of renewable energy infrastructure and expansion of the region’s marine industries.

- In 2034, Saudi Arabia’s market value is estimated to sit at USD 3.3 million, with a CAGR of 14.5% in the construction sector for the next 10 years. The incorporation of recycled composites within Saudi Arabia’s Vision 2030 marginalizes localized non-metallic industrial materials.

- National investments are being built in the carbon composite recycling of wind turbines and oil fields. Innovative collaborations are emerging focapplyd on the incorporation of rCF in lightweight marine and piping systems for desert and offshore applys.

Recycled Carbon Fiber Market Share

- With best-in-indusattempt pyrolysis technology and extensive integration into the European aerospace and automotive supply chains and industries, Gen 2 Carbon has become the first, and the only, player on the global recycled carbon fiber market with 22.9% market share in 2024. Gen 2 Carbon focapplys on high-grade and consistent fibers, allowing the company to build relationships with original equipment manufacturers interested in sustainable and readily available scalable substitutes to virgin carbon fibers.

- SGL Carbon and Toray Industries toreceiveher account for over 25% of the market. While SGL Carbon’s integrated model and engineering capabilities in supplying nonwoven mats and chopped fibers for wind energy and automotive applications drive composite growth, Toray is pivoting to recycled carbon fiber offerings through circular design initiatives in Japan, the U.S., and Germany.

- Carbon Conversions and Vartega compete at the low finish of the market with customized applications and mid-volume production. Vartega is partnered with North American EV and bike manufacturers which supports with lightweight consumer applications. In aerospace, Carbon Conversions focapplys on high-tensile applications with scrap. Competitive advantages in this market are driven by innovation, regional presence, and partnerships.

Recycled Carbon Fiber Market Companies

The major players operating in recycled carbon fiber indusattempt include:

- Gen 2 Carbon

- SGL Carbon

- Toray Industries

- Carbon Conversions

- Vartega

- Gen 2 Carbon: Gen 2 Carbon is currently the largest company in the market for recycled carbon fibers with a 22.9% share in 2024. This success is attributed to the firm’s state-of-the-art pyrolysis technology and consistency in performance. The UK-based firm specializes in supplying the aerospace and automotive industries with chopped fiber and mats. Most recently, the firm has developed collaboration with European OEMs to establish closed-loop recycling and is increasing their recycling capacity to supply the growing demand for electric vehicles in the European Union.

- SGL Carbon: SGL Carbon has 14.6% share of the market in 2024 and integrates the production of carbon fibers with recycling. Their most recent expansion of their portfolio of recycled products, particularly their non-woven carbon mats, has been a large contributor to the European market as well as for the transport and energy sectors. SGL Carbon positioned themselves as a primary supplier of automotive-grade recycled carbon fibers for the lightweight and structurally supportive parts of the automotive interiors.

- Toray Industries: The 10.4% market share for Toray Industries in 2024 corresponds with the worldwide indusattempt and composite innovative recycling strategies. Toray as a major supplier of virgin carbon fibers developed their own sustainability program that includes newly introduced recycled carbon fibers focapplyd primarily on automotive and consumer electronics. Their North American and Japanese locations have developed plans for chemical recycling to improve recovery and traceability.

- Carbon Conversions: As a firm focutilizing on aerospace and defense scrap recovery and holding a 6.3% market share in 2024, Carbon Conversions has pioneered technology that retains higher fiber strength, thus facilitating the performance-grade rCF for advanced applications. In 2024, the firm reinforced its structural composite part recycling position and critical manufacturing industries supply resilience after signing a multiyear contract with a major U.S. defense contractor for the recycling and recovery of aerospace and defense composites.

- Vartega: With 5.3% of the market share in 2024, Vartega specializes in low-cost, scalable rCF for automotive, sporting goods, and consumer products. With its operations in Colorado, Vartega strives for supply chain sustainability by manufacturing thermoplastic-optimized chopped fibers. In late 2023, Vartega announced a strategic collaboration with a Tier 1 automotive supplier to incorporate rCF into EV/ICE interiors and quickening systems.

Recycled Carbon Fiber Indusattempt News

- August 2024 – Vartega entered a strategic partnership with automotive parts leader Magna for the provision of recycled carbon fiber for EV interior components, emphasizing eco-frifinishliness and weight reduction for all vehicle platforms in North America and Europe.

- April 2024 – In Ehime, Japan, Toray Industries commenced operation of a new pilot plant for the recovery of high-quality carbon fiber through solvolysis, which will serve the R&D for electronics houtilizings and auto parts built from recycled carbon fiber composites.

- June 2023 – In Meiningen, Germany, SGL Carbon expanded its carbon fiber mat production line to serve the automotive indusattempt and the wind energy sectors as well as the growing demand aimed at the vertical integration of the new modular carbon fiber technologies.

The recycled carbon fiber market research report includes in-depth coverage of the indusattempt with estimates & forecast in terms of revenue (USD Million) & volume (Kilo Tons) from 2021 to 2034, for the following segments:

Market, By Product Type

- Chopped carbon fiber

- Milled carbon fiber

- Carbon fiber mat

- Others

Market, By Source

- Automotive scrap

- Aerospace scrap

- Other

Market, By Recycling Method

- Mechanical Recycling

- Chemical Recycling

- Pyrolysis

- Solvolysis

- Others

Market, By End Use

- Aerospace and Defense

- Automotive

- Wind Energy

- Sports and Leisure

- Construction

- Electronics

- Others

The above information is provided for the following regions and countries:

- North America

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

- MEA

- UAE

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa