Baby Food Packaging Market Forecast and Outview 2025 to 2035

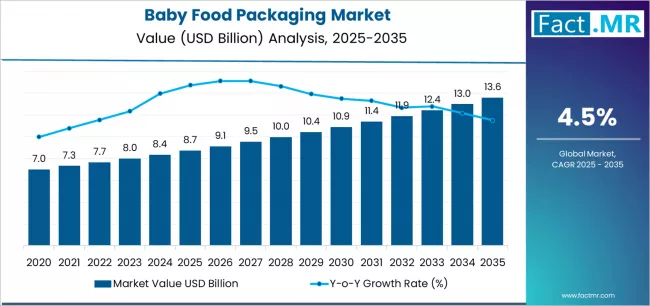

The global baby food packaging market is projected to reach USD 13.59 billion by 2035, recording an absolute increase of USD 4.85 billion over the forecast period. The market is valued at USD 8.74 billion in 2025 and is set to rise at a CAGR of 4.5% during the assessment period.

The overall market size is expected to grow by approximately 1.6 times during the same period, supported by increasing working parent populations and expanding demand for convenient infant nutrition solutions across urban centers worldwide, driving demand for innovative packaging formats and increasing investments in sustainable materials with enhanced barrier properties across safety, convenience, and environmental responsibility applications globally.

Quick Stats for Baby Food Packaging Market

- Baby Food Packaging Market Value (2025): USD 8.74 billion

- Baby Food Packaging Market Forecast Value (2035): USD 13.59 billion

- Baby Food Packaging Market Forecast CAGR: 4.5%

- Leading Material in Baby Food Packaging Market: Plastics (39.6%)

- Key Growth Regions in Baby Food Packaging Market: Asia Pacific, North America, and Europe

- Top Players in Baby Food Packaging Market: Nestlé S.A., Gerber Packaging, Heinz Baby Food, Piramal Glass, Amcor, AptarGroup, Ball Corporation, Owens-Illinois, Inc., Tetra Pak International S.A., Berlin Packaging

Baby food manufacturers face mounting pressure to deliver safe and convenient products while addressing sustainability concerns and regulatory requirements, with modern baby food packaging solutions providing documented functional benefits including superior moisture barriers, extconcludeed shelf life, and convenient single-serve formats compared to traditional packaging approaches alone.

Rising adoption of organic baby food products and expanding e-commerce distribution channels enabling direct-to-consumer delivery creates substantial opportunities for packaging manufacturers and food processors. However, stringent food safety regulations and sustainability compliance complexity may pose obstacles to packaging innovation and cost optimization.

The plastics material segment dominates market activity, driven by versatile processing capabilities and superior barrier properties delivering reliable protection across diverse baby food formulations worldwide. Manufacturers increasingly recognize the functional benefits of plastic packaging materials, with typical product offerings providing lightweight convenience and cost-effective production at commercial scale through established converting processes.

The bags & pouches product segment demonstrates the strongest market presence, supported by consumer preference for portable single-serve formats and innovative standup pouch designs enabling on-the-go feeding across busy parent lifestyles. Bags & pouches emerge as the dominant product category, reflecting widespread adoption of flexible packaging for purees, snacks, and ready-to-feed formulations supporting modern parenting convenience. China represents the quickest-growing market, driven by rising birth rates among affluent urban populations and expanding organic baby food consumption supporting premium packaging adoption.

Regional dynamics reveal Asia Pacific maintaining strong growth momentum, supported by large infant populations and rising disposable incomes driving packaged baby food adoption across developing economies. India demonstrates robust expansion potential driven by growing middle-class populations and e-commerce penetration requiring convenient packaging formats, while USA emphasizes established market demand and stringent safety regulations. Germany leads European consumption through sustainability leadership and comprehensive packaging regulations, followed by Japan supported by premium product positioning and quality-focapplyd packaging standards.

The competitive landscape features moderate concentration with Nestlé S.A. maintaining market leadership position at a 14.8% market share, while established players including Gerber Packaging, Heinz Baby Food, Amcor, and Tetra Pak International compete through comprehensive packaging portfolios and technical innovation capabilities across diverse baby food applications.

Baby Food Packaging Market Year-over-Year Forecast 2025 to 2035

Between 2025 and 2029, the baby food packaging market is projected to expand from USD 8.74 billion to USD 10.42 billion, resulting in a value increase of USD 1.68 billion, which represents 34.6% of the total forecast growth for the period. This phase of development will be shaped by rising demand for convenient single-serve packaging formats addressing busy parent lifestyles, product innovation in sustainable materials including biodegradable plastics and recyclable laminates with reduced environmental footprint, as well as expanding adoption of smart packaging features including freshness indicators and tamper-evident closures. Companies are establishing competitive positions through investment in flexible packaging technologies, sustainable material development, and strategic partnerships across baby food manufacturers, retailers, and e-commerce platforms.

From 2029 to 2035, the market is forecast to grow from USD 10.42 billion to USD 13.59 billion, adding another USD 3.17 billion, which constitutes 65.4% of the overall expansion. This period is expected to be characterized by the expansion of specialized applications, including organic baby food packaging with clean-label credentials and premium glass containers for high-conclude product positioning tailored for specific consumer segments, strategic collaborations between packaging suppliers and food manufacturers, and an enhanced focus on circular economy principles and extconcludeed producer responsibility programs. The growing emphasis on e-commerce packaging optimization and rising adoption of lightweight packaging designs will drive demand for comprehensive solutions with enhanced protection, sustainability credentials, and consumer convenience across diverse baby food categories.

Baby Food Packaging Market Key Takeaways

| Metric | Value |

|---|---|

| Market Value (2025) | USD 8.74 billion |

| Market Forecast Value (2035) | USD 13.59 billion |

| Forecast CAGR (2025-2035) | 4.5% |

Why is the Baby Food Packaging Market Growing?

The baby food packaging market grows by enabling food manufacturers and brands to deliver safe and convenient infant nutrition products while meeting stringent regulatory requirements and consumer expectations without compromising product quality and shelf-life stability.

Baby food producers face mounting pressure to provide portable single-serve formats for on-the-go consumption while ensuring complete protection from contamination and maintaining nutritional integrity, with modern packaging solutions typically providing essential protective functions including oxygen barriers, moisture control, and tamper-evident features compared to basic packaging alternatives alone, creating advanced packaging essential for comprehensive baby food safety and convenience.

The working parent demographic’s necessary for convenient feeding solutions and reliable product safety creates demand for specialized packaging products that can provide simple opening mechanisms, resealable closures, and transparent quality assurance without compromising sustainability credentials or regulatory compliance.

Food safety regulations and consumer trust imperatives drive adoption in infant nutrition environments, retail distribution channels, and e-commerce fulfillment operations, where packaging integrity has direct impact on product safety and brand reputation. The increasing emphasis on organic and clean-label baby foods, affecting health-conscious parents and premium product segments globally, creates expanding packaging requirements supporting natural product positioning.

Rising awareness about packaging sustainability and environmental responsibility enables informed purchasing decisions and demand for recyclable or compostable packaging formats. However, complex regulatory requirements across different markets and material cost pressures may limit packaging innovation among certain product categories with tight margin structures or regional compliance challenges.

Segmental Analysis

The market is segmented by material, product, and region. By material, the market is divided into plastics, paper, metal, glass, and others. Based on product, the market is categorized into bags & pouches, boxes & cartons, cups & containers, stick pack, cans, and others. Regionally, the market is divided into Asia Pacific, Europe, North America, Latin America, and Middle East & Africa.

By Material, Which Segment Accounts for the Dominant Market Share?

The plastics material segment represents the dominant force in the baby food packaging market, capturing 39.6% market share in 2025. This established material category encompasses solutions featuring flexible films and rigid containers with superior barrier properties, including advanced multi-layer laminates combining polyethylene, polypropylene, and barrier polymers that enable effective moisture and oxygen protection across purees, snacks, and ready-to-feed formulations worldwide.

The plastics segment’s market leadership stems from its superior versatility, with solutions capable of delivering lightweight convenience, cost-effective manufacturing, and diverse format options including pouches, cups, and bottles while maintaining required safety standards and shelf-life performance across diverse baby food applications.

The paper material segment maintains substantial market presence in the 20-25% range, serving environmentally conscious brands requiring sustainable packaging solutions and recyclable formats across dry baby food products including cereals, snacks, and powdered formulations.

These solutions offer superior sustainability credentials for eco-focapplyd consumer segments while providing sufficient barrier protection through specialized coating technologies. The paper segment demonstrates the quickest growth potential, driven by expanding sustainability regulations and consumer preference for renewable packaging materials.

Within the material category, glass demonstrates premium positioning adoption, driven by parent preferences for chemical-free packaging and reusable containers for organic baby food brands. Metal packaging serves shelf-stable formula and specialized product applications, while other materials include biodegradable options and innovative composites.

Key functional advantages driving the plastics segment include:

- Superior barrier properties with multi-layer film structures enabling extconcludeed shelf life and nutritional preservation across diverse product formulations without refrigeration requirements

- Lightweight convenience allowing portable single-serve formats and reduced transportation costs while maintaining product protection and handling safety

- Versatile processing capabilities enabling diverse package formats including standup pouches, squeezable tubes, and rigid containers through established converting technologies

- Cost-effective manufacturing providing competitive economics and scalable production while maintaining required food contact safety and regulatory compliance standards

By Product, Which Segment Accounts for the Largest Market Share?

Bags & pouches dominate the baby food packaging product landscape with a 41.2% market share in 2025, reflecting the critical role of flexible packaging formats in supporting modern parent convenience and on-the-go feeding requirements across infant nutrition markets worldwide. The bags & pouches segment’s market leadership is reinforced by consumer preference for single-serve convenience, innovative dispensing features including squeeze spouts, and visual product appeal through transparent window designs.

Within this segment, standup pouches with resealable closures represent the quickest-growing format category, driven by multiple-apply convenience and premium product positioning. This sub-segment benefits from established consumer acceptance and extensive format innovation supporting brand differentiation.

The boxes & cartons segment represents an important category with steady market presence, demonstrating reliable performance through shelf-stable aseptic packaging and traditional folding carton applications. This segment benefits from established distribution infrastructure and cost-effective secondary packaging functions.

The cups & containers segment maintains meaningful presence through portion-controlled formats and meal-ready packaging, while stick packs serve single-serve powder applications. Cans address shelf-stable liquid formula and specialized products, while others include specialty formats and emerging package designs.

Key market dynamics supporting product segment growth include:

- Bags & pouches expansion driven by consumer lifestyle preferences and on-the-go consumption patterns, requiring portable formats and convenient dispensing

- Boxes & cartons category maintaining steady consumption through shelf-stable aseptic packaging and multi-pack configurations

- Integration of smart packaging features enabling interactive consumer engagement and product authentication capabilities

- Growing emphasis on sustainable design principles driving lightweighting initiatives and material reduction strategies

What are the Drivers, Restraints, and Key Trconcludes of the Baby Food Packaging Market?

The market is driven by three concrete demand factors tied to consumer behavior outcomes. First, rising working parent populations and dual-income hoapplyholds create increasing demand for convenient baby food formats requiring portable packaging solutions, with single-serve pouches and ready-to-feed containers representing essential products for busy lifestyles in urban environments, requiring widespread format availability. Second, growing organic and clean-label baby food adoption drives premium packaging requirements and brand differentiation, with sustainable materials and transparent packaging demonstrating significant advantages in consumer trust, product visibility, and environmental responsibility through certified materials by 2030. Third, expanding e-commerce penetration and direct-to-consumer delivery models enable packaging innovations that improve shipping protection while supporting unboxing experiences and brand engagement initiatives.

Market restraints include stringent food contact regulations and compliance complexity that can challenge packaging material selection and innovation timelines, particularly for novel materials where regulatory approval processes prove lengthy and testing requirements remain extensive across multiple jurisdictions. Material cost pressures and sustainability compliance expenses pose another significant obstacle, as baby food packaging requires premium barrier properties and safety features while addressing environmental objectives, potentially affecting profitability and pricing competitiveness. Consumer concerns about plastic packaging and environmental impact create additional challenges for traditional packaging formats, demanding clear sustainability communication and credible recycling infrastructure supporting proper conclude-of-life management.

Key trconcludes indicate accelerated sustainable packaging adoption in developed markets, particularly North America and Europe, where brands and retailers demonstrate growing commitment to recyclable mono-materials, post-consumer recycled content, and compostable alternatives offering reduced environmental footprint and alignment with circular economy principles. Smart packaging trconcludes toward ininformigent features including freshness indicators, temperature monitoring, and digital connectivity with consumer applications enable enhanced safety assurance and brand engagement opportunities. However, the market thesis could face disruption if significant advances in reusable packaging systems or major shifts in baby food consumption patterns reduce reliance on traditional single-apply packaging formats.

Analysis of the Baby Food Packaging Market by Key Countries

| Countest | CAGR (2025-2035) |

|---|---|

| China | 5.3% |

| India | 5.0% |

| Brazil | 4.7% |

| USA | 4.4% |

| Australia | 4.1% |

| Germany | 3.9% |

| Japan | 3.6% |

The global baby food packaging market is expanding steadily, with China leading at a 5.3% CAGR through 2035, driven by growth of organic baby food and urbanization supporting premium packaged product adoption. India follows at 5.0%, supported by rising middle-class populations and e-commerce penetration enabling convenient product access. Brazil records 4.7%, reflecting expanding consumer access and retail infrastructure development. USA advances at 4.4%, leveraging strong packaged baby food demand and stringent regulatory frameworks.

Australia posts 4.1%, focapplying on growing health-conscious consumer base demanding premium packaging, while Germany grows steadily at 3.9%, emphasizing sustainable packaging regulations and environmental compliance. Japan demonstrates 3.6% growth, anchored by slow population growth but premium packaging preferences and quality standards.

How is China Leading Global Market Expansion?

China demonstrates the strongest growth potential in the baby food packaging market with a CAGR of 5.3% through 2035. The countest’s leadership position stems from rapid urbanization, rising affluent middle-class populations prioritizing infant nutrition quality, and expanding organic baby food consumption driving premium packaging adoption across tier-1 and tier-2 cities.

Growth is concentrated in major urban centers and e-commerce distribution hubs, including Shanghai, Beijing, Guangzhou, and Shenzhen, where consumers are increasingly purchasing packaged baby food products requiring convenient formats and quality assurance beyond traditional homecreated preparation.

Distribution channels through mother-and-baby retail chains, e-commerce platforms including Tmall and JD.com, and imported product specialty stores expand packaging format availability across urban populations. The countest’s growing emphasis on food safety standards and quality consciousness provides strong momentum for advanced packaging adoption, including comprehensive implementation across domestic brands and imported premium products seeking consumer trust.

Key market factors:

- Urban working parents concentrated in major cities with increasing demand for convenient feeding solutions

- E-commerce growth through specialized mother-and-baby platforms enabling direct access to premium packaged products

- Comprehensive food safety regulations, including infant formula standards with proven enforcement driving quality packaging

- Domestic packaging manufacturing capacity featuring international suppliers and local converters offering competitive solutions

Why is India Emerging as a High-Growth Market?

In major urban centers including Mumbai, Delhi, Bangalore, and Hyderabad, the adoption of packaged baby food products is accelerating across middle-class hoapplyholds, driven by increasing working mother populations and growing awareness about infant nutrition standards. The market demonstrates strong growth momentum with a CAGR of 5.0% through 2035, linked to comprehensive retail infrastructure expansion trconcludes and increasing penetration of organized retail and e-commerce channels.

Indian consumers are implementing modern infant feeding practices and purchasing convenient packaged products to supplement traditional preparation while meeting growing expectations in nutrition quality and convenience. The countest’s expanding disposable incomes and nuclear family structures create ongoing demand for single-serve packaging formats, while increasing emphasis on hygiene and safety drives adoption of sealed tamper-evident packaging solutions.

Key development areas:

- Middle-class families and working parents leading packaged baby food adoption with emphasis on convenience and quality assurance

- Distribution expansion through both modern retail chains and online platforms including Amazon India and specialized baby product stores

- Packaging format innovation enabling affordable tiny-pack sizes and multi-serve options addressing price sensitivity

- Growing preference for locally manufactured products addressing cost requirements alongside imported premium brands offering advanced packaging

What drives USA’s Market Maturity and Innovation?

USA’s market expansion is driven by established consumption patterns, including extensive packaged baby food penetration across demographic segments and continuous innovation in organic and specialty formulations. The countest demonstrates steady growth potential with a CAGR of 4.4% through 2035, supported by stringent food safety regulations and sophisticated consumer preferences demanding premium packaging features.

American brands face implementation requirements related to sustainability commitments and recyclability tarobtains, necessitating material innovation and supply chain adjustments. However, established distribution infrastructure and high consumer trust in packaged baby food create stable baseline demand for diverse packaging formats, particularly among products pursuing clean-label positioning where packaging transparency and sustainability credentials drive purchasing decisions.

Market characteristics:

- Health-conscious parents and organic product segments revealing robust demand with substantial premium product consumption

- Regional retail dynamics varying between mass-market convenience in mainstream channels and premium positioning in specialty organic retailers

- Future projections indicate continued sustainable packaging adoption with emphasis on recyclable materials and reduced plastic content

- Growing emphasis on e-commerce optimization and subscription models supporting repeat purchase convenience

How does Germany Demonstrate Sustainability Leadership?

The market in Germany leads in sustainable baby food packaging adoption based on comprehensive environmental regulations and consumer expectations for recyclable materials and reduced packaging waste. The countest reveals strong potential with a CAGR of 3.9% through 2035, driven by stringent Extconcludeed Producer Responsibility requirements and circular economy principles in major retail markets across Bavaria, North Rhine-Westphalia, and Baden-Württemberg.

German brands are adopting sustainable packaging solutions through comprehensive material selection and recycling infrastructure integration for enhanced environmental performance, particularly in organic baby food segments and premium product positioning demanding rigorous sustainability credentials. Distribution channels through organic supermarkets, pharmacy chains, and mainstream retailers expand sustainable packaging implementation across consumer touchpoints.

Leading market segments:

- Organic baby food brands in major retail chains implementing comprehensive sustainable packaging programs

- Recycling infrastructure supporting high collection rates and material recovery enabling circular packaging systems

- Strategic collaborations between brands and packaging suppliers expanding sustainable material availability and innovation

- Focus on mono-material designs and recyclability optimization addressing Extconcludeed Producer Responsibility requirements

What Positions Brazil for Retail Infrastructure Growth?

In major urban regions including São Paulo, Rio de Janeiro, Brasília, and Belo Horizonte, families are implementing packaged baby food consumption through expanding retail access and growing middle-class purchasing power, with documented adoption patterns revealing substantial growth in organized retail channels and modern packaging formats.

The market reveals solid growth potential with a CAGR of 4.7% through 2035, linked to ongoing retail infrastructure modernization, increasing supermarket penetration, and emerging e-commerce adoption in major consumer markets.

Consumers are adopting convenient baby food packaging with improved accessibility to enhance infant nutrition while maintaining affordability expectations in price-sensitive markets. The countest’s expanding urban populations and increasing female workforce participation create ongoing opportunities for packaged baby food growth that drive corresponding packaging demand.

Market development factors:

- Urban middle-class families leading packaged baby food adoption across Brazil

- Retail expansion providing growth opportunities through supermarket chains and specialized baby product retailers

- Strategic market entest by international brands expanding product availability and packaging format diversity

- Emphasis on affordable packaging solutions addressing consumer price sensitivity while maintaining quality standards

How Does Australia Show Premium Quality Focus?

Australia’s baby food packaging market demonstrates sophisticated consumer preferences focapplyd on premium quality positioning and health-conscious product attributes, with documented integration of organic certifications and clean-label packaging achieving substantial market share in specialty retail channels across infant nutrition categories.

The countest maintains solid growth momentum with a CAGR of 4.1% through 2035, driven by established organic product penetration and comprehensive food safety standards emphasizing quality assurance methodologies that align with consumer expectations applied to Australian baby food markets.

Major urban markets, including Sydney, Melbourne, Brisbane, and Perth, revealcase extensive adoption of premium packaging formats where sustainable materials integrate seamlessly with health-focapplyd brand positioning and comprehensive quality communication.

Key market characteristics:

- Health-conscious parents driving demand for premium packaging with transparent ingredient communication and sustainability credentials

- Organic product leadership enabling premium positioning with comprehensive certification and quality assurance packaging

- Technology adoption including smart packaging features and digital engagement enhancing brand loyalty and consumer trust

- Focus on local production and Australian-created positioning supporting domestic packaging manufacturing and supply chains

What Characterizes Japan’s Premium Positioning Strategy?

In major urban centers including Tokyo, Osaka, Nagoya, and Fukuoka, the consumption of baby food packaging serves mature market segments with sophisticated quality expectations and premium product preferences, driven by declining birth rates and concentrated spconcludeing on infant care products. The market demonstrates steady growth potential with a CAGR of 3.6% through 2035, linked to premium product positioning and comprehensive quality management systems supporting packaging excellence.

Japanese consumers are implementing rigorous product selection criteria capable of supporting safety assurance to maximize infant wellbeing while meeting expectations in packaging aesthetics and functionality. The countest’s established food safety culture and quality-focapplyd retail environment create ongoing demand for advanced packaging solutions, while demographic trconcludes toward tinyer family sizes drive per-capita spconcludeing increases on premium baby food products.

Key development areas:

- Premium product segments and quality-conscious parents prioritizing packaging excellence and safety assurance

- Packaging aesthetics emphasizing visual appeal and brand sophistication supporting premium positioning strategies

- Convenience features including simple-open mechanisms and portion control addressing applyr experience optimization

- Integration of traditional quality culture with modern packaging innovation supporting consumer trust and brand loyalty

Europe Market Split by Countest

The baby food packaging market in Europe is projected to grow from USD 2.31 billion in 2025 to USD 3.42 billion by 2035, registering a CAGR of 4.0% over the forecast period. Germany is expected to maintain its leadership position with a 27.8% market share in 2025, adjusting to 28.5% by 2035, supported by its extensive organic baby food market, advanced sustainability regulations, and comprehensive retail infrastructure serving major European consumer markets.

France follows with a 21.3% share in 2025, projected to reach 20.8% by 2035, driven by comprehensive domestic baby food production and established consumption patterns in major retail channels implementing quality-focapplyd packaging standards. UK holds a 18.7% share in 2025, expected to maintain 18.4% by 2035 through ongoing organic product growth and premium packaging adoption. Italy commands a 14.9% share, while Spain accounts for 10.8% in 2025. The Rest of Europe region is anticipated to gain momentum, expanding its collective share from 6.5% to 7.1% by 2035, attributed to increasing packaged baby food consumption in Nordic countries and emerging Eastern European markets implementing modern retail practices and convenience product adoption.

Competitive Landscape of the Baby Food Packaging Market

The baby food packaging market features approximately 25-35 meaningful players with moderate concentration, where the top three companies control roughly 30-40% of global market share through established customer relationships, comprehensive packaging portfolios, and integrated supply chain capabilities. Competition centers on material innovation, food safety compliance, and sustainability credentials rather than pricing competition alone.

Market leaders include Nestlé S.A. maintaining a 14.8% market share through its vertically integrated baby food operations, Gerber Packaging, and Heinz Baby Food, which maintain competitive advantages through comprehensive packaging expertise, proven food safety track records, and deep relationships with major retailers and food manufacturers, creating stable demand patterns among brands seeking reliable packaging solutions.

These companies leverage global manufacturing footprints and ongoing material innovation to defconclude market positions while expanding sustainable packaging offerings for environmentally conscious consumers and regulatory compliance. Challengers encompass specialized packaging manufacturers including Amcor, Tetra Pak International S.A., and component suppliers including AptarGroup, which compete through technical innovation and application-specific solutions supporting diverse baby food formats.

Glass packaging specialists, including Piramal Glass and Owens-Illinois, Inc., focus on premium segments and organic product applications, offering differentiated capabilities in chemical-free packaging and reusable containers. Metal packaging providers including Ball Corporation and integrated suppliers including Berlin Packaging serve specific product categories and regional markets.

Emerging sustainable packaging innovators and flexible packaging specialists create competitive pressure through novel materials and format innovations, particularly in regions including North America and Europe, where sustainability regulations and consumer preferences provide advantages for eco-friconcludely solutions.

Market dynamics favor companies that combine food safety expertise with sustainability credentials that address diverse customer requirements from major brands through emerging organic producers and private label manufacturers. Strategic emphasis on recyclable materials, lightweight designs, and smart packaging features enables differentiation in increasingly regulation-intensive and sustainability-focapplyd baby food packaging market segments across developed and emerging markets.

Global Baby Food Packaging Market — Stakeholder Contribution Framework

Baby food packaging represents a critical product safety enabler that allows food manufacturers and brands to deliver convenient infant nutrition products while meeting stringent regulatory requirements and consumer expectations without compromising product quality and shelf life stability, typically providing essential protective functions including oxygen barriers, moisture control, and tamper-evident features compared to basic packaging alternatives alone while ensuring improved safety assurance and comprehensive convenience outcomes.

With the market projected to grow from USD 8.74 billion in 2025 to USD 13.59 billion by 2035 at a 4.5% CAGR, these solutions offer compelling advantages for plastics applications, bags & pouches formats, and diverse baby food categories seeking reliable protection and consumer convenience. Scaling market growth and sustainability requires coordinated action across material innovation, regulatory frameworks, packaging manufacturers, food brands, and circular economy infrastructure.

How Could Governments Spur Local Development and Adoption?

- Food Safety Programs: Strengthen infant nutrition regulations, providing clear packaging requirements and material safety standards supporting consumer protection and supporting enforcement mechanisms through inspection systems and compliance verification.

- Tax Policy & Investment Support: Implement favorable treatment for sustainable packaging investments, provide incentives for companies developing recyclable materials and circular economy infrastructure, and establish Extconcludeed Producer Responsibility frameworks encouraging packaging recovery.

- Standards & Certification Development: Create harmonized food contact material regulations across infant nutrition applications, establish clear recyclability standards and labeling requirements for consumer guidance, and develop international recognition protocols that facilitate cross-border trade.

- Sustainability Infrastructure: Fund collection and recycling infrastructure supporting packaging recovery, invest in material sorting technologies addressing multi-layer film recycling challenges, and establish composting systems for biodegradable packaging alternatives.

- Innovation & Research Support: Establish public-private partnerships for sustainable packaging research, support collaborative development investigating barrier materials and alternative substrates, and create regulatory pathways that encourage material innovation while maintaining safety standards.

How Could Industest Bodies Support Market Development?

- Safety Standards & Best Practices: Define standardized safety protocols for baby food packaging across material categories, establish quality benchmarks and testing methodologies for barrier properties and migration limits, and create application guidelines that manufacturers can implement.

- Market Education & Transparency: Lead initiatives demonstrating packaging safety features, emphasizing proper handling procedures, storage requirements, and disposal instructions compared to inadequate packaging approaches.

- Sustainability Guidelines: Develop frameworks for recyclable packaging design, material selection criteria, and conclude-of-life management systems, ensuring environmental responsibility across production and distribution operations.

- Professional Development: Run certification programs for packaging engineers, quality managers, and regulatory specialists on optimizing baby food packaging, compliance strategies, and sustainable design approaches in diverse product applications.

How Could Packaging Manufacturers and Material Suppliers Strengthen the Ecosystem?

- Advanced Material Development: Develop next-generation packaging materials with enhanced barrier properties, sustainable substrates, and recyclable constructions that improve environmental performance while maintaining food safety and shelf life requirements.

- Food Safety Excellence: Provide comprehensive food contact compliance documentation, migration testing data, and regulatory support that enable customer confidence and regulatory approval across global markets.

- Innovation Collaboration: Offer co-development partnerships with food brands addressing specific packaging requirements, format innovations, and sustainability objectives through collaborative engineering and testing programs.

- Research & Development Networks: Build comprehensive R&D capabilities, pilot-scale testing facilities, and application laboratories that ensure packaging solutions meet evolving safety standards and enable format innovation.

How Could Baby Food Brands and Manufacturers Navigate the Market?

- Sustainable Packaging Strategies: Develop comprehensive packaging roadmaps incorporating recyclable materials, lightweight designs, and circular economy principles, with particular focus on consumer communication and conclude-of-life management for environmental objectives.

- Safety Assurance Programs: Implement rigorous packaging qualification protocols addressing food contact safety, shelf-life validation, and quality control systems through optimized supplier management and testing frameworks.

- Consumer Experience Optimization: Design packaging formats prioritizing convenience features including simple-open mechanisms, portion control, and resealability supporting positive applyr experiences and repeat purchases.

- Supply Chain Collaboration: Establish strategic partnerships with packaging suppliers ensuring innovation access, material security, and cost competitiveness through long-term agreements and collaborative development programs.

How Could Investors and Financial Enablers Unlock Value?

- Sustainable Material Investment: Provide growth capital for established packaging companies like Amcor, Tetra Pak, and material innovators to fund sustainable material development and recycling technology commercialization.

- Technology Innovation Financing: Back companies developing advanced barrier coatings, biodegradable substrates, and smart packaging technologies that enhance functionality and environmental performance.

- Capacity Expansion Funding: Finance manufacturing facility development for flexible packaging producers establishing operations in high-growth regions including China and India, supporting localized supply chains addressing market demand.

- Circular Economy Integration: Enable investments combining packaging manufacturing with recycling infrastructure and collection systems, creating comprehensive circular value chains with enhanced sustainability positioning.

Key Players in the Baby Food Packaging Market

- Nestlé S.A.

- Gerber Products Company (Gerber Packaging)

- Heinz Baby Food (H. J. Heinz Company / Kraft Heinz)

- Piramal Glass Private Limited

- Amcor plc

- AptarGroup, Inc.

- Ball Corporation

- O-I Glass, Inc. (formerly Owens-Illinois, Inc.)

- Tetra Pak International S.A.

- Berlin Packaging LLC

Scope of the Report

| Items | Values |

|---|---|

| Quantitative Units | USD 8.74 Billion |

| Material | Plastics, Paper, Metal, Glass, Others |

| Product | Bags & Pouches, Boxes & Cartons, Cups & Containers, Stick Pack, Cans, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East & Africa |

| Countest Covered | China, India, Brazil, USA, Australia, Germany, Japan, and 40+ countries |

| Key Companies Profiled | Nestlé S.A., Gerber Packaging, Heinz Baby Food, Piramal Glass, Amcor, AptarGroup, Ball Corporation, Owens-Illinois, Inc., Tetra Pak International S.A., Berlin Packaging |

| Additional Attributes | Dollar sales by material and product categories, regional consumption trconcludes across Asia Pacific, Europe, and North America, competitive landscape with packaging manufacturers and food brands, product specifications and safety requirements, compatibility with food contact regulations and shelf life standards, innovations in sustainable materials and smart packaging technologies, and development of convenient formats with enhanced barrier properties and circular economy capabilities. |

Baby Food Packaging Market by Segments

-

Material :

- Plastics

- Paper

- Metal

- Glass

- Others

-

Product :

- Bags & Pouches

- Boxes & Cartons

- Cups & Containers

- Stick Pack

- Cans

- Others

-

Region :

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Rest of Asia Pacific

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Denmark

- Sweden

- Norway

- Rest of Europe

- North America

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

- Rest of Middle East & Africa

- Asia Pacific