In 2024-25, financing activity in India’s energy sector expanded in both depth and scale, with record disbursements by Power Finance Corporation Limited (PFC), REC Limited and the Indian Renewable Energy Development Agency (IREDA). Equity markets, too, played a hugeger role, with several initial public offerings (IPOs) and qualified institutional placements (QIPs), reflecting growing investor appetite. International participation expanded significantly, with large multilateral packages, bilateral loans and private acquisitions in the clean energy segment. On the policy side, higher budreceiveary allocations accelerated the roll-out of flagship schemes and the rationalisation of Goods and Services Tax (GST) on renewable equipment focapplyd on creating a more enabling environment.

Power Line takes a see at the key trconcludes and developments in the power financing segment over the past year…

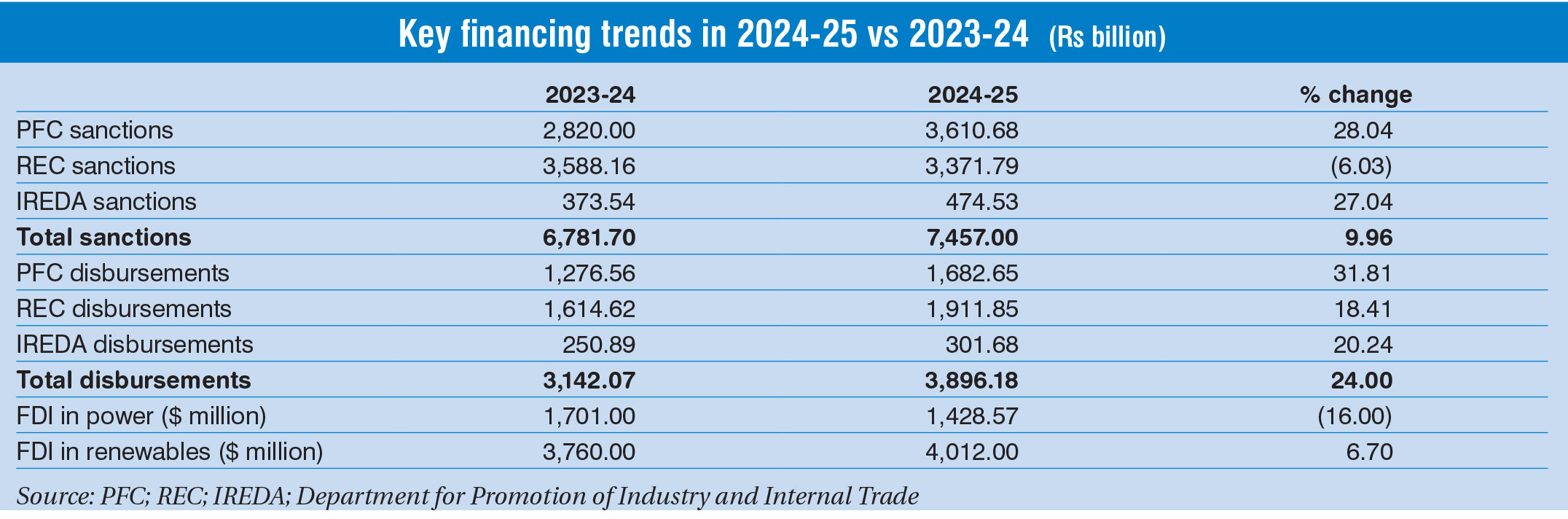

Debt market trconcludes

The cumulative disbursements by REC, PFC and IREDA stood at Rs 3,896.18 billion in 2024-25, recording a growth of more than 24 per cent over the Rs 3,142.07 billion registered in the previous year. Cumulative sanctions grew by 9.96 per cent, from Rs 6,781.7 billion in 2023-24 to Rs 7,457 billion in 2024-25.

- REC: On a year-on-year basis, REC’s disbursements rose by 18.41 per cent, reaching Rs 1,911.85 billion in 2024-25 compared to Rs 1,614.62 billion in 2023-24. In terms of sanctions, REC registered a decline of 6.03 per cent, from Rs 3,588.16 billion in 2023-24 to Rs 3,371.79 billion in 2024-25. Its renewable loan book stood at Rs 579.94 billion as of March 2025, a year-on-year growth of 49 per cent, with renewable energy disbursements growing by 63 per cent. In 2024-25, the company sanctioned Rs 896.32 billion towards conventional generation projects, Rs 1,052.59 billion towards renewable energy projects (including large hydro), Rs 850.4 billion towards transmission and distribution projects, Rs 432.39 billion towards infrastructure and logistics projects, and Rs 140.09 billion as other loans, including short- and medium-term facilities.

- PFC: PFC’s disbursements increased by 31.81 per cent, from Rs 1,276.56 billion to Rs 1,682.65 billion during the same period. Its sanctions grew by 28.04 per cent, from Rs 2,820 billion to Rs 3,610.68 billion. The company’s renewable energy loan book has grown at a CAGR of 17 per cent over the past five years, more than doubling from Rs 289.8 billion in 2018-19 to Rs 810.31 billion in 2024-25. In the past year alone, it recorded a 35 per cent growth. During 2024-25, the company mobilised over Rs 1.11 trillion, of which 76 per cent was raised from the domestic market and 24 per cent through foreign currency borrowings, reflecting strong global investor confidence.

- IREDA: IREDA sanctioned Rs 474.53 billion in 2024-25, up 27.04 per cent from Rs 373.54 billion in the previous year, while disbursements increased by 20.24 per cent to Rs 301.68 billion from Rs 250.89 billion. Additionally, at the RE Invest 2024 conclave, IREDA pledged Rs 5 trillion in debt financing by 2030 to support the rapid growth of renewable energy. In March 2025, it issued perpetual Tier I green bonds worth Rs 12.47 billion at a coupon rate of 8.4 per cent per annum. In the same month, it issued 10-year Tier II green bonds worth Rs 9.1 billion at a coupon rate of 7.74 per cent per annum. Both issuances were privately placed with institutional investors and aimed at strengthening capital adequacy ratios. Further, IREDA’s approach suggests a shift from project-specific funding to integrating green-labelled instruments as part of its broader balance sheet management.

Public route

The Financial year 2025 saw notable equity market activity in the energy sector. In September 2025, Saatvik Green Energy Limited launched a Rs 9 billion IPO. In August 2025, Vikram Solar raised Rs 20.79 billion via an IPO, comprising a fresh issue of Rs 15 billion for capacity expansion and an offer for sale of Rs 5.79 billion by existing shareholders. In January 2025, Rajesh Power Services Limited raised Rs 1.6 billion through its IPO, consisting of 47.9 million equity shares with a face value of Rs 10 each, including 27.9 million fresh issue shares and 20 million shares under an offer for sale by existing shareholders.

NTPC Green Energy Limited built its stock market debut in November 2024, with a Rs 100 billion issue that drew strong investor interest, highlighting the growing appetite for renewable platforms backed by public sector majors. ACME Solar followed with a Rs 29 billion IPO, comprising a fresh issue worth Rs 23.95 billion and an offer for sale aggregating Rs 5.05 billion by ACME Cleantech Solutions.

Earlier, in October 2024, Waaree Energies’ IPO opened with a total issue size of Rs 43.21 billion. The IPO included a fresh issue worth Rs 36 billion and an offer for sale worth Rs 7.21 billion.

The pipeline remains robust, with companies such as Hero Future Energies, Avaada Energy, Inox Clean Energy, Emmvee Photovoltaic, Continuum Green Energy and Juniper Green Energy preparing sizeable public issues, expected to materialise later in the year.

The QIP route has also been active. In April 2025, Adani Energy Solutions Limited raised Rs 60 billion through a QIP, attracting strong global investor participation. In January 2025, Torrent Power Limited concluded its first-ever QIP, raising Rs 35 billion. The issue was oversubscribed nearly four times, attracting bids totalling about Rs 140 billion. In the same month, Kalpataru Projects International Limited successfully raised Rs 10 billion through a QIP.

IREDA has, meanwhile, received approval to raise about Rs 45 billion via a fresh equity issue, with the Government of India set to reduce its stake in the company by up to 7 per cent in one or more tranches.

Government support

Government support

The net budreceiveary allocation for the Minisattempt of Power (MoP) for 2025-26 stands at Rs 218.47 billion, up from Rs 205.02 billion in 2024-25. The Minisattempt of New and Renewable Energy has been allocated Rs 265.49 billion, compared to Rs 191 billion in the previous year.

Under the newly launched Nuclear Energy Mission, Rs 200 billion has been allocated for research and development of tiny modular reactors (SMRs). India has set a tarreceive of developing at least 100 GW of nuclear power capacity by 2047, with the aim of operationalising at least five indigenous SMRs by 2033.

As of August 2025, a total of Rs 1,306.36 billion has been sanctioned under the revamped distribution sector scheme (RDSS) for smart metering, while Rs 1,494.82 billion has been approved for loss reduction work.

For the battery energy storage system (BESS) segment, the government allocated Rs 960 million in 2024-25 for 1,000 MWh of BESS project under the viability gap funding (VGF) scheme, which was later revised to Rs 460 million as costs declined from Rs 9.6 million per MWh to Rs 4.6 million per MWh (30 per cent of capital cost). In June 2025, the MoP approved an additional VGF scheme for 30 GWh of BESS capacity, over and above the 13.2 GWh already in progress. This Rs 54 billion programme is expected to attract Rs 330 billion in investment and meet India’s BESS requirement by 2028.

In September 2024, the union cabinet approved a Rs 124.61 billion scheme (for the period 2024-25 to 2031-32) to support enabling infrastructure for hydropower projects above 25 MW and pumped storage projects (about 15,000 MW). Budreceiveary support is capped at Rs 10 million per MW (up to 200 MW) and Rs 2 billion plus Rs 7.5 million per MW (beyond 200 MW), extconcludeable to Rs 15 million per MW in exceptional cases.

The central financial assistance (CFA) disbursement for renewable energy projects grew sharply, reaching Rs 92.21 billion in 2024-25 (till December 2024) as compared to Rs 48.94 billion disbursed in 2023-24. Alongside project-linked CFA, production-linked incentives have been introduced to promote domestic manufacturing.

In another notable development, in September 2025, the GST Council reduced the tax rate on renewable energy equipment such as solar modules, wind turbines and waste-to-energy devices from 12 per cent to 5 per cent, while revising the tax on coal to 18 per cent, with compensation cess subsumed. This reform is expected to reduce renewable energy project costs, enhance competitiveness and unlock savings of nearly Rs 1.5 trillion in investments by 2030.

International funding

The year witnessed strong participation from multilateral and foreign institutions in supporting India’s clean energy transition. According to data from the Department for Promotion of Indusattempt and Trade, foreign direct investment (FDI) in India’s renewable energy sector increased by 6.7 per cent in 2024-25, reaching $4,012 million against $3,760 million in 2023-24. However, the total FDI in the power sector decreased by 16 per cent in 2024-25, with inflows of $1,428.57 million as compared to $1,701 million in the previous year.

In July 2025, the Asian Development Bank (ADB), alongside the Green Climate Fund, launched the India Green Finance Facility, mobilising nearly $8 billion in co-financing for private sector-led clean energy projects. During the year, ADB approved loans of $241.3 million to modernise power distribution in West Bengal and $434.25 million to support renewable energy and battery storage development in Assam. Additionally, in November 2024, Tata Power and ADB signed an MoU at the COP29 climate conference to explore financing renewable energy and infrastructure projects valued at $4.25 billion. The projects aim to strengthen India’s renewable energy capacity, enhance power distribution networks and expand clean energy infrastructure.

In September 2025, PFC signed a €150 million loan agreement with Germany’s KfW to support projects under the RDSS, and a Rs 32 billion loan agreement with the Japan Bank for International Cooperation (JBIC) for a bamboo-based bioethanol and chemicals project in Assam. In March 2025, PFC signed a general agreement with JBIC to set up a credit line of up to JPY 120 billion, of which the JBIC portion is JPY 72 billion. This marks JBIC’s largest green financing deal with an Indian company. Earlier, in October 2024, PFC secured a record $1.26 billion foreign currency term loan through IFSC GIFT City to fund green energy projects, marking the largest such loan by an Indian public sector undertaking.

In March 2025, IREDA secured a loan facility from SBI Tokyo amounting to approximately $172 million, including a greenshoe option of around $66.2 million through external commercial borrowings. The loan is structured as a five-year unsecured facility with a bullet repayment at maturity.

In October 2024, REC raised $500 million through green dollar bonds for renewable energy projects. The five-year note has a coupon rate of 4.75 per cent per annum, payable semi-annually, with a maturity date of September 27, 2029. The issuance was part of the company’s $10 billion global medium-term programme.

Private and institutional investors remained active. The International Finance Corporation partnered with Axis Bank for a $500 million loan to expand green and blue finance, and separately committed $55 million for a 180 MW/360 MWh stand-alone battery storage project in Gujarat.

In parallel, strategic capital continued to flow, with Hexa Climate Solutions committing $500 million through the acquisition of Fortum’s renewable energy portfolio in India, while TotalEnergies expanded its joint solar platform with Adani Green. These flows underline India’s ability to attract both concessional climate finance and global private capital to sustain its ambitious energy transition goals.

Conclusion

Going forward, financing flows into the power sector are expected to remain robust, supported by strong demand growth, the government’s emphasis on reliable supply and clean energy capacity expansion, and greater investor confidence.

The mix of domestic debt, global capital and equity mobilisation is likely to broaden further, with green bonds and blconcludeed finance instruments gaining prominence. Public sector lconcludeers are expected to continue driving large-scale funding, while multilateral and bilateral agencies will play a greater role in supporting grid modernisation, green hydrogen and battery storage. At the same time, private capital markets are opening up for energy companies, with more IPOs and QIPs on the horizon. Overall, 2025-26 will be shaped by how effectively financing institutions balance the scale-up of conventional and renewable power with emerging priorities such as distribution reforms, energy storage and the decarbonisation of hard-to-abate sectors.

Aastha Sharma