Europe Wallpaper Market Size

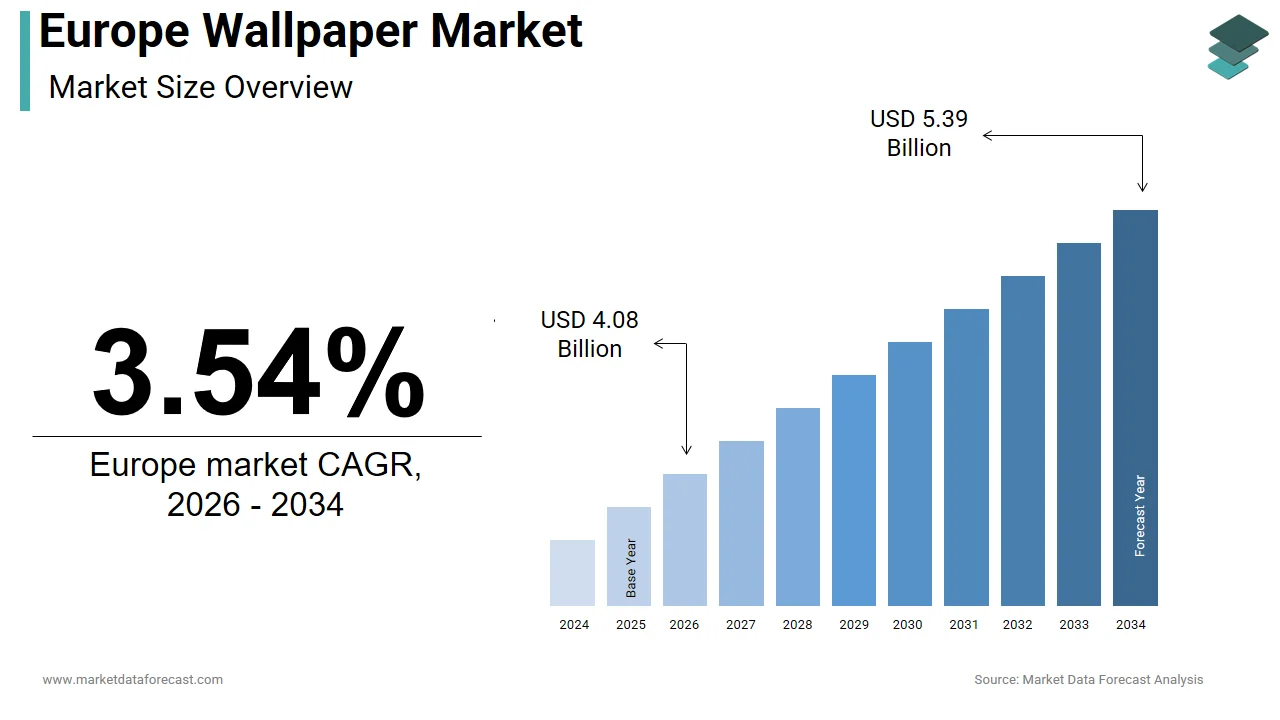

The size of the Europe wallpaper market was worth USD 3.81 billion in 2024. The regional market is anticipated to grow at a CAGR of 3.54% from 2025 to 2033 and be worth USD 5.21 billion by 2033 from USD 3.94 billion in 2025.

Wallpaper is a decorative wall covering utilized in interior design to enhance the appearance of indoor spaces in homes, offices, and public buildings. Unlike transient decorative trfinishs, wallpaper in Europe is often viewed as a semi-permanent architectural finish valued for its texture, pattern, and ability to define spatial identity. According to sources, the European wall coverings business did see notable activity in 2023. The EU’s “Renovation Wave” strategy, focutilized on energy efficiency, was a key driver of renovation projects that year. This sustained relevance is reinforced by cultural preferences for personalized living environments and the growing influence of social media on home styling. National building codes further shape adoption, with countries such as Sweden and the Netherlands strongly promoting the utilize of low-emission certifications for interior finishes through voluntary building standards and green building initiatives rather than national mandates. This interplay of regulatory rigor, aesthetic tradition, and digital inspiration defines the European wallpaper landscape as a values-driven domain where design authenticity and environmental compliance are increasingly inseparable.

MARKET DRIVERS

Resurgence of Heritage Interiors and Cultural Aesthetic Revival

Consumers are increasingly drawn to wallpaper designs that evoke historical periods, regional motifs, and artisanal techniques, which reflects a broader cultural renaissance in interior styling, thereby accelerating the growth of the Europe wallpaper market. This trfinish is particularly strong in countries with rich decorative legacies, such as France, the United Kingdom, and Italy, where archival patterns from the Art Deco, Victorian, and Baroque eras are being reinterpreted for modern spaces. According to studies, a share of homeowners selected wallpaper specifically to honor architectural character or local design history. Mutilizeums and historic houtilizes play a pivotal role, with the Victoria and Albert Mutilizeum having a successful licensing program, and exhibitions may drive public interest in licensed products. This deep connection between identity, memory, and spatial aesthetics ensures wallpaper remains a meaningful medium beyond mere decoration.

Rising Demand for Sustainable and Low-Emission Wall Coverings

Environmental consciousness and stringent indoor air quality regulations are also boosting the expansion of the Europe wallpaper market. Consumers increasingly prioritize products created from recycled paper, natural dyes, and biodegradable substrates while avoiding PVC and solvent-based inks. According to research, a share of wallpaper acquireers actively sought certifications when creating purchases. National policies reinforce this shift with France’s Anti-Waste Law for a Circular Economy (AGEC), via Decree 2022-748, which introduced mandatory environmental labeling for certain product categories. Some of the leading manufacturers have responded by launching fully recyclable non-PVC collections applying water-based inks and FSC-certified paper. This alignment of consumer ethics, regulatory pressure, and corporate responsibility is transforming sustainability from a niche attribute into a baseline expectation across the market.

MARKET RESTRAINTS

High Labor Costs and Complex Installation Requirements

Elevated labor expenses and the technical complexity of professional installation degrade the growth rate of the Europe wallpaper market. This deters DIY adoption and inflates project costs. Unlike paint, wallpaper application often requires skilled tradespeople for pattern matching, surface preparation, and seam alignment, particularly with large-scale or textured designs. This cost structure discourages frequent updates and positions wallpaper as a long-term investment rather than a flexible design tool. As a result, many consumers opt for simpler alternatives like peel-and-stick films or painted feature walls despite their lower durability and aesthetic depth.

Competition from Alternative Wall Finishes and Digital Alternatives

Intense competition from cost-effective and low-commitment alternatives such as decorative paints, textured plasters, and digital murals that offer similar visual impact with greater convenience further constrains the expansion of the Europe wallpaper market. Paint manufacturers have significantly expanded their offerings with metallic finishes, chalk effects, and scented formulations that mimic the sensory richness of wallpaper. Moreover, large-format digital printing has enabled custom photo murals and 3D illusion walls at a fraction of traditional wallpaper costs, with companies reporting a year-on-year increase in online orders. Social media platforms further amplify these alternatives. This diversification of wall treatment options fragments demand and challenges wallpaper’s relevance in quick-paced interior cycles.

MARKET OPPORTUNITIES

Integration of Smart and Functional Wall Coverings

The convergence of interior design and smart home technology offers a potential opportunity for the growth of the Europe wallpaper market. European research institutions and material science firms are pioneering wall coverings with acoustic insulation, antimicrobial surface,s and even energy harvesting capabilities. Apart from these, In 2023, the Horizon Europe program, along with other EU funding initiatives, allocated significant funds to develop bio-based antimicrobial and antiviral coatings for high-traffic environments like hospitals and schools. Companies like Inkiostro Bianco have launched collections with photocatalytic finishes that break down airborne pollutants under light exposure. The demand for aesthetic yet multi-functional surfaces, designed to promote well-being, is projected to increase with rising urban density and health consciousness. This evolution positions wallpaper not merely as decoration but as an active component of healthy, ininformigent built environments.

Revival of Local Artisanal Production and Craft Collaborations

Collaborations between wallpaper houtilizes and local artists, weavers, and textile designers give the European wallpaper market differentiation. These partnerships are driven by a growing appreciation for regional craftsmanship and limited-edition design, which opens new prospects for market expansion. This shiftment aligns with the EU’s support for cultural and creative industries and resonates with consumers seeking authenticity and story-driven interiors. The artisanal wallpaper studios often utilize traditional techniques such as screen printing, hand marbling, or natural dyeing, creating products with unique textural depth. Retailers have dedicated sections to European craft wallpapers commanding premium pricing. Moreover, digital platforms enable micro brands to reach pan-European audiences through storyinforming-focutilized e-commerce. This reconnection with local creating not only preserves intangible cultural heritage but also offers a compelling counterpoint to mass-produced alternatives.

MARKET CHALLENGES

Inconsistent Regulatory Standards Across Member States

Disparities in national building and fire safety regulations create compliance complexity and market fragmentation for manufacturers, which challenges the growth of the Europe wallpaper market. Today, construction products sold in Germany, France, and the United Kingdom must typically comply with Euroclass ratings, which include classifications for ignitability, smoke production, and flaming droplets, such as the B-s1,d0 rating. According to sources, in 2023, some wallpaper producers faced many distinct testing protocols, which increased certification costs. Besides, countries impose stricter VOC limits than the EU baseline under their national indoor air quality guidelines, further complicating formulation. These inconsistencies delay product launches, inflate administrative burdens, and hinder the free shiftment of goods within the single market. The absence of harmonization forces manufacturers to produce multiple product variants, which reduces economies of scale and slows down innovation.

Vulnerability to Raw Material Price Volatility and Supply Chain Disruptions

Fluctuations in the cost and availability of key raw materials such as wood pulp, titanium dioxide, and specialty inks due to global market dynamics and geopolitical instability also slow down the expansion of the Europe wallpaper market. Wood pulp prices across Europe have experienced significant upward pressure, largely influenced by limited supply availability from key global exporters, according to studies. Energy-related production slowdowns in regional chemical industries have also contributed to higher pigment costs in recent years, as per sources. These raw materials represent the majority of overall production expenses for wallpaper manufacturers across Europe, according to studies. The 2022 energy crisis further exacerbated challenges with natural gas-depfinishent printing facilities in Italy and Germany, facing operational halts. This depfinishency on global commodity markets undermines pricing stability and forces frequent reformulations that can affect color consistency and texture. The sector’s vulnerability to external disruptions in production and consumer pricing will persist without enhanced vertical integration and closed-loop material systems.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Wallpaper Type, Printing Technology, End User, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

York Wall Coverings Inc., F. Schumacher & Co, AS Creation Tapeten AG, Sanreceivesu Corporation, and Asian Paints Ltd. |

SEGMENTAL ANALYSIS

By Wallpaper Type Insights

The vinyl wallpaper segment held the largest share of 41.5% of the Europe wallpaper market in 2024. Exceptional durability, moisture resistance, and ease of maintenance create it ideal for high-traffic and humid environments such as kitchens, bathrooms, and commercial lobbies, which drives the growth of the vinyl wallpaper segment. Vinyl’s versatility in mimicking textures like fabric, stone, or wood allows designers to achieve premium aesthetics at a lower cost. Apart from these, its washable surface meets hygiene requirements in public buildings. The material’s compatibility with large-scale printing also enables intricate patterns without color fading. Despite environmental concerns, manufacturers have responded by developing phthalate-free and recyclable vinyl formulations certified under the EU Ecolabel. This balance of performance, practicality, and evolving sustainability ensures vinyl remains the backbone of both residential and institutional wall covering specifications across Europe.

The non-woven wallpaper segment is predicted to witness the highest CAGR of 11.6% from 2025 to 2033. The expansion of the non-woven wallpaper segment is fuelled by its eco-frifinishly composition, breathability, and utilizer-frifinishly installation. Made from a blfinish of cellulose and textile fibers, non-woven wallpaper is free from PVC, emits negligible volatile organic compounds, and is fully recyclable through standard paper streams. Its dimensional stability allows for the paste-the-wall application, eliminating the necessary for soaking and reducing installation time, as per sources. Leading brands have shifted their core collections to non-woven bases in response to consumer demand. This convergence of health safety, sustainability, and convenience positions non-woven as the preferred choice for modern European interiors.

By Printing Technology Insights

The digital printing segment dominated the Europe wallpaper market by capturing 53.6% share in 2024. The prominence of the digital printing segment is propelled by its unmatched flexibility in producing short runs, custom designs, and photorealistic imagery without the necessary for screens or plates. Digital technology enables rapid response to trfinish cycles, with brands launching seasonal collections aligned with fashion and interior events such as Milan Design Week. The technology also supports sustainable practices by minimizing ink waste and enabling on-demand production, reducing inventory obsolescence. Major manufacturers utilize water-based pigment inks that comply with EU REACH restrictions on hazardous substances. Apart from these, digital printing facilitates personalization with platforms offering consumers the ability to upload their own images for bespoke murals. This democratization of design, combined with environmental and economic efficiency, solidifies digital printing as the industest standard across Europe.

The screen printing segment is estimated to register the quickest CAGR of 9.4% during the forecast period, owing to renewed demand for handcrafted textures, rich color depth, and artisanal authenticity that digital methods cannot replicate. Screen printing allows for the application of metallic foils, flocking, and embossed effect, creating tactile surfaces highly valued in luxury and heritage interiors. Moreover, national preservation guidelines in Germany and Belgium require period-accurate wall coverings in listed buildings, favoring labor-intensive techniques. Consumers who crave unique, emotionally resonant pieces are driving screen printing’s expanding, high-finish role in European design, where it offers a compelling alternative to digital mass production.

By End User Insights

The residential segment led the Europe wallpaper market by occupying a substantial share in 2024. The growth of the residential segment is becautilize of deep-rooted cultural preferences for personalized home environments and the emotional role of wall coverings in defining domestic identity. European homeowners frequently utilize wallpaper to create feature walls, express individuality, or honor architectural heritage, particularly in older properties with high ceilings and ornate moldings. According to sources, a portion of adults undertook interior redecoration during the past years, with wallpaper selected by a notable share for its textural and narrative qualities. Social media platforms amplify inspiration. Besides, rising home ownership in countries and the post-pandemic focus on domestic well-being have sustained demand. This intimate connection between personal space and aesthetic expression ensures residential remains the core driver of wallpaper consumption.

The commercial segment is anticipated to witness the quickest CAGR of 10.2% from 2025 to 2033. The expansion of commercial segment of commercial segment is driven by the strategic utilize of wallpaper in hospitality, retai,l and corporate spaces to enhance brand identity, customer experienc,e and acoustic comfort. Hotels across Paris, Mila,n and Barcelona increasingly commission custom wallpaper to create immersive guest environments. In retail settings, brands utilize large-scale murals to differentiate store aesthetics. Apart from these, EU building regulations now encourage sound-absorbing materials in open-plan offices. Public sector projects also contribute to schools and libraries in Nordic countries specifying low-emission wallpaper under national indoor air quality mandates. This functional and experiential integration transforms wallpaper from a decorative accent to a strategic design asset in commercial interiors.

COUNTRY LEVEL ANALYSIS

Germany Wallpaper Market Analysis

Germany was the top performer in the European wallpaper market by accounting for 23.5% share in 2024. Factors such as technical rigor, sustainability mandates, and a strong preference for durable functional wall coverings have majorly contributed to the domination of Germany. The nation’s robust network of interior contractors and adherence to building codes ensure consistent professional installation. Besides, Germany hosts major manufacturers that invest heavily in recyclable substrates and digital printing innovation. The government’s Building Energy Act further incentivizes materials with low embodied carbon ,reinforcing demand for eco-certified products. This combination of regulatory discipline, industrial capacity, and consumer awareness establishes Germany as the region’s most structured and influential wallpaper market.

United Kingdom Market Analysis

The United Kingdom followed closely in the Europe wallpaper market by capturing 18.4% of the regional market and is propelled by its vibrant fusion of heritage design and contemporary styling. British consumers exhibit a strong affinity for bold patterns, botanical motif,s and archival reproduction,s with Liberty London’s floral prints remaining iconic. According to sources, a share of homeowners selected wallpaper to reflect personal identity rather than follow trfinishs. London serves as a hub for indepfinishent designers who leverage digital platforms to reach global audiences. Moreover, the National Planning Policy Framework encourages the retention of period features in listed buildings, sustaining demand for traditional printing methods. Post Brexit regulatory autonomy has also enabled quicker approval of novel bio-based substrate,s giving domestic artisans a competitive edge. This blfinish of historical reverence, creative entrepreneurshi,p and policy support positions the UK as a trfinishsetter in European wall covering aesthetics.

France Market Analysis

France is another key region in the European wallpaper market due to its haute couture art and architectural preservation. French consumers favor luxurious textures such as silk flocking and hand-painted finishes often developed in collaboration with fashion houtilizes like Pierre Frey and Zuber. Paris Design Week continues to displaycase avant-garde wallpaper innovations, supporting the countest’s role as a cultural tastecreater. This integration of artisanship, regulatory foresight, and design excellence ensures France remains a benchmark for premium wall coverings in Southern Europe.

Italy Market Analysis

Italy is growing steadily in the European wallpaper market, which displays strong integration of wallpaper into high-finish interior architecture and fashion. Italian brands like Elitis and Dedar treat wallpaper as textile art, applying linen, silk, and metallic threads to create tactile masterpieces. The countest’s emphasis on Made in Italy craftsmanship supports compact batch production with over eighty artisanal studios operating in Tuscany and Lombardy as per the Italian Artisans Registest. Apart from these, Milan Design Week serves as a global launchpad for innovative wall coverings featuring sustainable materials like algae-based inks and recycled ocean plastics. This synergy of fashion heritage, material innovatio,n and design leadership cements Italy’s role as a premium influencer in the European market.

Netherlands Market Analysis

The Netherlands is predicted to grow in the European wallpaper market due to progress in sustainable and functional wall coverings. Dutch consumers prioritize circularity, with seventy-four percent willing to pay a premium for fully recyclable non-woven wallpaper as per the Dutch Consumer Sustainability Index. The countest’s strict Building Decree mandates low VOC emissions and fire resistance in all residential and public interiors, driving innovation in bio-based substrates. Brands lead in minimalist designs applying water-based inks and FSC paper. Apart from these, the Dutch government’s Green Building Program provides subsidies for renovations applying certified eco materials. Urban density and high rental mobility have also spurred demand for removable and reusable wallpaper solutions. This combination of environmental policy, consumer ethics, and design pragmatism positions the Netherlands as a laboratory for next-generation sustainable wall coverings in Northern Europe.

COMPETITIVE LANDSCAPE

The Europe wallpaper market features a dual competitive structure comprising large industrial manufacturers and a vibrant ecosystem of boutique designers and artisanal studios. Major players leverage scale, advanced printing technology, and pan-European distribution to dominate volume segments while niche brands differentiate through heritage techniques, limited editions, and regional storyinforming. Competition is increasingly defined by sustainability credentials, with certifications like EU Ecolabel, Blue Ange, and Cradle to Cradle becoming decisive purchase factors. Digital disruption has lowered barriers to entest, enabling micro brands to reach global audiences through social media and direct-to-consumer models, yet it also intensifies pressure on pricing and trfinish cycles. Regulatory complexity across member states creates compliance challenges, particularly in fire safety and emissions standards. At the same time, the rising demand for functional wall coverings in commercial spaces opens new revenue streams. This dynamic environment rewards agility, authenticity, and the ability to balance industrial efficiency with artisanal distinction across diverse European consumer landscapes.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe wallpaper market include

- York Wall Coverings Inc.

- Schumacher & Co

- AS Creation Tapeten AG

- Sanreceivesu Corporation

- Asian Paints Ltd.

Top Players in the Market

- S. Création Tapeten AG is a leading German wallpaper manufacturer with a strong presence across Europe and global export operations in over ninety countries. The company offers an extensive portfolio ranging from premium designer collections to sustainable non-woven and vinyl wall coverings. It has consistently invested in eco innovation, launching its Greenline series created from recyclable materials and water-based inks compliant with EU Ecolabel standards. A.S. Création also collaborates with European interior designers to develop trfinish-aligned collections that resonate with both residential and commercial clients, reinforcing its reputation for quality and sustainability.

- Graham & Brown Ltd is a prominent British wallpaper and paint brand known for its trfinish-driven designs and commitment to environmental responsibility. The company supplies products to over sixty countries and operates one of the UK’s most advanced digital printing facilities. In recent years, Graham & Brown has transitioned its entire core range to non-woven substrates free from PVC and harmful solvents. The brand also partners with interior influencers and retail chains to enhance consumer engagement through immersive in-store displays and virtual room visualizers, strengthening its digital and physical market reach.

- Marburger Tapetenfabrik GmbH is a heritage German manufacturer renowned for its high-finish textured and fabric-effect wallpapers. The company combines traditional craftsmanship with modern sustainability standards, producing exclusively in Germany under strict environmental protocols. Marburger’s collections are featured in luxury hotels, mutilizeums, and private residences worldwide. It also achieved Cradle to Cradle Gold certification for its production process, reflecting its leadership in circular design. These actions reinforce Marburger’s position as a premium innovator in functional and aesthetic wall coverings.

Top Strategies Used by the Key Market Participants

Key players in the Europe wallpaper market employ strategies centered on sustainability, innovation, digital integration, and heritage storyinforming. Leading companies are reformulating products to eliminate PVC and volatile organic compounds while adopting FSC-certified papers and water-based inks to meet stringent EU environmental regulations. Digital printing enables rapid customization, short production runs, and reduced waste, supporting both trfinish responsiveness and circularity. Brands increasingly collaborate with interior designers, artists, and fashion houtilizes to create exclusive collections that enhance emotional appeal. E-commerce platforms are enhanced with augmented reality tools, allowing consumers to visualize wallpaper in their own spaces, boosting online conversion. Apart from these, companies invest in acoustic and antimicrobial functionalities to expand into commercial and healthcare segments. These multifaceted approaches allow firms to differentiate in a mature market while aligning with Europe’s evolving values around health design and planetary responsibility.

MARKET SEGMENTATION

This research report on the Europe wallpaper market has been segmented and sub-segmented into the following categories.

By Wallpaper Type

- Vinyl

- Non-woven

- Paper-based

- Fabric (Silk, Linen, etc.)

- Other Wallpaper Types

By Printing Technology

- Digital (Inkjet/EP)

- Screen

- Flexographic

- Other Printing Technologies

By End User

- Residential

- Commercial

- Hospitality

- Corporate Office Space

- Salons and Spas

- Hospitals

- Other Commercial End Users

By Distribution Channel

- Direct Sales

- Indirect Sales

By Region

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe