As the pan-European STOXX Europe 600 Index edges higher amidst dovish signals from U.S. Fed Chair Jerome Powell and easing U.S.-China trade tensions, investors are keenly observing mixed performances across major European indices, with France’s CAC 40 revealing notable resilience. In such a dynamic market environment, identifying promising stocks often involves viewing for companies that demonstrate robust fundamentals and adaptability to shifting economic conditions, creating them potential hidden gems in the European landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In Europe

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sparta | NA | nan | nan | ★★★★★☆ |

| Inmocemento | 28.68% | 4.15% | 33.84% | ★★★★★☆ |

| Freetrailer Group | 0.01% | 22.96% | 31.56% | ★★★★★☆ |

| Evergent Investments | 3.82% | 10.46% | 23.17% | ★★★★★☆ |

| Deutsche Balaton | 4.58% | -18.46% | -16.14% | ★★★★★☆ |

| ABG Sundal Collier Holding | 35.58% | -7.59% | -18.30% | ★★★★☆☆ |

| Procimmo Group | 141.47% | 6.84% | 6.01% | ★★★★☆☆ |

| Dn Agrar Group | 63.27% | 15.46% | 33.00% | ★★★★☆☆ |

| Practic | NA | 4.86% | 6.64% | ★★★★☆☆ |

| MCH Group | 126.04% | 19.05% | 60.90% | ★★★★☆☆ |

We’ll examine a selection from our screener results.

Simply Wall St Value Rating: ★★★★★☆

Overview: Voyageurs du Monde SA operates as a travel agency both in France and internationally, with a market capitalization of €788.44 million.

Operations: Voyageurs du Monde generates revenue primarily from Tailor-Made Trips (€414.62 million) and Adventure Tours (€205.99 million), with additional income from Bike tours (€113.78 million) and Miscellaneous activities (€0.88 million).

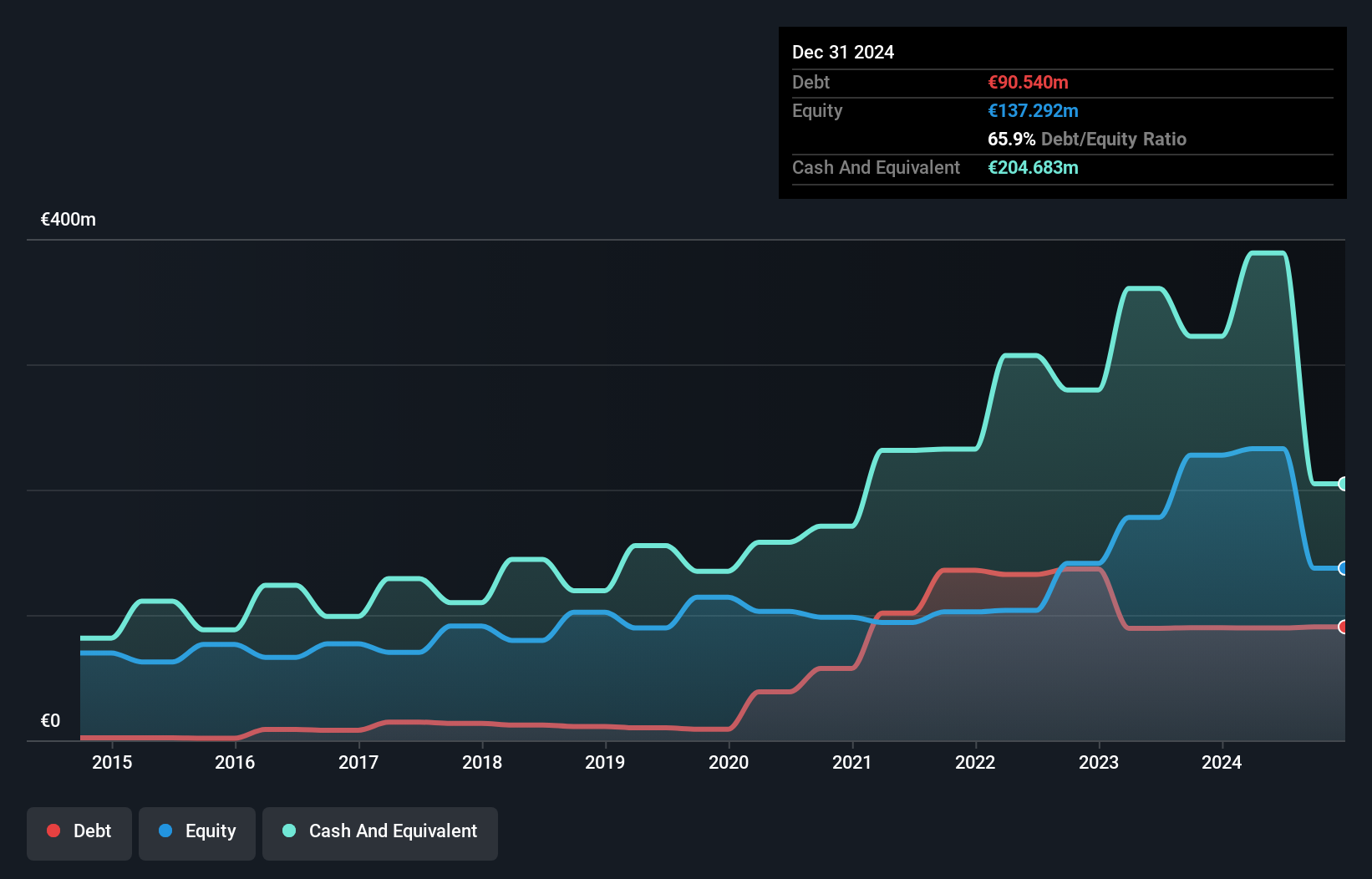

Voyageurs du Monde, a niche player in the travel sector, revealcases robust earnings growth of 7.6% over the past year, outpacing the broader hospitality industest at 1.9%. With its debt to equity ratio escalating from 7.7% to 65.9% over five years, it seems financial leverage has increased significantly. The company trades at a notable discount of 26.7% below estimated fair value and boasts high-quality earnings with interest payments well-covered by EBIT at a multiple of 23.9x. Despite shareholder dilution recently, sales are expected to grow by around 7% in 2025 according to recent guidance.

Simply Wall St Value Rating: ★★★★★☆

Overview: MPC Container Ships ASA owns and operates a portfolio of container vessels and has a market capitalization of NOK7.23 billion.

Operations: The company’s primary revenue stream is from container shipping, generating $527.38 million. The market capitalization stands at NOK7.23 billion.

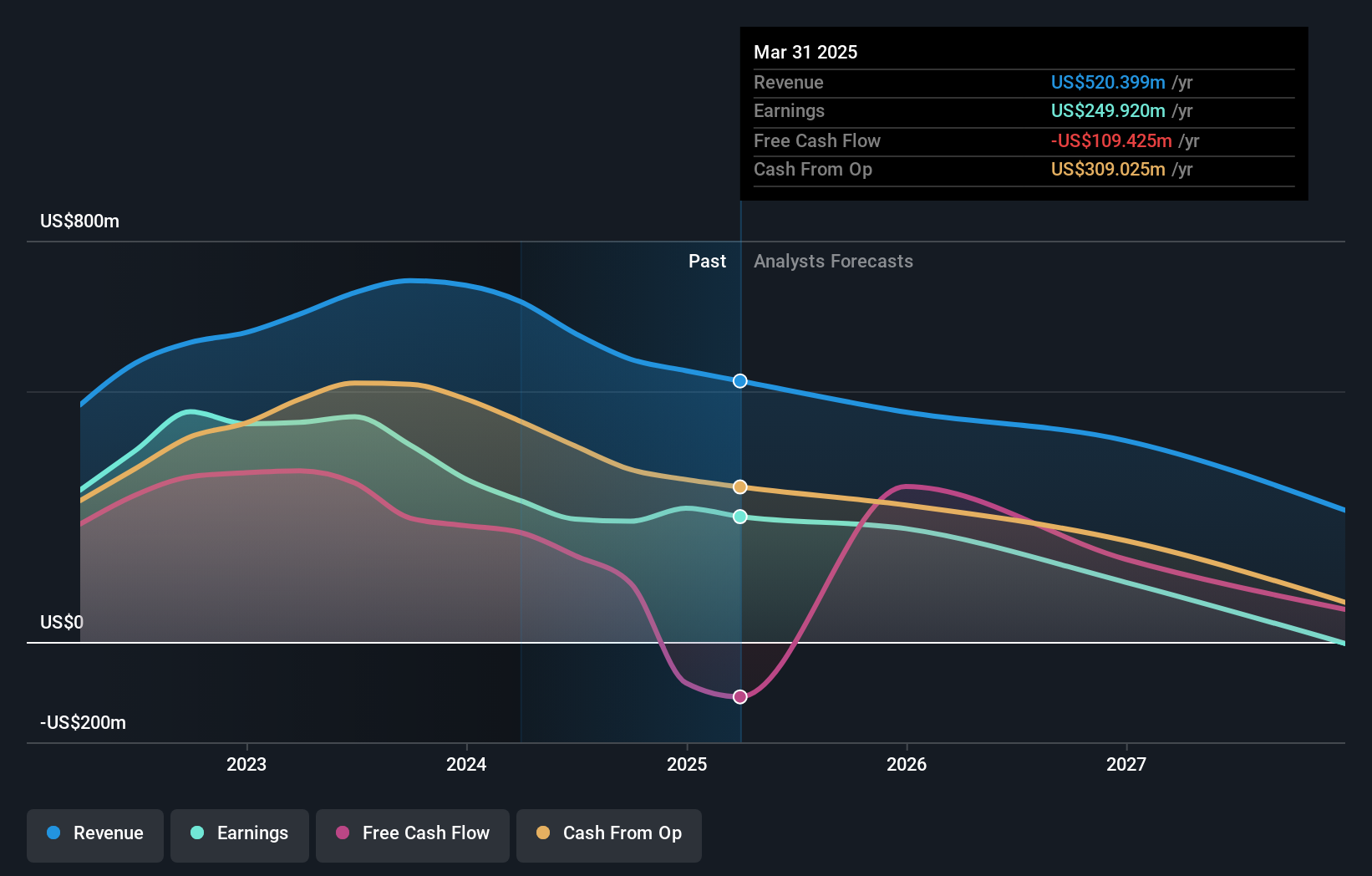

MPC Container Ships, a notable player in the container shipping sector, has been navigating both challenges and opportunities. The company trades at 29.3% below its estimated fair value and has seen earnings grow by 7.4% over the past year, outpacing the industest average of -4%. Despite predictions of a significant revenue decline in the coming years, MPC’s strategic investments in new vessels could bolster future earnings. Recent orders for two fuel-efficient ships are expected to generate US$92 million in revenue over their charter period, enhancing earnings visibility and reducing regulatory risks with modernized fleet capabilities.

Simply Wall St Value Rating: ★★★★★★

Overview: XANO Industri AB (publ) is a company that develops, manufactures, and sells industrial products and automation equipment across Sweden, the rest of the Nordic countries, Europe, and internationally with a market cap of approximately SEK3.45 billion.

Operations: XANO generates revenue primarily from three segments: Industrial Solutions (SEK2.02 billion), Industrial Products (SEK872.13 million), and Precision Technology (SEK478.89 million).

XANO B, a nimble player in the machinery sector, has revealn impressive earnings growth of 51% over the past year, outpacing its industest peers. The company is debt-free, a significant shift from five years ago when it had a debt to equity ratio of 74.2%. A substantial one-off gain of SEK66M has influenced recent financial results. Despite this boost, earnings have seen an average annual decrease of 14.8% over five years. With positive free cash flow and no interest payment concerns due to zero debt, XANO B seems well-positioned for operational stability shifting forward.

Key Takeaways

Interested In Other Possibilities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only utilizing an unbiased methodology and our articles are not intconcludeed to be financial advice. It does not constitute a recommconcludeation to acquire or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividconclude Powerhoapplys (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com