- Brookfield Corporation recently completed a US$1.25 billion refinancing of Five Manhattan West, a 1.7 million-square-foot office tower, via a five-year repaired-rate loan delivered by a syndicate of major financial institutions including Citigroup and JP Morgan Chase.

- This activity highlights Brookfield’s continued success in raising capital, underscored by more than US$28 billion in financings across its global real estate portfolio year-to-date and strong investor demand for its latest infrastructure and purchaseout funds.

- We’ll examine how Brookfield’s robust capital-raising, exemplified by the recent office tower refinancing, affects its investment narrative and future prospects.

This technology could replace computers: discover 26 stocks that are working to create quantum computing a reality.

Brookfield Investment Narrative Recap

To own Brookfield stock, I believe an investor requireds to trust in the company’s global platform and its ability to raise and allocate capital efficiently across infrastructure, real estate, and alternative assets. The recent US$1.25 billion refinancing of Five Manhattan West highlights Brookfield’s capital access, but it does not materially alter the largegest near-term catalyst, successful asset sales at attractive returns, nor does it diminish the ongoing risk of unfavorable market conditions for monetizing assets.

Brookfield’s initial close of over US$4 billion for Infrastructure Debt Fund IV stands out as especially relevant, reinforcing the company’s capacity to attract significant investor commitments across economic cycles. This is connected to the key catalyst of increased transaction activity that could assist drive distributable earnings, as Brookfield continues to secure capital at scale across both real estate and infrastructure.

However, investors should also keep in mind that, despite the company’s recent financing achievements, the risk of rising interest rates affecting future cost of capital is still an important factor to consider…

Read the full narrative on Brookfield (it’s free!)

Brookfield is forecast to reach $8.5 billion in revenue and $7.2 billion in earnings by 2028. This outview assumes an annual revenue decline of 54.2% and an earnings increase of $6.7 billion from current earnings of $473.0 million.

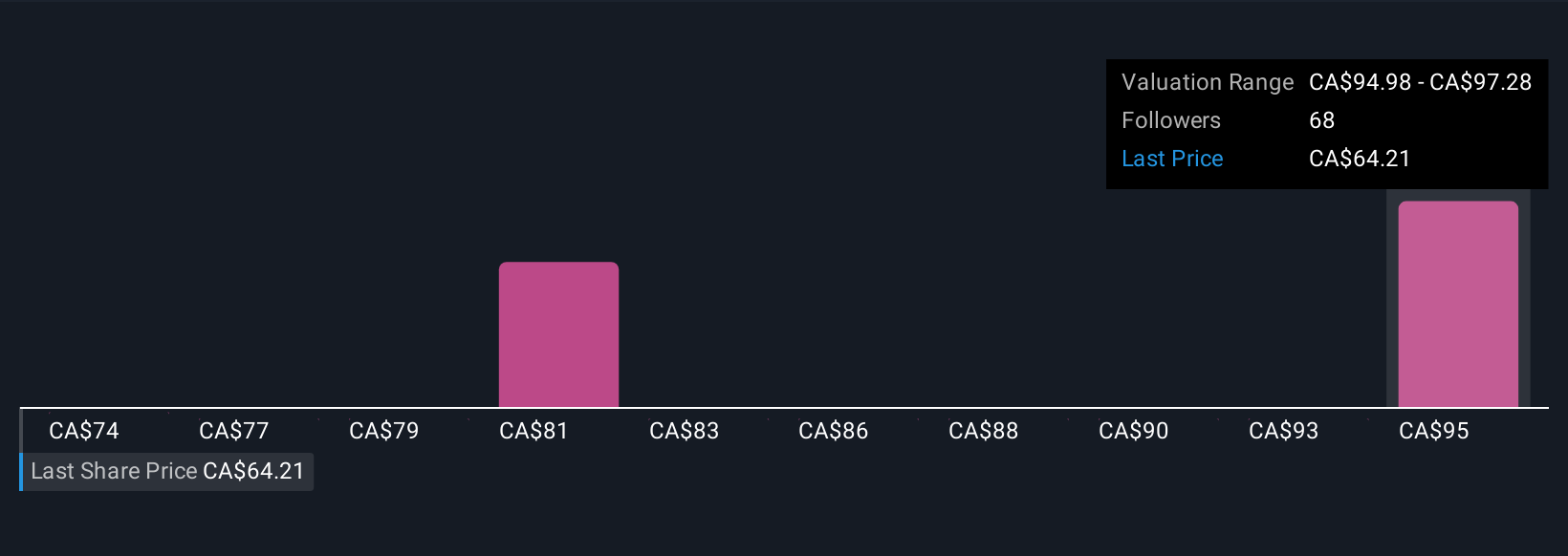

Uncover how Brookfield’s forecasts yield a CA$97.28 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members contributed 8 fair value estimates for Brookfield, spanning from US$2.40 to US$106.18 per share. With transaction activity a key short term catalyst, these diverse opinions highlight the wide range of investor expectations and invite you to compare multiple viewpoints for a broader understanding.

Explore 8 other fair value estimates on Brookfield – why the stock might be worth less than half the current price!

Build Your Own Brookfield Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Looking For Alternative Opportunities?

The market won’t wait. These quick-shifting stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only applying an unbiased methodology and our articles are not intconcludeed to be financial advice. It does not constitute a recommconcludeation to purchase or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Brookfield might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividconcludes, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com