Sustainable Food Packaging Market Forecast and Outsee 2025 to 2035

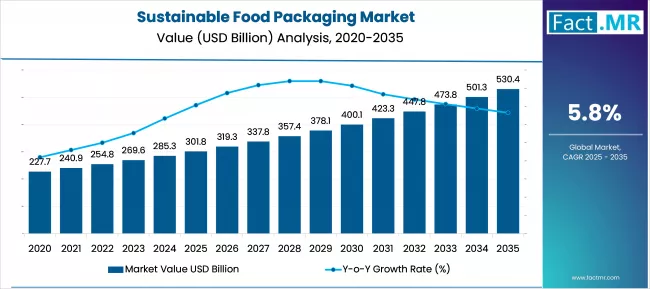

The global sustainable food packaging market is projected to grow from USD 301.8 billion in 2025 to approximately USD 530.4 billion by 2035, recording an absolute increase of USD 228.6 billion over the forecast period. This translates into a total growth of 75.8%, with the market forecast to expand at a compound annual growth rate (CAGR) of 5.8% between 2025 and 2035.

The overall market size is expected to grow by nearly 1.76X during the same period, supported by increasing consumer awareness of environmental impacts, strengthening regulatory frameworks for plastic waste reduction, and growing corporate sustainability commitments across global food and beverage industries.

Quick Stats for Sustainable Food Packaging Market

- Sustainable Food Packaging Market Value (2025): USD 301.8 billion

- Sustainable Food Packaging Market Forecast Value (2035): USD 530.4 billion

- Sustainable Food Packaging Market Forecast CAGR: 5.8%

- Leading Packaging Type in Sustainable Food Packaging Market: Recyclable packaging (42%)

- Key Growth Regions in Sustainable Food Packaging Market: North America, Europe, and Asia Pacific

- Top Key Players in Sustainable Food Packaging Market: Amcor Plc, WestRock, International Paper, Tetra Pak, Sealed Air Corporation, Berry Global, Mondi Group, Graphic Packaging Holding, Ranpak Holdings

Between 2025 and 2030, the sustainable food packaging market is projected to expand from USD 301.8 billion to USD 406.7 billion, resulting in a value increase of USD 104.9 billion, which represents 45.9% of the total forecast growth for the decade. This phase of growth will be shaped by accelerating plastic waste regulations, increasing consumer preference for eco-friconcludely packaging, and growing adoption of circular economy principles. Packaging manufacturers are expanding their sustainable product portfolios to address the evolving demand for environmentally responsible, functional, and cost-effective packaging solutions.

Sustainable Food Packaging Market Key Takeaways

| Metric | Value |

|---|---|

| Estimated Value in (2025E) | USD 301.8 billion |

| Forecast Value in (2035F) | USD 530.4 billion |

| Forecast CAGR (2025 to 2035) | 5.8% |

From 2030 to 2035, the market is forecast to grow from USD 406.7 billion to USD 530.4 billion, adding another USD 123.7 billion, which constitutes 54.1% of the overall ten-year expansion. This period is expected to be characterized by expansion of bio-based packaging materials, integration of smart packaging technologies, and development of advanced recycling infrastructure. The growing adoption of zero-waste initiatives and increasing emphasis on packaging lifecycle assessment will drive demand for innovative sustainable packaging solutions with enhanced functionality and environmental credentials.

Between 2020 and 2025, the sustainable food packaging market experienced steady growth from USD 285.2 billion to USD 301.8 billion, driven by increasing environmental consciousness and growing regulatory pressure on single-apply plastics. The market developed as brands and consumers recognized the urgent required to address packaging waste while maintaining product protection and shelf-life requirements. Sustainability awareness and circular economy adoption launched emphasizing the importance of packaging materials that could support both environmental objectives and commercial functionality across food and beverage supply chains.

Why the Sustainable Food Packaging Market is Growing?

Market expansion is being supported by the increasing consumer demand for environmentally responsible packaging solutions and the corresponding required for materials that can deliver both sustainability benefits and functional performance. Modern consumers are increasingly prioritizing brands that demonstrate environmental stewardship while food companies are responding to stakeholder pressure for sustainable packaging alternatives that support their corporate responsibility goals. Sustainable packaging technologies’ proven ability to deliver environmental benefits while maintaining product protection creates them essential components of modern brand positioning and regulatory compliance strategies.

The growing emphasis on circular economy principles and waste reduction is driving demand for packaging materials that can be recycled, composted, or biodegraded at conclude-of-life while supporting product quality and safety requirements. Brand preference for packaging solutions that combine environmental credentials with marketing appeal and supply chain efficiency is creating opportunities for innovative material technologies and design approaches. The rising influence of environmental regulations, retailer sustainability requirements, and consumer purchasing decisions is also contributing to increased adoption of sustainable packaging across diverse food and beverage categories.

Segmental Analysis

The market is segmented by packaging type, material type, application, technology, and region. By packaging type, the market is divided into recyclable packaging, biodegradable, compostable, and others. Based on material type, the market is categorized into paper & paperboard, plastics, metal, and glass. In terms of application, the market is segmented into food & beverages, personal care, online retail, and industrial. By technology, the market includes barrier coatings, bio-based materials, recycled content, and smart packaging. Regionally, the market is divided into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

By Packaging Type, Recyclable Packaging Segment Accounts for 42% Market Share

The recyclable packaging segment is projected to account for 42% of the sustainable food packaging market in 2025, reaffirming its position as the category’s dominant packaging approach. Recyclable packaging offers established infrastructure compatibility, proven environmental benefits, and consumer familiarity that supports widespread adoption across diverse food and beverage applications. This segment leverages existing recycling systems while providing materials that can maintain functionality and cost-effectiveness compared to conventional packaging alternatives.

This segment forms the foundation of the sustainable packaging transition, as it represents the most immediately scalable and economically viable approach to reducing packaging environmental impact. The continuous improvement of recycling technologies, expansion of collection infrastructure, and increasing recycled content requirements continue to strengthen adoption across both developed and emerging markets. With growing regulatory support for recycling systems and increasing consumer participation in recycling programs, the recyclable packaging segment aligns with both immediate sustainability requireds and long-term circular economy objectives.

By Material Type, Paper & Paperboard Segment Accounts for 45% Market Share

Paper & paperboard materials are projected to represent 45% of sustainable food packaging demand in 2025, underscoring their role as the primary sustainable material category for food packaging applications. Paper-based materials offer renewable resource sourcing, established recycling infrastructure, and biodegradable properties that appeal to environmentally conscious consumers and regulatory frameworks. Positioned as proven sustainable alternatives, these materials provide reliable barrier properties, printability, and structural integrity for diverse packaging formats including boxes, bags, wraps, and containers.

The segment is supported by the mature foresattempt indusattempt, advanced paper manufacturing technologies, and continuous innovation in barrier coatings and treatments that enhance performance for food contact applications. Additionally, paper and paperboard materials benefit from consumer preference for materials perceived as natural and environmentally friconcludely while supporting established supply chains and processing capabilities. As sustainability regulations continue to favor renewable materials and recycling infrastructure expands globally, paper and paperboard will maintain their leading position, reinforcing their essential role in the sustainable packaging ecosystem.

By Application, Food & Beverages Segment Accounts for 60% Market Share

The food & beverages application segment is forecasted to contribute 60% of the sustainable food packaging market in 2025, reflecting the massive scale of global food packaging requireds and the increasing sustainability requirements across food supply chains. Food and beverage companies face growing pressure from consumers, retailers, and regulators to adopt sustainable packaging while maintaining product safety, quality, and shelf-life requirements. This segment benefits from established packaging requirements, large volume applications, and strong sustainability commitments from major food brands and retailers.

The segment also benefits from food and beverage companies’ substantial purchasing power and their ability to drive innovation through collaboration with packaging suppliers and material developers. With growing consumer awareness of packaging waste and increasing regulatory requirements for sustainable packaging across food categories, food and beverages serve as the primary market for sustainable packaging innovation while supporting technology development and scaling of sustainable material production across the packaging indusattempt.

What are the Drivers, Restraints, and Key Trconcludes of the Sustainable Food Packaging Market?

The sustainable food packaging market is advancing rapidly due to increasing environmental regulations and growing consumer preference for eco-friconcludely products. However, the market faces challenges including higher material costs, performance limitations of some sustainable alternatives, and complex recycling infrastructure requirements. Innovation in material science and processing technologies continue to influence solution effectiveness and market accessibility.

Strengthening Regulatory Frameworks and Plastic Waste Legislation

The implementation of comprehensive plastic waste legislation including single-apply plastic bans, extconcludeed producer responsibility programs, and recycled content mandates is driving significant demand for sustainable packaging alternatives. Government agencies worldwide are establishing packaging waste reduction tarobtains, material restriction policies, and circular economy frameworks that require companies to transition to sustainable packaging solutions. These regulatory drivers create sustained demand for packaging materials and designs that can deliver environmental compliance while maintaining commercial functionality and cost competitiveness.

Integration of Advanced Material Technologies and Bio-Based Innovation

Modern sustainable packaging manufacturers are incorporating advanced bio-based materials, nanotechnology coatings, and smart packaging features to enhance performance while maintaining environmental credentials. These technologies enable the development of packaging solutions that can match or exceed conventional packaging performance while offering superior conclude-of-life options including compostability, recyclability, and biodegradation. Advanced material innovation also enables the creation of packaging systems that provide enhanced product protection, extconcludeed shelf life, and improved consumer experience while supporting sustainability objectives.

Sustainable Food Packaging Market by Key Counattempt

Europe Market Split by Counattempt

The sustainable food packaging market in Europe demonstrates advanced development across major economies with Germany revealing strong presence through its leadership in environmental technology and comprehensive sustainability frameworks, supported by companies leveraging engineering excellence to develop innovative packaging solutions that meet stringent environmental standards while delivering superior functional performance across diverse food and beverage applications.

France represents a significant market driven by its commitment to circular economy principles and sophisticated understanding of packaging lifecycle management, with companies pioneering advanced sustainable packaging technologies that combine French environmental leadership with innovative material science for enhanced sustainability outcomes and regulatory compliance. The UK exhibits considerable growth through its post-Brexit environmental indepconcludeence and comprehensive plastic waste reduction initiatives, with packaging manufacturers leading the adoption of bio-based materials and advanced recycling technologies.

Italy and Spain reveal expanding interest in sustainable packaging solutions, particularly for applications supporting premium food products and export market requirements that demand environmental credentials and quality assurance. BENELUX countries contribute through their focus on circular economy innovation and international sustainability leadership, while Eastern Europe and Nordic regions display growing potential driven by EU regulatory alignment and increasing investment in sustainable packaging infrastructure across diverse food and beverage sectors.

Japan Market Split by Counattempt

The Japanese sustainable food packaging market demonstrates steady growth driven by precision manufacturing focus, advanced material technologies, and consumer preference for high-quality packaging solutions that combine environmental responsibility with superior functional performance and aesthetic appeal. The market emphasizes innovative material development, sophisticated barrier technologies, and precision manufacturing processes that reflect Japanese attention to detail and quality excellence in packaging applications. Growing environmental awareness and regulatory initiatives supporting sustainable packaging drive demand for recyclable materials, bio-based alternatives, and circular economy solutions across food and beverage sectors.

Japanese companies prioritize packaging innovation, material quality, and environmental performance, creating opportunities for premium sustainable packaging solutions that deliver exceptional functionality while meeting strict environmental standards. The integration of traditional Japanese environmental principles with modern packaging technology positions Japan as an important market for advanced sustainable packaging applications requiring superior quality, innovative materials, and comprehensive environmental stewardship across diverse food packaging applications.

South Korea Market Split by Counattempt

The South Korean sustainable food packaging market reveals emerging growth potential driven by expanding environmental awareness, increasing regulatory requirements, and growing corporate sustainability commitments that align with the counattempt’s green growth initiatives and circular economy development programs. The market benefits from South Korea’s technological advancement capabilities and increasing focus on environmental innovation that drives investment in sustainable packaging materials, recycling technologies, and circular economy solutions. Korean companies increasingly adopt recyclable packaging systems, bio-based materials, and advanced recycling technologies to improve environmental performance while meeting commercial functionality requirements and consumer expectations.

Growing influence of Korean food exports and K-culture globally supports demand for sustainable packaging that meets international environmental standards while maintaining product quality and brand appeal. The integration of traditional Korean environmental values with modern sustainable packaging technologies creates opportunities for innovative solutions that combine cultural responsibility with technological advancement. Rising consumer environmental consciousness and government support for green technology development drive adoption of sustainable packaging solutions across food and beverage applications requiring comprehensive environmental performance, commercial functionality, and cultural authenticity for both domestic and international markets.

Analysis of Sustainable Food Packaging Market by Key Counattempt

| Counattempt | CAGR (2025-2035) |

|---|---|

| USA | 6.2% |

| Germany | 6.0% |

| China | 5.8% |

| France | 5.5% |

| UK | 5.3% |

| India | 4.9% |

| Brazil | 4.7% |

The sustainable food packaging market is experiencing robust growth globally, with the USA leading at a 6.2% CAGR through 2035, driven by state-level plastic waste legislation, corporate sustainability commitments, and consumer environmental awareness. Germany follows at 6.0%, supported by environmental technology leadership and comprehensive circular economy frameworks. China reveals steady growth at 5.8%, focapplying on pollution reduction initiatives and manufacturing capacity development. France records 5.5%, emphasizing circular economy principles and packaging lifecycle management. The UK demonstrates 5.3% growth, driven by environmental indepconcludeence and plastic waste reduction policies.

The report covers an in-depth analysis of 40+ countries; seven top-performing countries are highlighted below.

USA Leads Market Growth with Regulatory Innovation

Revenue from sustainable food packaging in the USA is projected to exhibit strong growth with a CAGR of 6.2% through 2035, driven by state-level plastic waste legislation, corporate sustainability commitments, and increasing consumer environmental awareness. The counattempt’s diverse regulatory landscape and advanced packaging indusattempt are creating significant opportunities for sustainable packaging innovation. Major packaging manufacturers and food brands are investing in sustainable material development and supply chain transformation to serve evolving regulatory and market requirements.

- State-level legislation and corporate commitments are creating substantial opportunities for sustainable packaging solutions designed for regulatory compliance and brand differentiation.

- Consumer environmental awareness and purchasing preferences are driving development of premium sustainable packaging with enhanced functionality and marketing appeal.

Germany Demonstrates Strong Market Leadership with Technology Excellence

Revenue from sustainable food packaging in Germany is expanding at a CAGR of 6.0%, supported by environmental technology leadership, comprehensive circular economy frameworks, and advanced manufacturing capabilities. The counattempt’s engineering excellence and sustainability commitment are driving demand for innovative packaging solutions that deliver superior environmental performance. Leading packaging manufacturers are establishing comprehensive research and development capabilities to serve both domestic and international markets.

- Environmental technology leadership and circular economy frameworks are creating significant demand for advanced sustainable packaging with proven environmental benefits and commercial viability.

- Manufacturing excellence and innovation capabilities are supporting development of premium packaging solutions for diverse food and beverage applications across global markets.

China Shows Strong Growth with Manufacturing Leadership

Revenue from sustainable food packaging in China is projected to grow at a CAGR of 5.8% through 2035, supported by pollution reduction initiatives, manufacturing capacity development, and growing environmental awareness among urban consumers. The counattempt’s massive manufacturing infrastructure and evolving environmental policies are driving demand for sustainable packaging across domestic and export markets. Major packaging manufacturers are establishing comprehensive sustainable production capabilities to serve global supply chains.

- Manufacturing capacity and pollution reduction initiatives are creating increased demand for sustainable packaging solutions supporting both domestic consumption and export market requirements.

- Growing environmental awareness and urban consumer preferences are supporting market development for premium sustainable packaging across diverse food and beverage categories.

France Maintains Leadership with Circular Economy Excellence

Revenue from sustainable food packaging in France is projected to grow at a CAGR of 5.5% through 2035, supported by circular economy leadership, packaging lifecycle management expertise, and comprehensive environmental frameworks. French companies prioritize environmental performance, material innovation, and sustainable design principles, creating opportunities for advanced packaging solutions across food and luxury goods sectors.

- Circular economy leadership and lifecycle management expertise are driving demand for comprehensive sustainable packaging solutions that deliver measurable environmental benefits throughout product lifecycles.

- Environmental frameworks and sustainability standards are supporting adoption of innovative packaging materials and design approaches across diverse commercial applications.

UK Strengthens Market with Environmental Indepconcludeence

Revenue from sustainable food packaging in the UK is projected to grow at a CAGR of 5.3% through 2035, supported by post-Brexit environmental indepconcludeence, plastic waste reduction policies, and comprehensive sustainability frameworks. British companies value environmental performance, innovation capabilities, and market differentiation, positioning sustainable packaging as essential components of competitive advantage and regulatory compliance.

- Environmental indepconcludeence and policy innovation are driving demand for sustainable packaging solutions that support autonomous environmental standards and international market access.

- Plastic waste reduction initiatives and sustainability frameworks are encouraging adoption of advanced packaging materials and circular economy principles across food and beverage sectors.

India Demonstrates Growing Market Acceptance with Environmental Awareness

Revenue from sustainable food packaging in India is expanding at a CAGR of 4.9%, supported by growing environmental awareness, urbanization trconcludes, and increasing regulatory attention to packaging waste management. The counattempt’s large population and expanding middle class are creating significant opportunities for sustainable packaging adoption across food and consumer goods sectors. International and domestic packaging companies are establishing scalable production capabilities to serve the evolving market requirements.

- Environmental awareness growth and urbanization trconcludes are creating increased demand for sustainable packaging solutions supporting urban lifestyle alters and environmental consciousness.

- Regulatory development and waste management initiatives are supporting market expansion for packaging materials and systems that address local environmental challenges and infrastructure capabilities.

Brazil Shows Emerging Market Growth with Sustainability Focus

Revenue from sustainable food packaging in Brazil is projected to grow at a CAGR of 4.7% through 2035, supported by environmental awareness development, agricultural export requirements, and increasing corporate sustainability commitments. The counattempt’s large food production sector and growing environmental consciousness provide significant opportunities for sustainable packaging market expansion and technology adoption.

- Agricultural export requirements and environmental standards are creating substantial demand for sustainable packaging solutions supporting international market access and quality assurance.

- Corporate sustainability commitments and environmental awareness are supporting market development for packaging materials that combine environmental benefits with commercial functionality across diverse food sectors.

Competitive Landscape of Sustainable Food Packaging Market

The sustainable food packaging market is characterized by competition among established packaging manufacturers, specialty sustainable material producers, and emerging technology innovators. Companies are investing in advanced material development, sustainable manufacturing processes, circular economy integration, and global supply chain capabilities to deliver comprehensive, functional, and environmentally responsible packaging solutions. Innovation capabilities, sustainability credentials, and supply chain reliability are central to strengthening market position and customer relationships.

Amcor Plc, Australia-based, leads the market with 16.5% global value share, offering comprehensive packaging solutions with focus on recyclable materials, sustainable innovation, and global manufacturing capabilities across flexible and rigid packaging applications. WestRock, USA, provides integrated paper and packaging solutions with emphasis on renewable materials, recycling capabilities, and supply chain optimization. International Paper, USA, delivers comprehensive paper-based packaging with focus on sustainable foresattempt practices and recycled content integration.

Tetra Pak, Sweden, focapplys on sustainable food packaging systems with emphasis on renewable materials, recycling infrastructure, and food safety technology for liquid food applications. Sealed Air Corporation, USA, provides protective packaging solutions with focus on material reduction, recyclable designs, and supply chain efficiency optimization. Berry Global, USA, offers diverse packaging solutions with emphasis on sustainable material development and circular economy integration.

Mondi Group, Austria, emphasizes sustainable paper and packaging solutions with focus on renewable materials, innovative design, and comprehensive sustainability reporting. Graphic Packaging Holding, USA, provides paperboard packaging solutions with focus on renewable materials and recycling compatibility for food and beverage applications. Ranpak Holdings, USA, delivers protective packaging systems with emphasis on paper-based alternatives and sustainable e-commerce packaging solutions.

Key Players in the Sustainable Food Packaging Market

- Amcor Plc

- WestRock

- International Paper

- Tetra Pak

- Sealed Air Corporation

- Berry Global

- Mondi Group

- Graphic Packaging Holding

- Ranpak Holdings

Scope of the Report

| Items | Values |

|---|---|

| Quantitative Units (2025) | USD 301.8 Billion |

| Packaging Type | Recyclable packaging, Biodegradable, Compostable, Others |

| Material Type | Paper & paperboard, Plastics, Metal, Glass |

| Application | Food & beverages, Personal care, Online retail, Industrial |

| Technology | Barrier coatings, Bio-based materials, Recycled content, Smart packaging |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Countries Covered | United States, Canada, United Kingdom, Germany, France, China, Japan, South Korea, India, Brazil, Australia and 40+ countries |

| Key Companies Profiled | Amcor Plc, WestRock, International Paper, Tetra Pak, Sealed Air Corporation, Berry Global, Mondi Group, Graphic Packaging Holding, and Ranpak Holdings |

| Additional Attributes | Dollar sales by packaging type and material, regional sustainability trconcludes, competitive landscape, purchaseer preferences for recyclable versus biodegradable solutions, integration with circular economy principles, innovations in bio-based materials, smart packaging technology, and lifecycle assessment methodologies |

Sustainable Food Packaging Market by Segments

-

Packaging Type :

- Recyclable packaging

- Biodegradable

- Compostable

- Others

-

Material Type :

- Paper & paperboard

- Plastics

- Metal

- Glass

-

Application :

- Food & beverages

- Personal care

- Online retail

- Industrial

-

Technology :

- Barrier coatings

- Bio-based materials

- Recycled content

- Smart packaging

-

Region :

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic

- BENELUX

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Chile

- Rest of Latin America

- Middle East & Africa

- Kingdom of Saudi Arabia

- Other GCC Countries

- Turkey

- South Africa

- Other African Union

- Rest of Middle East & Africa

- North America