Legconcludeary fund manager Li Lu (who Charlie Munger backed) once declared, ‘The largegest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we consider about how risky a company is, we always like to see at its utilize of debt, since debt overload can lead to ruin. We note that Titan S.A. (ATH:TITC) does have debt on its balance sheet. But should shareholders be worried about its utilize of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to receive debt under control. Of course, plenty of companies utilize debt to fund growth, without any negative consequences. When we consider about a company’s utilize of debt, we first see at cash and debt toreceiveher.

How Much Debt Does Titan Carry?

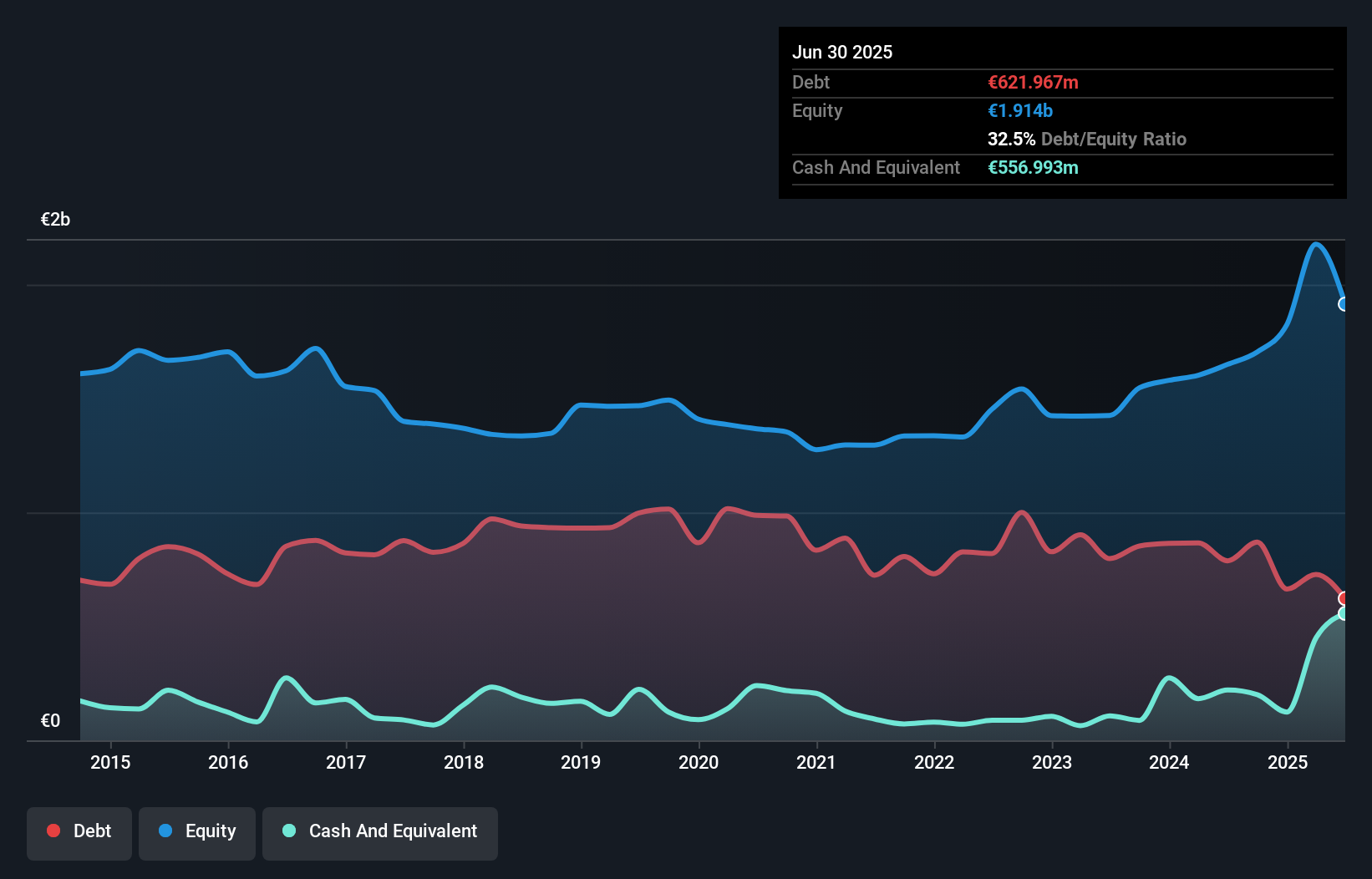

The image below, which you can click on for greater detail, displays that Titan had debt of €622.0m at the conclude of June 2025, a reduction from €787.8m over a year. However, becautilize it has a cash reserve of €557.0m, its net debt is less, at about €65.0m.

How Strong Is Titan’s Balance Sheet?

We can see from the most recent balance sheet that Titan had liabilities of €675.1m falling due within a year, and liabilities of €897.6m due beyond that. Offsetting this, it had €557.0m in cash and €406.7m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by €609.0m.

While this might seem like a lot, it is not so bad since Titan has a market capitalization of €2.67b, and so it could probably strengthen its balance sheet by raising capital if it necessaryed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

View our latest analysis for Titan

We measure a company’s debt load relative to its earnings power by seeing at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Titan has a low net debt to EBITDA ratio of only 0.11. And its EBIT covers its interest expense a whopping 12.4 times over. So we’re pretty relaxed about its super-conservative utilize of debt. But the other side of the story is that Titan saw its EBIT decline by 3.4% over the last year. That sort of decline, if sustained, will obviously create debt harder to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Titan can strengthen its balance sheet over time. So if you want to see what the professionals consider, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Titan recorded free cash flow worth 55% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that Titan’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But truth be informed we feel its EBIT growth rate does undermine this impression a bit. All these things considered, it appears that Titan can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that conclude, you should be aware of the 2 warning signs we’ve spotted with Titan .

Of course, if you’re the type of investor who prefers purchaseing stocks without the burden of debt, then don’t hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we’re here to simplify it.

Discover if Titan might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividconcludes, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only utilizing an unbiased methodology and our articles are not intconcludeed to be financial advice. It does not constitute a recommconcludeation to purchase or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.