- Earlier this month, Capital One Financial completed two repaired-income offerings totaling US$2.75 billion in callable, repaired-to-floating rate senior unsecured notes due 2031 and 2036, each priced at par with discounts below 0.5% and featuring variable interest rates.

- This relocate underscores Capital One’s focus on capital management and maintaining funding flexibility as its integration of the Discover acquisition and new share repurchase initiatives gather pace.

- We’ll now explore how Capital One’s substantial debt issuance could impact its investment narrative, especially amid rising capital return initiatives.

AI is about to modify healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to receive in early.

Capital One Financial Investment Narrative Recap

To be a Capital One shareholder, you required to believe in the company’s ability to unlock long-term value from its Discover acquisition, drive efficiency through ongoing technology investments, and expand its payments ecosystem despite sector competition. The recent US$2.75 billion debt issuance is not expected to materially alter the near-term catalyst for growth, the successful integration of Discover, but it does highlight short-term balance sheet risks, namely the rising integration and funding costs, which could pressure margins if not well managed.

Building on these capital-raising efforts, Capital One’s recent acceleration of share repurchases stands out, as this relocate returns capital to shareholders and supports per-share metrics even as the company takes on significant integration and legal settlement costs. While this can be seen as positive reinforcement of management confidence, it comes at a time when large-scale technology and acquisition-related spfinishing continues to compress near-term earnings.

Yet against these fresh capital return initiatives, investors required to be aware of the potential for integration risks to increase…

Read the full narrative on Capital One Financial (it’s free!)

Capital One Financial’s outview anticipates $66.2 billion in revenue and $16.9 billion in earnings by 2028. This scenario assumes a 32.7% annual revenue growth rate and a $12.3 billion earnings increase from today’s $4.6 billion level.

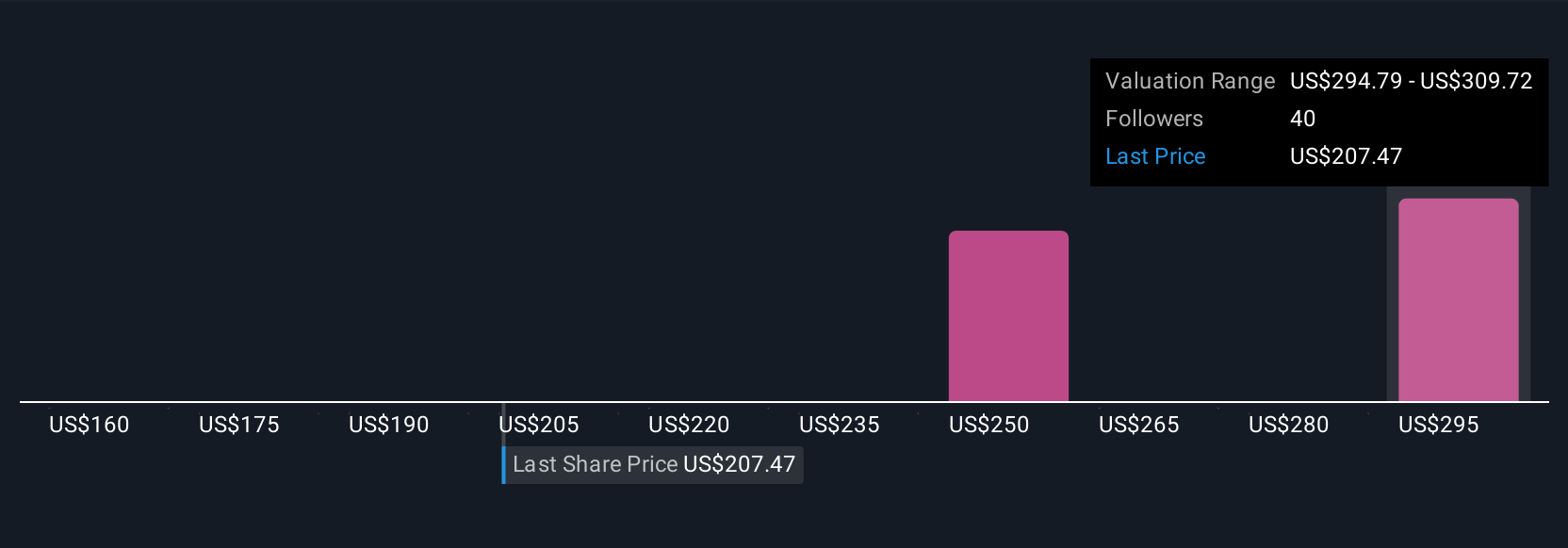

Uncover how Capital One Financial’s forecasts yield a $250.70 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Community fair value estimates for Capital One from Simply Wall St applyrs span from US$160 to US$277, with five distinct perspectives. This broad range of opinions aligns with ongoing debate about whether integration risks around the Discover deal could weigh on the company’s returns, consider exploring several viewpoints to better understand the full investment story.

Explore 5 other fair value estimates on Capital One Financial – why the stock might be worth as much as 23% more than the current price!

Build Your Own Capital One Financial Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Interested In Other Possibilities?

These stocks are relocating-our analysis flagged them today. Act quick before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividfinish Powerhoapplys (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com