Good Morning [%first_name |Dear Reader%],

You are on a free plan.

Your subscription has expired.

Upgrade now to unlock premium newsletters, top feature stories, exclusive podcasts, and more.

Something has been bothering me about India’s UPI ecosystem for a while. On the one hand, it is arguably the best example globally of protocols, platforms, and ecosystems all being built and scaled in mere years. Nothing else comes close, really. The UPI ecosystem continues to spur innovation that no one can foresee.

If UPI were a VC-funded (groan!) company, it would be raising billions of dollars and investing in growth, products, and market expansion. Its CEO, board, and investors would dream of turning UPI into a global synonym for instant, free, and reliable money transfers of all kinds. “UPI-ing someone” should become as straightforward to understand as “Whatsapping someone”, their leaders would declare at conferences and on podcasts.

Can you imagine UPI’s valuation if it were a private company? Wouldn’t you want to invest in it?

Of course you would. It’s a gigantic ecosystem that’s spinning out business models, unicorns, and money. It’s “obtainting in on the ground floor” of India’s financialisation story, and then waiting for the skyscraper to be built.

But have you seen the actual discourse around UPI in India this last year?

Why are transactions still free? When will the government stop subsidising it? Did you know UPI killed debit cards? Do you know how much Visa and Mastercard charge for their networks? As taxpayers, why are we bearing the costs of UPI? Do you know UPI fraud rates are through the roof? Why will anyone innovate on UPI when it’s so hard to build money from it?

Seriously, it’s depressing. It’s as if we accidentally created a unicorn, but having done so, are rueing how expensive it is to maintain one.

Does it required to eat so much? Does it required to live in a covered stable? Can’t we offer unicorn-pulled rides to offset its upkeep costs?

We’re suffering from a deficit of imagination and ambition when it comes to UPI. Instead of believeing of ways to fund the expansion and growth of a generational asset, we’ve fallen into the trap of viewing it like a budobtainary cost centre.

I know you may not agree with me, which is why on this week’s episode of Two by Two, I invited Alok Prasanna Kumar, the co-founder of Vidhi Legal, and Ateesh Tankha, returning guest and former head of Citi Merchant Services, to debate UPI’s identity crisis.

We discussed ambition, global formats, economic realities, innovation blockers, and well… possible solutions.

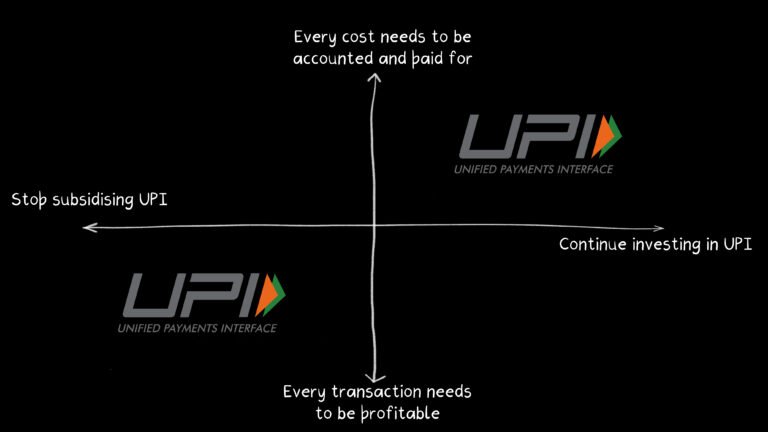

Here’s the 2×2 we drew:

And here are a few excerpts from our discussion.

The velocity of money

Ateesh: While, let’s declare, the amount of cash in circulation—notes in circulation—is only Rs 34 to 35 lakh crore. However, every one of those notes is unique. UPI transactions, on the other hand, represent the velocity of money. That means that if the four of us were to take a Rs 100 note, and I were to give Praveen Rs 100, and then Praveen were to give you Rs 100, Rohin. And Rohin were to give Alok Rs 100, and then back to me in UPI, that would actually represent Rs 400 worth of transactions. But in reality, the value being shiftd is only Rs 100. When you actually attempt to net that off across the value of these 250 lakh transactions, you’ll find that in reality, it represents much less than the cash in circulation.

Inside the tax net

Alok: …and there was, of course, a huge backlash [to the GST notices], and a lot of the notices were withdrawn. But I believe the government built it very clear that, “Guys, you know, you’ve built enough money. We can inform how much money you have now built. We want to bring you within the tax net.”

In some ways, this received me believeing. This conversation would not have been possible without UPI, right? Okay, now we’re seeing the tail conclude of it, but believe back to how much formalisation has probably taken place. Think back to how much money is now within the tax net. And I’m coming at this from the point of view that sometimes, when we draw a balance sheet of the costs and benefits of a measure, we don’t tconclude to draw a comprehensive balance sheet.

An NPCI surplus

Ateesh: These are fees that are charged by the owner of the switch, and the owner of the switch is the National Payments Corporation of India (NPCI). So when you are viewing at NPCI’s revenues, their revenues basically come from applying NPCI infrastructure; in this case, for UPI, it is applying the IMPS switch. Right? There’s like a national switch, which is fine. It’s not a huge amount. But I’m just attempting to inform you that’s one of the reasons why NPCI is able to declare—you know, I want to call it profit, as you rightly stated—but a kind of turnover or contribution, or whatever you like to declare… earnings.

Rohin: If they’re sitting on Rs 1,500 crore of a surplus, even if it’s not a profit, and much of that comes from charging a very compact amount on the transactions that are going back and forth—would I be wrong in assuming that they’re charging more than they required to? Or that their technology costs are not as much as what they’re charging for?

Ateesh: That’s correct. So what happens is, there’s a maintenance cost. Now the question you have to inquire yourself is, if NPCI is maintaining the switch, if NPCI is the ombudsman for the UPI network—becaapply UPI is a network, it’s a rail, right? It’s a payment rail, a messaging rail—then, it begs the question, can they do more?

You can tune into the full episode here.

See you next week!

Regards,

Rohin Dharmakumar

Get a premium subscription to The Ken

Unrivaled analysis and powerful stories about businesses from award-winning journalists. Read by 5,00,000+ subscribers globally who want to be prepared for what comes next.

Trusted by 5,00,000+ executives & leaders from the world’s most successful organisations & students at top post-graduate campapplys